Global| Aug 27 2020

Global| Aug 27 2020Money and Credit Growth Respond to Stimulus...And to Distress

Summary

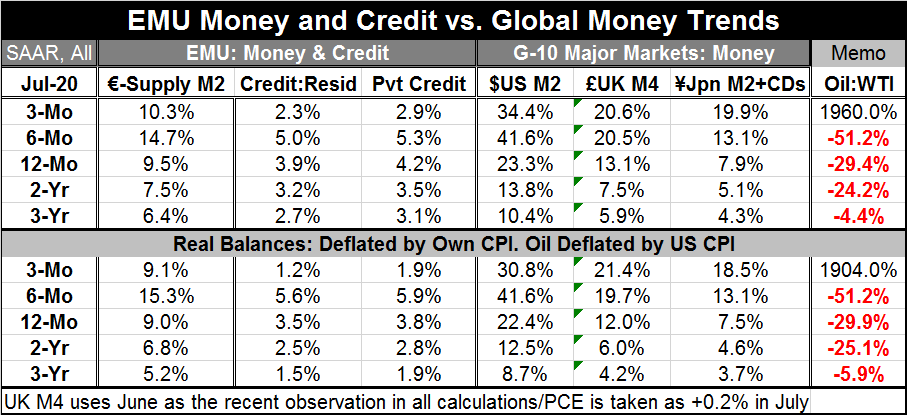

Money supply in EMU has surged showing annualized double-digit rates of growth over three months and six months, and nearly so over 12 months (9.5%). And while year-on-year credit growth has accelerated on 12-month growth rates (see [...]

Money supply in EMU has surged showing annualized double-digit rates of growth over three months and six months, and nearly so over 12 months (9.5%). And while year-on-year credit growth has accelerated on 12-month growth rates (see table) even as sequential credit growth has accelerated, it has then decelerated with the three-month growth rate below the credit growth rates for six-months, 12-months, two-years and even three-years. The same is true of private credit expansion. While money supply growth also dipped over three months compared to over six months, it is still higher than the longer horizon growth rates. Money growth has accelerated much more than has credit growth.

Money supply in EMU has surged showing annualized double-digit rates of growth over three months and six months, and nearly so over 12 months (9.5%). And while year-on-year credit growth has accelerated on 12-month growth rates (see table) even as sequential credit growth has accelerated, it has then decelerated with the three-month growth rate below the credit growth rates for six-months, 12-months, two-years and even three-years. The same is true of private credit expansion. While money supply growth also dipped over three months compared to over six months, it is still higher than the longer horizon growth rates. Money growth has accelerated much more than has credit growth.

A further problem is that credit growth is not a pure indicator of 'stimulus.' Europe, as well as globally, there is a great deal of dislocation and credit use may not be capturing new credit to expand business or to support new spending as much as it is credit serving as a replacement to a flow of income that used to be generated by a company's normal flow of business or a person's normal spending. This sort of distortion is less relevant in a country like Germany where funds are being topped up at the firm level by the government and employees are being carried and are still fully employed even if not working. In the U.S., the sense of dislocation is much larger. Some firms retained labor using the payroll protection program. Many others did not. Upon being let go, workers filed for unemployment insurance and were paid that plus extra monies according to several support programs for workers. But in the process, many workers would lose certain benefits including health care protection which is not what you want to lose in the middle of a pandemic. In any case, in such an environment credit is a little less meaningful and what we see in the EMU with nations taking various approaches to helping firms and workers absorb the shock of the virus and of economic shutdowns is that growth has been hit hard, unemployment rates are still rising and there is still dislocation. The increase in credit clearly is a patch to make up for what has been lost much more than a new slug of stimulus and spending.

Globally the impact on money growth has been building with the U.S. seeing the fastest increase in money supply by far followed at some distance by the U.K. then EMU where growth is fading and by Japan. Meanwhile, economic growth is still erratic and inflation is subdued.

Growth rates for real money balances show slowing for the EMU and the U.S. compared to ongoing acceleration in the U.K. and in Japan.

The role of oil is hard to pin down. The oil price, as measured here by WTI, shows declines over all horizons except the shortest. On that horizon, oil prices are up by more than 100% in raw terms and accelerating at warp speed at a nearly 2000% annual rate over three months.

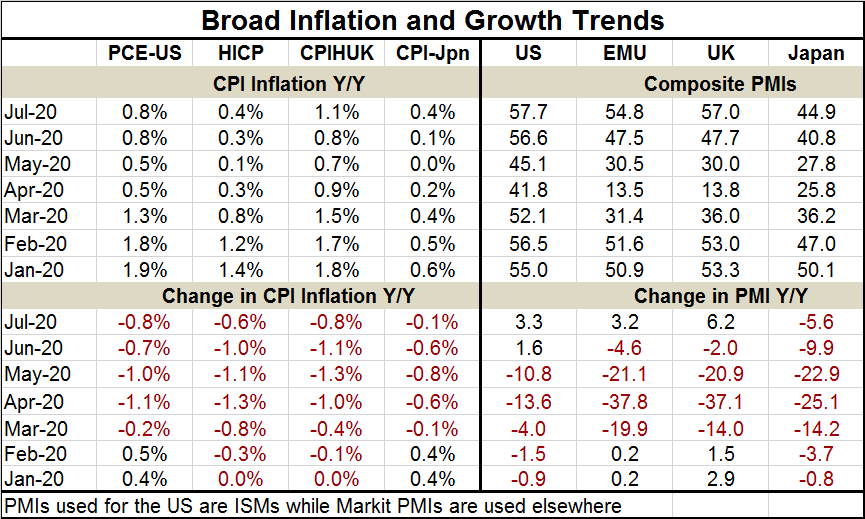

Still, for these four economic units, inflation is falling year-over-year in each and has been doing so for at least four months in a row. The pace of inflation over 12 months is in the vicinity of 1% to 0.5% for all four countries or regions. Money growth as stimulus and the government programs to support growth are still fighting what is not yet a winning battle against weakening growth.

The virus continues to spread; this malaise is defying all countries even those that initially had the best performance against it. While the virus kills very few, it has a high impact on people with certain preexisting conditions and it may in fact inflict others with health problems that will emerge later. The global approach has been to keep infection rates low except in Sweden where progress toward getting what is called 'natural herd immunity' is well underway. In countries that have had success fighting the virus, that 'success' means that their nationwide infection rate has been kept low and that in turn means its vulnerability nationwide to a new round of infections is high. That is why the shelter-in-place/lockdown/hide-from-it strategies are not long-run solutions. The only long-run solution is what Sweden is doing or it depends on a workable broad vaccine being discovered. Even then manufacturing and distribution of a vaccine will take time. We are going to continue to struggle with this virus for some time. It is not clear that national policies have some to grips with that fact. In the U.S., economic policies continue to be adopted on hand to mouth basis or worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief