Global| Sep 25 2009

Global| Sep 25 2009Money Supplies: Weakening, Surprise!

Summary

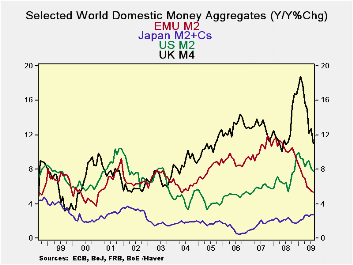

Year-over-year most money supply measures for key countries are still showing solid-to-too-strong growth. The UK is at 11% and the US at 7.8% compared to Japan at 2.8% and EMU at 5.3%. But the developing story is the decay in monetary [...]

Year-over-year most money supply measures for key countries are still showing solid-to-too-strong growth. The UK is at 11% and the US at 7.8% compared to Japan at 2.8% and EMU at 5.3%. But the developing story is the decay in monetary growth rates and continued weakening credit growth. After pumping out a lot of liquidity in the crisis that same liquidity has to be mopped up. But that is not exactly what is going on, as most of the US ‘liquidity injection’ is still sloshing around on bank balance sheets. In the US bank reserves were expanded greatly but there the story is despite all the ‘excess liquidity’ in the banking system, money growth is decelerating sharply. The high powered money in banks is excessive but what is in the hands of the main economic transactors is growing slowly. US M2 growth has gone from growth of 6.8% Yr/Yr to -2.2% at annual rate over three-months or from 9.4% in real terms to a real 3-month annualized growth rate of -6.8%. The turnaround in the UK is nearly as dramatic. Of course, the US and the UK are banking centers.

IN EMU the story is flat and moderate money growth: 5.3% Yr/Yr and a 5.4% annual rate over three-months. Money supply in the EMU region did not really react that much to the crisis. It had peaked in October 2007 and has been gradually stepping down since then, accelerating its drop since November of 2008. In real terms there is a drop off in EMU money growth from 5.5% Yr-over-year to a three month real annualized rate of growth of 3.4%. At the same time residential credit and loans growth rates have decelerated in EMU. Over three-months residential credit is up at an annual rate of 1% and loans are contracting at an annual rate of 1.3%. In real terms, of course the slowing is even more dramatic and real credit balances are contracting as are real loan balances. Nominal loans to corporations and households are the weakest they have ever been in EMU since data began being collected in 1991.

Year-over-year growth rates for money are contracting in all major monetary centers except in Japan. The most severe Yr/Yr decelerations are in EMU and in the UK. The US deceleration is nascent and has not hit the Yr/Yr profile that hard (see chart).

Much of the problem is the growth of loans. If banks are going to be very tight fisted then the money multiplier will not be a stimulative. Banks have been very cautious in underwriting new credit demands. This remains one of the main obstacles to getting recovery into higher gear in Europe, in the US and in Japan.

| Saar-all | Euro Measures (E13): Money & Credit | G-10 Major Markets: Money | Memo | ||||

| €€-Supply M2 | Credit:Resid | Loans | $US M2 | ££UK M4 | ¥¥Jpn M2+Cds | OIL:WTI | |

| 3-MO | 5.4% | 1.0% | -1.3% | -2.2% | 3.2% | 2.8% | 116.4% |

| 6-MO | 3.1% | -0.6% | -1.9% | 0.8% | 0.5% | 3.1% | 231.6% |

| 12-MO | 5.3% | 2.2% | 0.2% | 7.8% | 11.0% | 2.8% | -39.2% |

| 2-Yr | 7.6% | 6.6% | 4.5% | 6.6% | 11.1% | 2.6% | -1.0% |

| 3-Yr | 8.7% | 8.2% | 6.6% | 6.5% | 12.0% | 2.3% | -0.9% |

| Real Balances: deflated by Own CPI. Oil deflated by US CPI | |||||||

| 3-MO | 3.4% | -1.0% | -3.3% | -6.8% | -0.4% | 4.0% | 106.4% |

| 6-MO | 2.4% | -1.2% | -2.5% | -1.4% | -1.8% | 4.7% | 224.2% |

| 12-MO | 5.5% | 2.3% | 0.4% | 9.4% | 9.3% | 5.0% | -38.3% |

| 2-Yr | 5.7% | 4.7% | 2.6% | 4.6% | 7.7% | 2.6% | -2.8% |

| 3-Yr | 6.8% | 6.3% | 4.7% | 4.5% | 9.0% | 2.4% | -2.8% |

| Japan CPI for Aug is an estimate; it uses the July value to produce the real balance figure | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief