Asia| Nov 03 2025

Asia| Nov 03 2025Economic Letter from Asia: Come Together

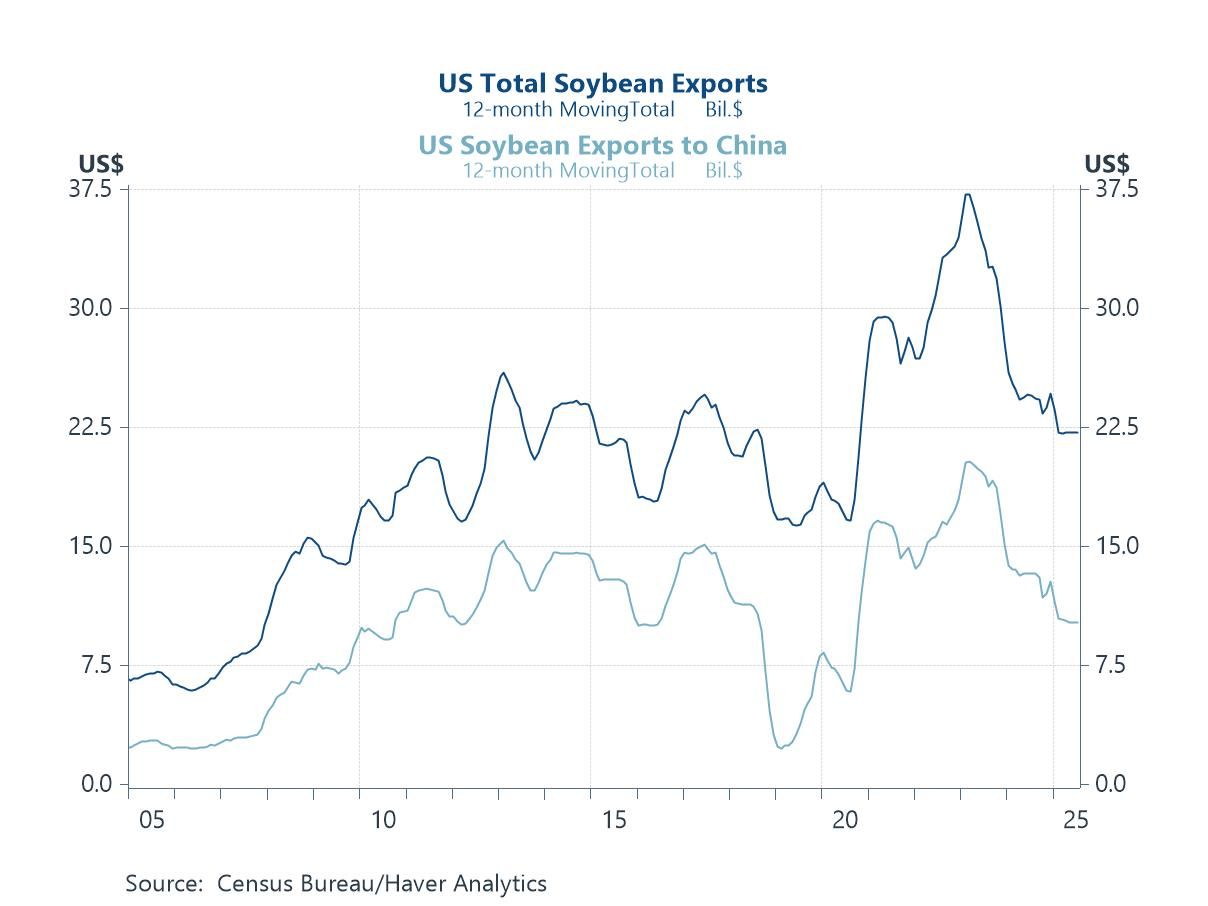

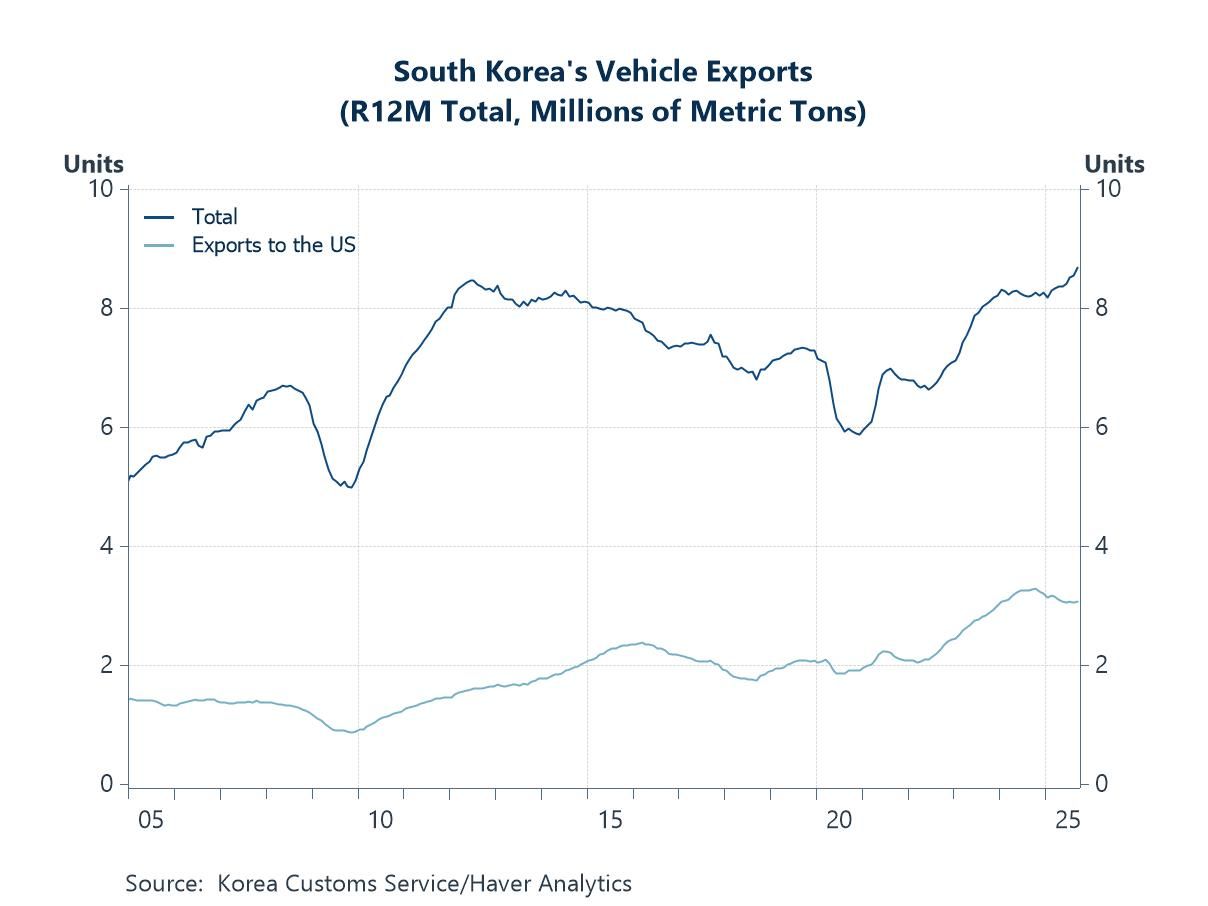

This week, we review a wave of key developments across Asia following US President Trump’s tour of the region last week. A central theme concerned countries courting closer ties with the US to avoid harsher actions, while also boosting regional cooperation amid trade barriers and scrutiny of China. This push for closer ties has manifested through new and updated trade agreements—ironically driven by ongoing uncertainty in global trade and supply chains, with US–China relations at the core. A major outcome of Trump’s trip was the new US–China trade agreement, which included the US halving tariffs on Chinese fentanyl-related products to 10%, while China suspended rare earth export controls and resumed soybean purchases vital to the US (chart 1). Perhaps more importantly, the deal signalled a small conciliatory shift and avoided a potentially worse outcome. Beyond the US–China agreement at the APEC Summit in South Korea, the US–South Korea trade deal also gained more clarity. Under the deal, US auto tariffs on South Korea has fallen to 15%, matching the rate applied to Japan and likely providing relief for South Korean automakers (chart 2).

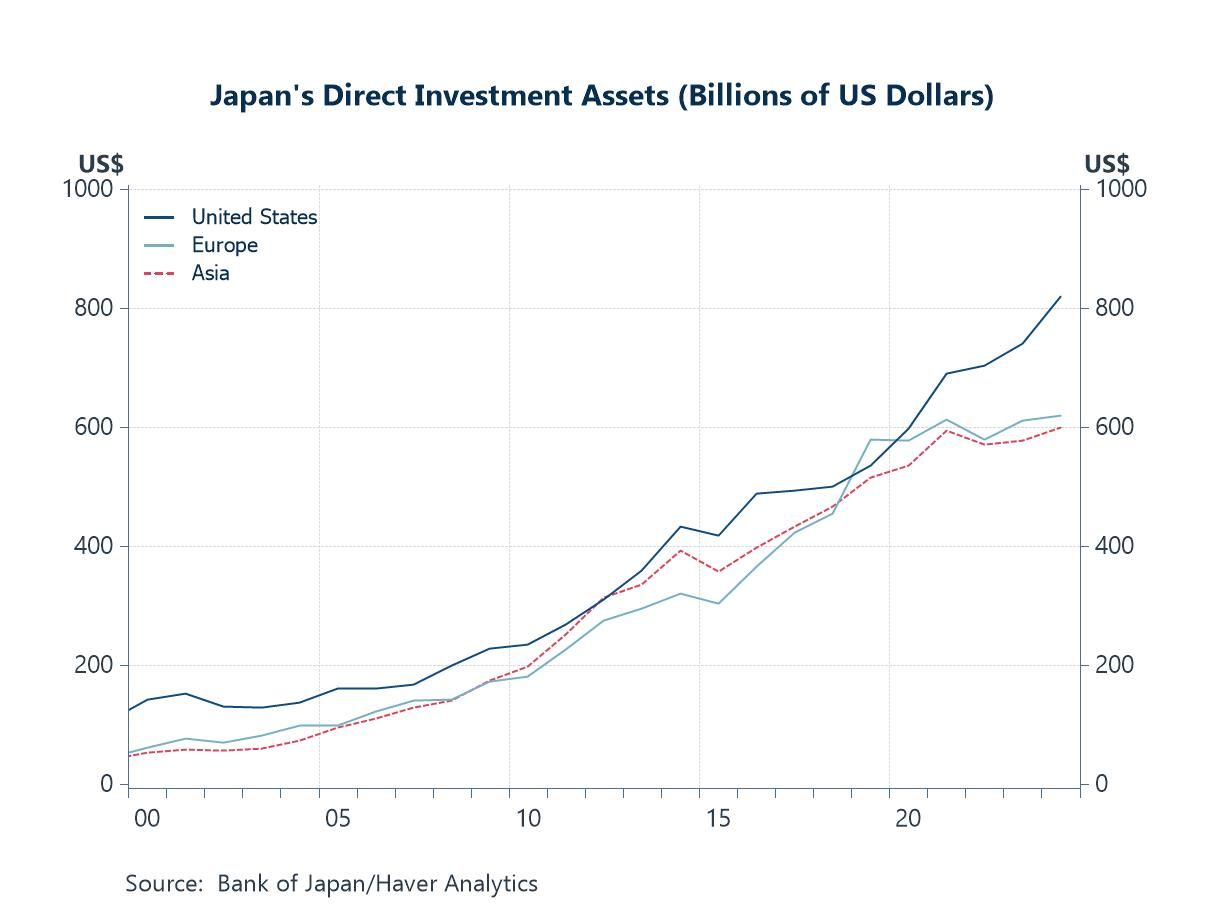

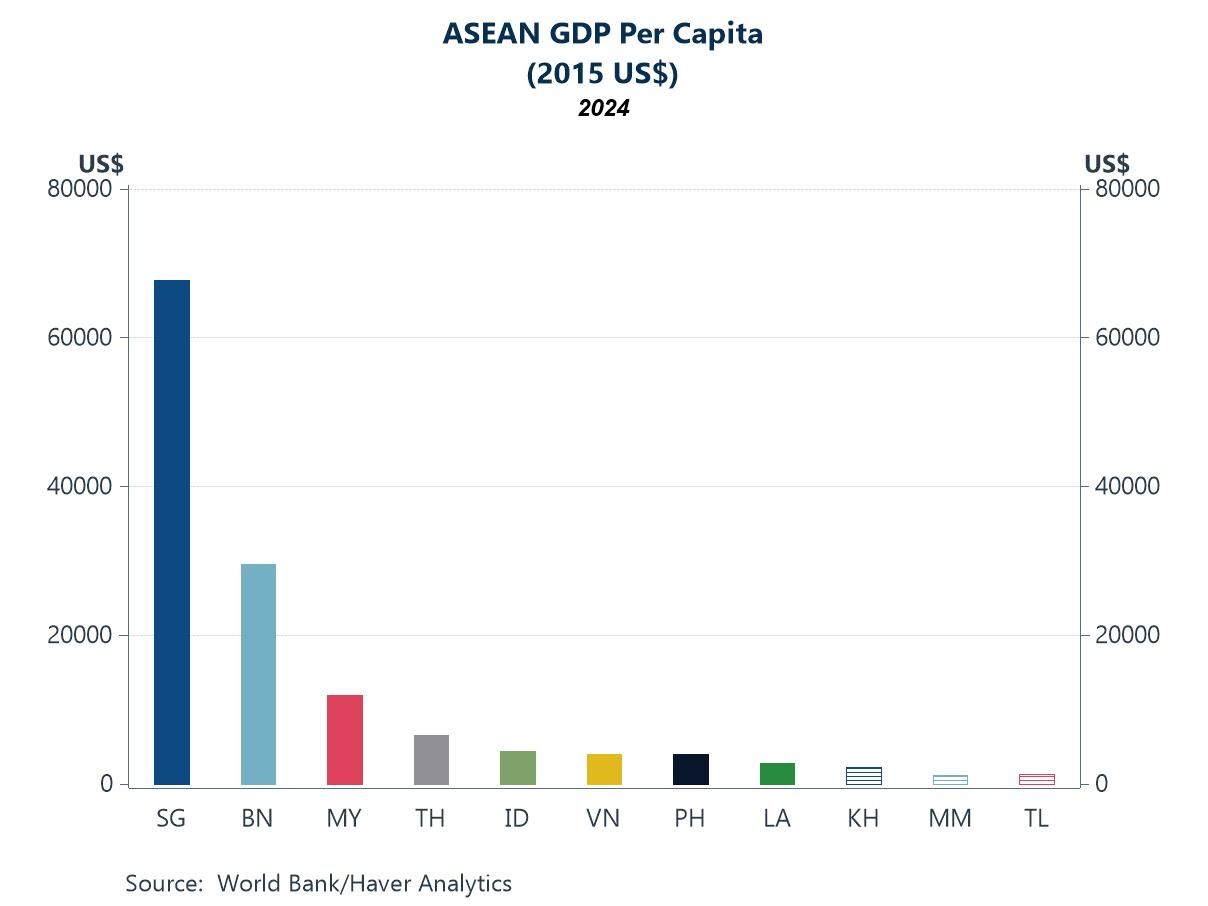

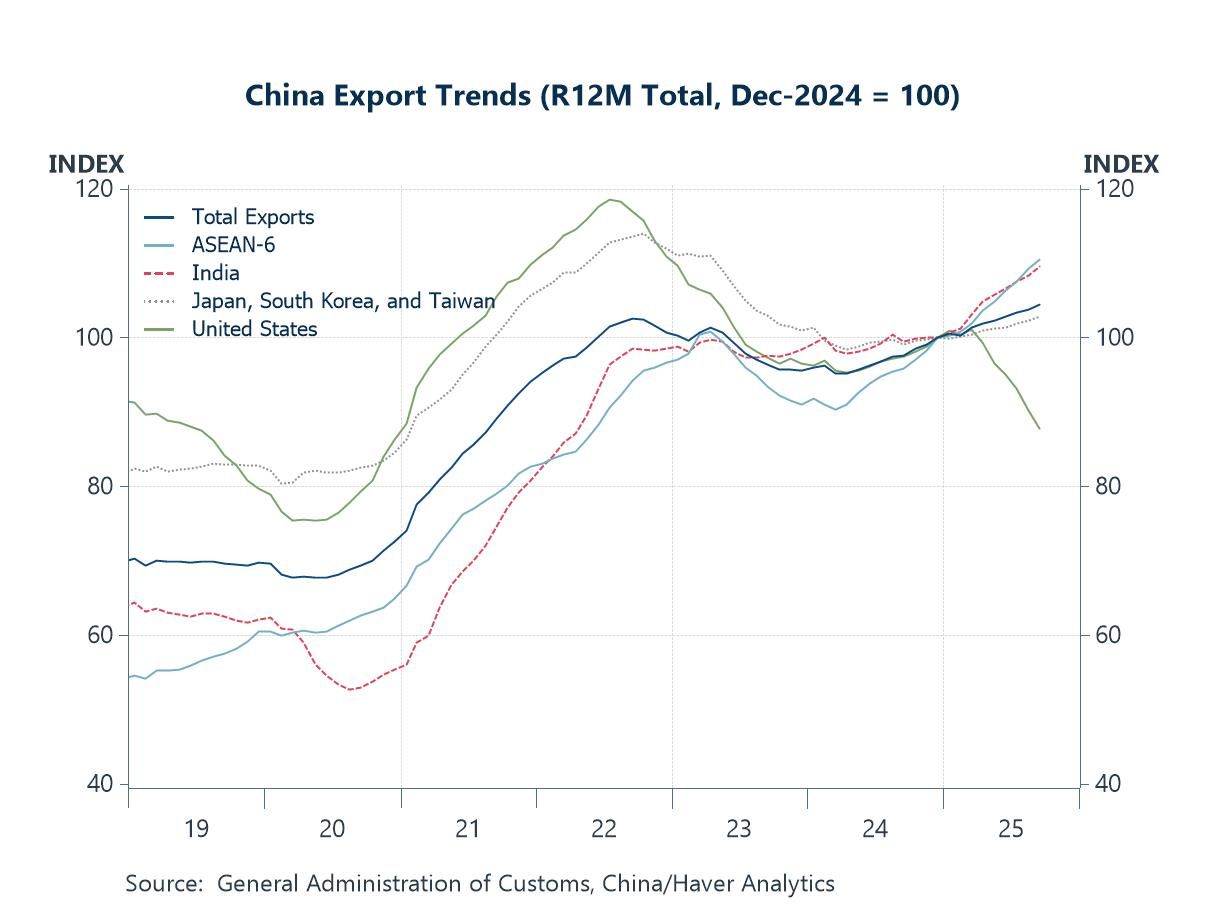

Trump’s visit to Japan was another highlight. Relations with new Prime Minister Takaichi got off to a strong start, and further details emerged on Japan’s previously cited $550 billion investment commitment in the US—substantial even relative to Japan’s existing direct investment there (chart 3). However, specifics on the timing and implementation of the investment remain limited. Meanwhile, at the ASEAN Summit earlier in the week, aside from Trump’s engagements, the bloc officially welcomed its 11th member—Timor-Leste—the first new member in decades—granting it access to the bloc’s mechanisms and potentially supporting a catch-up in economic development (chart 5). Looking ahead, the focus on China and Japan is likely to continue, with China set to release its October trade (chart 6) and CPI data, and Japan scheduled to report employee wages and household spending.

The APEC summit The US and China made a modest but meaningful step forward on trade following the Trump–Xi meeting at the APEC Summit in South Korea. The US lowered tariffs on Chinese fentanyl-related products to 10% from 20% and suspended enforcement of rules targeting subsidiaries of blacklisted firms—previous points of contention for Beijing. In return, China pledged stronger efforts to curb fentanyl flows, paused rare earth export controls for a year, and resumed purchases of US soybeans—significant given its historically large share of US export demand (chart 1). While not a comprehensive reset, these moves eased immediate tensions and helped avert more severe outcomes, including Trump’s previously threatened 100% tariff hike. The tone of the meeting also suggests a more conciliatory shift, though relations remain fragile and the risk of renewed escalation is still material.

Chart 1: US soybean exports

Beyond the headline-grabbing US–China trade deal, the APEC Summit in South Korea also saw the US reach a trade agreement with South Korea. Under the deal, US tariffs on South Korean autos and auto parts have fallen to 15% from 25%, matching the US tariff rate on Japanese autos and providing relief to South Korea’s sizable automotive export sector (chart 2). The agreement also clarified South Korea’s supposed $350 billion investment in the US: $200 billion in cash, capped at $20 billion per year to avoid currency market distortions, with the remaining $150 billion directed toward shipbuilding cooperation. While also not a major breakthrough, the deal represents incremental progress, addressing prior uncertainties and signalling steps toward a more favourable trade framework.

Chart 2: South Korea vehicle exports

US President Trump’s Japan Visit Turning to US President Trump’s visit to Japan last week, new Prime Minister Takaichi appears to have gotten off to a strong start, with Trump hailing US–Japan relations as entering a “NEW GOLDEN AGE.” The two countries signed several agreements, including a Technology Prosperity Deal, and deepened cooperation on critical minerals and rare earths. Japan’s previously vague $550 billion investment commitment in the US is now somewhat clearer: up to $332 billion will support critical US infrastructure, $30 billion will target AI, and $15 billion will go toward electronics and supply chains, among other areas. While the headline figure is substantial—even relative to Japan’s already significant direct investment assets in the US (chart 3)—the open-ended nature of the commitment and the lack of a clear timeline leave its actual impact uncertain.

Chart 3: Japan’s direct investment assets

The ASEAN summits Whilst US President Trump’s attendance at the ASEAN–US Summit in Malaysia dominated headlines, there were also several other notable developments at last week’s ASEAN meetings in Kuala Lumpur. Most prominently, Timor-Leste was officially admitted as ASEAN’s eleventh member, following a two-decade accession process during which the country actively aligned its political and economic frameworks with ASEAN standards. Membership grants Timor-Leste access to the bloc’s broader security and economic mechanisms and could open further avenues for trade, investment, and development cooperation. Nonetheless, the country still has considerable ground to make up relative to its new ASEAN peers, particularly in terms of both GDP and GDP per capita (chart 4).

Chart 4: ASEAN GDP per capita

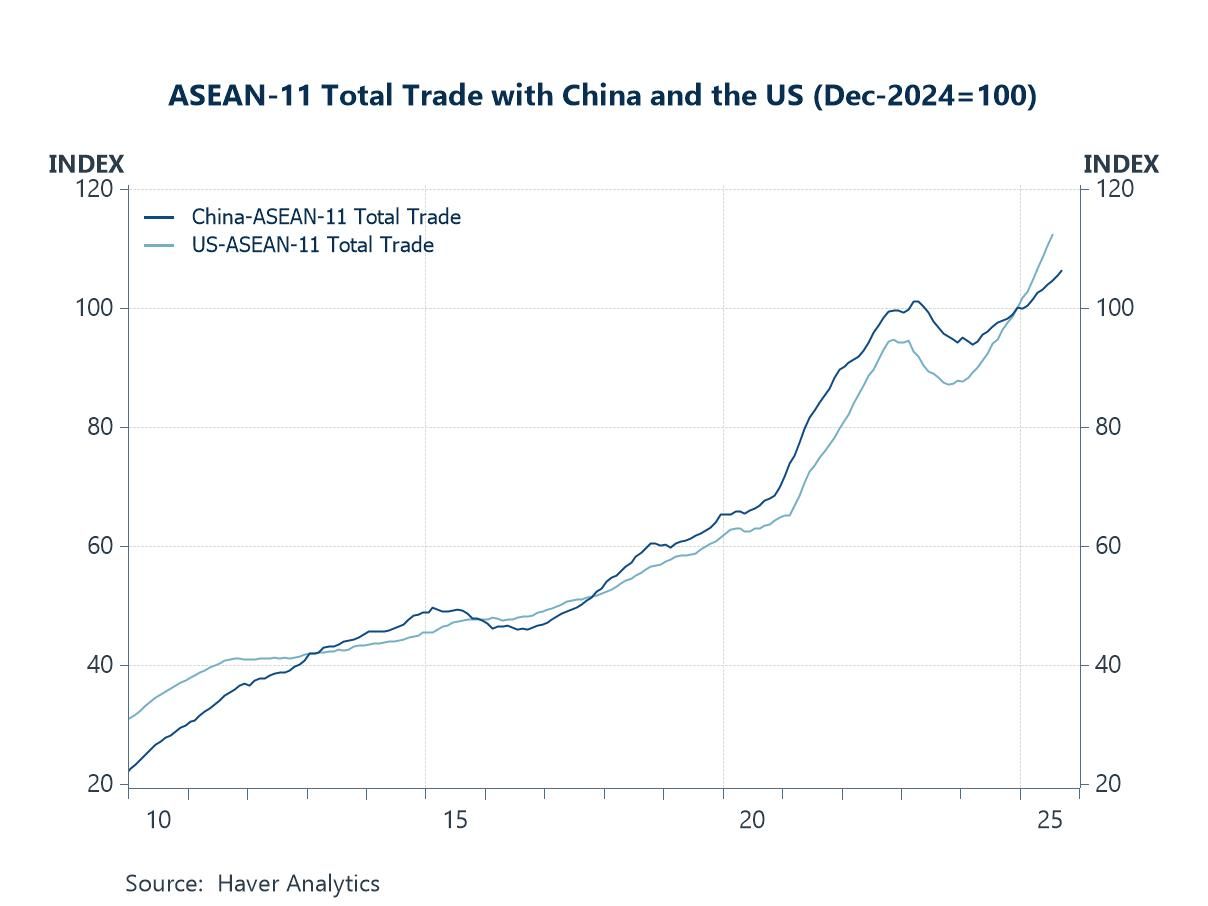

The accession of Timor-Leste into ASEAN aside, last week’s summits also brought a number of economic developments for the bloc. More concretely, ASEAN and China signed an upgrade to their free trade agreement last week, bringing the deal to so-called version 3.0. The upgraded deal (ACFTA 3.0) introduces commitments in new areas such as Digital Economy, Green Economy, and Supply Chain Connectivity, among other themes. And notably, just as the US and ASEAN have found common ground to collaborate in fields such as those relating to rare earths, given how the US has seen vulnerabilities arising from this space given China’s dominance in the field, China has taken the year’s US-China frictions to foster closer ties with its neighbours in the region, including the collectively sizable ASEAN bloc. Just by the trade dimension alone, China-ASEAN-11 trade has growth significantly this year (chart 2), although the economies’ total trade with the US also rose, and at a more significant pace, despite tariff measures.

Chart 5: ASEAN-11 total trade with China and the US

Looking ahead, investors will focus on a series of China-related releases this week, notably the Caixin PMI readings, as well as October trade and CPI inflation data. These indicators will help gauge the economy’s performance under ongoing US tariffs and assess domestic demand and supply conditions, all in the broader context of recent US–China interactions during Trump’s Asia tour. In Japan, attention will turn to updated data on employee wages and household spending, which—together with developments in the external environment—will shape expectations for the Bank of Japan’s future policy stance. Elsewhere in the region, investors will watch interest rate decisions from Australia and Malaysia, where rates are expected to remain unchanged, as well as GDP readings from Indonesia and the Philippines.

Chart 6: China exports by trading partner

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief