Global| Jul 23 2018

Global| Jul 23 2018Monthly Greek Current Account Swings to Surplus

Summary

The Greek current account in May swung to surplus, its fourth surplus in the last 12 months. It is the fourth largest monthly current account surplus for Greece back to January 2002. Since that time, the Greek current account has been [...]

The Greek current account in May swung to surplus, its fourth surplus in the last 12 months. It is the fourth largest monthly current account surplus for Greece back to January 2002. Since that time, the Greek current account has been in surplus about 8.5% of the time. However, this has speed up since the current account has been in surplus 33% of the time in the past 12 months.

The Greek current account in May swung to surplus, its fourth surplus in the last 12 months. It is the fourth largest monthly current account surplus for Greece back to January 2002. Since that time, the Greek current account has been in surplus about 8.5% of the time. However, this has speed up since the current account has been in surplus 33% of the time in the past 12 months.

Just since 2012, Greece began to post sporadic current account surpluses following a legacy of never-ending deficits. By March 2014, Greece had experienced four (current account) surpluses in the last 12 months for the first time in years. By April 2015, this count was down to one surplus in the last 12 months. By December 2015, the count was back up to five surpluses in the last 12 months as the surpluses transitioned in and out of greater frequency. The 12-month surplus count dipped back to one in 12 months in late-2016 and the count has been rising since then. In 2018, there is a clustering of months with three to four current account surpluses out of the last 12 as Greece appears to be making more persistent balance of payments progress.

Since about 2012, the Greek current account position has generated mostly small deficits with a smattering of surpluses.

The Great Recession and financial crisis period set Greek back dramatically as it dealt with never-ending austerity programs. Greek debt remains a load that is probably too heavy for it to bear. However, the Greek economy has stabilized and is growing more persistently. Recently, it has accelerated.

The Great Recession and financial crisis period set Greek back dramatically as it dealt with never-ending austerity programs. Greek debt remains a load that is probably too heavy for it to bear. However, the Greek economy has stabilized and is growing more persistently. Recently, it has accelerated.

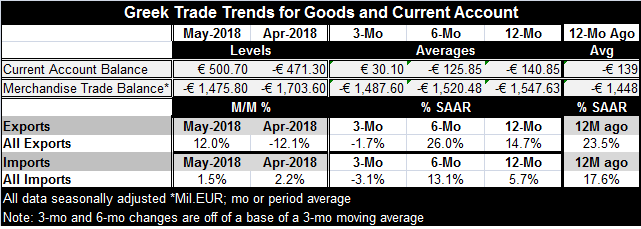

Greek exports and imports show similar trends. Both are up substantially over 12 months although with the export growth rate nearly three times that of the import growth rate. Over three months, both exports and imports are falling, but imports are falling nearly twice as fast as exports. These trends have produced trade and current account improvement for Greece.

Greece’s improvement is real. But its future is still clouded. Migrant issues still hammer the economy and the EU has yet to really provide enough assistance for Greece to deal with the influx. The new government in Italy has taken a more aggressive stance rejecting migrants saved at sea. And this has put more pressure on Italy’s neighbors to absorb more and on the EU to take steps to deal with the issue. But it remains an active issue. Germany held up the final tranche of Greece’s payment because the VAT tax hike scheduled for five of the Greek islands was going to be postponed to give them more resources to deal with the influx of migrants (Lesvos, Chios, Samos, Kos and Leros). Germany balked the funds transfer but ultimately did not block it but did ask for the revenue loss to be recaptured through other means. Greece’s debt load remains heavy but interest payments have been stopped putting the day of reckoning off in the future. Former government official Yanis Varoufakis said: "Congratulations, comrades. (Eurozone creditors) extend the Greek state's bankruptcy into 2060 and they call it debt... relief." His assessment is not incorrect.

Greece’s eight-year crisis toppled four governments and shrank the economy by 25%. Unemployment rose to 20.2% in April from 20.1% in March, the highest rate of any euro area member. Greek unemployment has been higher since 1991 only about 32% of the time. Greece is still under pressure from its creditors, and has already agreed to slash pensions again in 2019, and reduce the tax-free income threshold for millions of people in 2020.

But the progress in its trade account is a good sign that Greek competitiveness is coming back to square with global standards. Of course, the future will depend a lot on the ongoing global trade disputes which have Greece on the sidelines but still not unaffected. Greece’s exit from being under a bail out condition in August is good news, but it is not a clean bill of health. Despite all the pain and suffering that Greece has undergone, it still has a very fine line to walk to stay out of financial difficulty.

IMF Managing Director Christine Lagarde said this: "In the medium term analysis there is no doubt in our minds that Greece will be able to reaccess the markets. As far as the longer term is concerned we have concerns." Still, it’s a better situation than Greece has been in for a long time.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief