Global| Nov 06 2017

Global| Nov 06 2017New Orders Rise Again in Germany As EMU Service Sector Slows

Summary

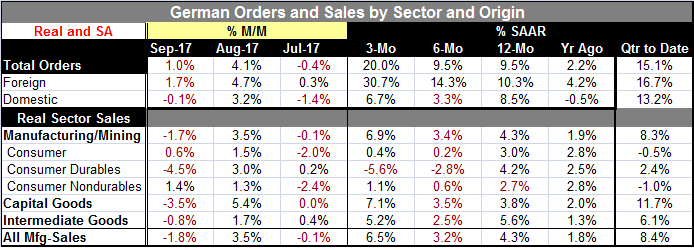

Germany's new orders rose by 1% in September with foreign orders gaining 1.7% and domestic orders slipping by 0.1%. Even so, domestic real orders rose to a point approximately level with orders before the start of the financial crisis [...]

Germany's new orders rose by 1% in September with foreign orders gaining 1.7% and domestic orders slipping by 0.1%. Even so, domestic real orders rose to a point approximately level with orders before the start of the financial crisis back in late-2007. Foreign orders had returned to pre-crisis levels by around mid-2014. Despite strong growth in Germany and its stellar economic statistics, German domestic orders are only now close to the sort of levels that had been common at the end of 2007.

Germany's new orders rose by 1% in September with foreign orders gaining 1.7% and domestic orders slipping by 0.1%. Even so, domestic real orders rose to a point approximately level with orders before the start of the financial crisis back in late-2007. Foreign orders had returned to pre-crisis levels by around mid-2014. Despite strong growth in Germany and its stellar economic statistics, German domestic orders are only now close to the sort of levels that had been common at the end of 2007.

Orders from outside the euro area fell by 1% while orders from other euro area member countries rose by a very strong 6.3%. Germany is benefiting from its competitiveness position inside the euro area as it has run the lowest inflation rates year-in and year-out since the common currency was established, putting Germany in a strong competitive lead against its fellow EMU members.

Still, the gain in orders on the month was only 1% overall. Manufacturers of intermediate goods saw new orders fall by 4.0% compared with August 2017. Manufacturers of capital goods showed an increase of 4.9% on the previous month, marking capital goods as the engine of growth this month. For consumer goods, new orders fell by 2.8%, despite the strong performance of the German economy and an expansion of orders from abroad. The consumer is not leading this parade. And with German domestic orders only now getting back to their 2007 level, it is hard to believe that there are bottlenecks requiring investment anywhere unless the capital stock has withered due to atrophy over the last 10 years.

However, orders overall are ramping up from three-month and six-month rates of growth at 9.5% to a pace of 20% over three months. Foreign orders have ramped up on growth rates from 10.3% to 14.3% to 30.7% on the same timeline. German domestic orders were falling one year ago on a year-over-year basis. They are now up by 8.5% year-on-year but up on a 3.3% pace over six months. Domestic orders' three-month growth rate is up to 6.7%, however. It's been a long time coming, but there is some lift there.

Overall there is a sense of expansion and acceleration in the data. Still, the long view is not that these growth rates are putting German industry to the test. Growth in Germany is still moderate even of orders are stepping up. Sales by sector show that the overall sales pace in manufacturing fell in the month despite the order pick up. Consumer goods shipments rose even as capital and intermediate goods shipments declined. Capital goods shipments fell in September after spurting in August; and still remain strong over the two months together.

The longer view on sales/shipments is that sales are up from a 3.5% to 4% pace over 12 months and six months to an accelerated 6% to 7% pace in September.

In the quarter-to-date, overall orders as well as domestic and foreign orders are expanding at a pace of about 15% annualized. By sector all sales are up except for consumer goods where nondurables are the drag on expansion. With the third quarter data complete, Q3 sales are strongest for capital goods (11.7%) and intermediate goods (6.1%) while consumer goods sales erode at a 0.5% pace.

On balance, the report for German orders was better than expected since a decline in orders was the mainline forecast for September. Instead, orders rose on the month and are rising briskly over three months. Judging from the orders received from the rest of the euro area, the entire region seems to be doing relatively well despite a minor setback in the services PMIs reported today.

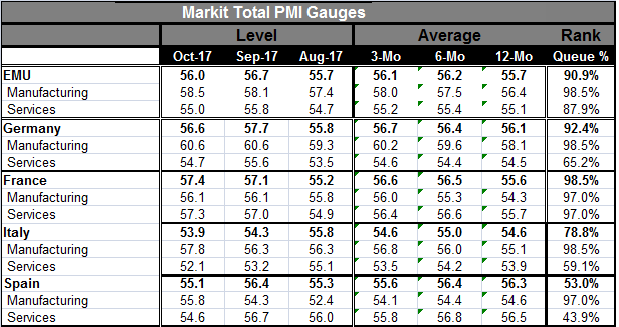

In today's reports, the EMU services sector in October lost its 90th percentile standing and the German services sector stepped back again to a 54.7 diffusion value and a 65.2 percentile standing since January 2012. Among the four largest EMU economies, only France has a particularly strong service sector ranking; Germany, Italy and Spain show weaker performance with Spain posting a service sector reading below is median since January 2012. Manufacturing sector metrics remain especially strong. But the services sector is beginning to show some softness at least among the largest EMU economies.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief