Global| Feb 27 2008

Global| Feb 27 2008Money and Credit Trend in Euro Area Remain Robust…

Summary

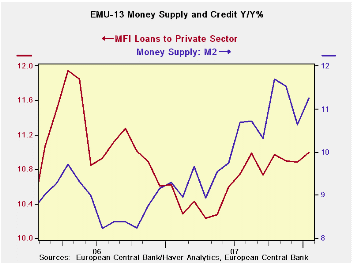

The table below shows Euro area money and credit growth comparing it to money growth in several key countries. We also provide data on real balances (inflation-adjusted money and credit). Despite ongoing financial turmoil, here data [...]

The table below shows Euro area money and credit growth comparing it to money growth in several key countries. We also provide data on real balances (inflation-adjusted money and credit). Despite ongoing financial turmoil, here data show that there has been little slowing in EMU money and credit. Credit to residents has slowed a touch over the three months compared to six-month and one-year rates. Overall business loan growth in EMU has barely slowed.

Money growth has held up around the various main global money centers as well. Unexpectedly, the growth in real money in EMU has been stronger than in the US where it is off by 0.1% over three months. Over 12 months US M2 is up at just a pace of 1.4% compared to 7.9% in the EMU. Real money growth in the UK is quite steady. In Japan real money growth is slow but is being held fairly steady.

The memo item on the right of the table shows how relentless the rise has been in the price of crude oil in these various periods. Central banks have done a really impressive job in running policy amid this ongoing energy shock as well and a new shock stemming from food prices.

Judging by interest rate policy, monetary policy in the US is loose. But judging from the growth in real balances, US monetary policy is tighter than in UK, EMU or Japan over three months and tied with Japan for stringency over the past year.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief