Global| Apr 04 2007

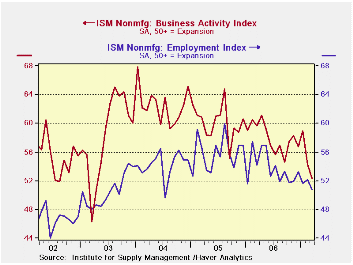

Global| Apr 04 2007Nonmanufacturing ISM: Sharp Two-Month Drop Off

ISM trends show a weakening trend in the services-mining-construction sector of the economy to add to the lethargy in manufacturing. The past two months show that the index has dropped to a much lower profile than before. This is the weakest activity recorded since early 2003. Employment trend has been ground into a lower profile as well. The results are disconcerting although it may be that ongoing construction problems are weighing on the index and services are not as weak as the index suggests.

ISM trends show a weakening trend in the services-mining-construction sector of the economy to add to the lethargy in manufacturing. The past two months show that the index has dropped to a much lower profile than before. This is the weakest activity recorded since early 2003. Employment trend has been ground into a lower profile as well. The results are disconcerting although it may be that ongoing construction problems are weighing on the index and services are not as weak as the index suggests.

An analysis of the position of the various ISM components in their respective ranges shows that weakness characterizes this sector. Both activity and orders are below their range midpoints and below their period average values. Order backlogs continue to appear strong as an offset, as we have seen in durable goods order report. Unlike the ISM manufacturing we see that export and import services are weak. For manufacturing these two series were quite firm. Price readings rose in the month and remain firm in their historic range. On balance, the nonmanufacturing sector does not appear to be as strong or supportive of the economy as it once was. It raises the question of whether the weakness in manufacturing and construction industries has ground down the once vibrant services sector that is nested within the nonmanufacturing ISM.

| ISM Nonmanufacturing Statistics from January 1998 to Date | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| ISM-NMFG | Current | Std Dev | Average | SD %Avg | MAX | MIN | Range | Percentile | % of AVG |

| PM Activity | 52.4 | 4.7 | 57.5 | 8.2 | 67.9 | 40.5 | 27.4 | 43.4 | 91 |

| New Orders | 53.8 | 4.7 | 57.2 | 8.2 | 66.9 | 41.3 | 25.6 | 48.8 | 94 |

| Backlogs | 52.5 | 3.7 | 51.0 | 7.2 | 57.0 | 40.5 | 16.5 | 72.7 | 103 |

| Supplier Deliveries | 50.0 | 2.1 | 53.6 | 4.0 | 60.5 | 48.0 | 12.5 | 16.0 | 93 |

| Inventory Sentiment | 63.0 | 2.7 | 63.1 | 4.3 | 69.0 | 55.0 | 14.0 | 57.1 | 100 |

| Inventories | 52.0 | 3.2 | 50.5 | 6.2 | 59.0 | 43.5 | 15.5 | 54.8 | 103 |

| Prices | 63.3 | 8.3 | 59.8 | 13.9 | 80.5 | 41.3 | 39.2 | 56.1 | 106 |

| Employment | 50.8 | 3.7 | 51.7 | 7.1 | 59.9 | 43.9 | 16.0 | 43.1 | 98 |

| Export Orders | 48.5 | 4.5 | 54.8 | 8.3 | 64.0 | 44.5 | 19.5 | 20.5 | 89 |

| Import Orders | 50.0 | 4.0 | 54.7 | 7.4 | 63.5 | 45.5 | 18.0 | 25.0 | 91 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief