Global| Oct 28 2015

Global| Oct 28 2015Migrant Issues Whack German Sentiment; Other Issues Clobber Sentiment Worldwide

Summary

GfK reports this month that concerns over the impact of migrants in Germany have set back the expected confidence reading for November. But the lagging components of the index show the sharpest drop is in economic expectations. [...]

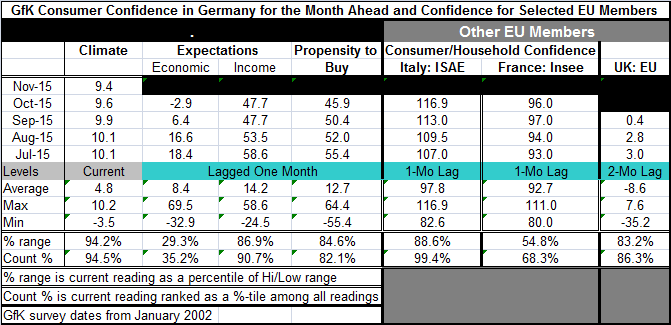

GfK reports this month that concerns over the impact of migrants in Germany have set back the expected confidence reading for November. But the lagging components of the index show the sharpest drop is in economic expectations. Expectations drop from +6.4 in September to -2.9 in October. The November reading is not yet available. But the economic reading was 18.4 as recently as July. The October economic expectations reading resides in the 35th percentile of its historic queue of data, a decidedly weak standing and one that is quite out of step with the standing of the headline reading itself as well as the other components.

GfK reports this month that concerns over the impact of migrants in Germany have set back the expected confidence reading for November. But the lagging components of the index show the sharpest drop is in economic expectations. Expectations drop from +6.4 in September to -2.9 in October. The November reading is not yet available. But the economic reading was 18.4 as recently as July. The October economic expectations reading resides in the 35th percentile of its historic queue of data, a decidedly weak standing and one that is quite out of step with the standing of the headline reading itself as well as the other components.

Income expectations in October were flat at their September level. The propensity to buy reading fell in October to 45.9 from 50.4 in September. All the components have been losing ground since July.

However, the standing of the GfK November reading is still in the 94.5 percentile of its historic queue of data, a quite strong reading, albeit lower than any reading since February. Income expectations stand in their 86.9 queue percentile and the propensity to buy metric sits in its 82.1 queue percentile. At the 35th percentile, the economic expectation reading is really leading the way lower.

Two other large EMU member countries report sentiment for October. Italy is the odd man out, showing a rise in sentiment to 116.9 from September's 113.0. France shows a backtracking to 96 in October from 97 in September. The U.K. measure that lags by two months slowed in August. Italy's reading is strong standing in the top 1% of its historic queue of data. France's sentiment stands only in its 68th percentile, a moderately firm reading. The one-month-older U.K. measure stands in its 86th queue percentile.

There are, however, more sentiment indicators that were released today and the news on the whole is not good. Japan's small business confidence indicator fell unexpectedly to 48.7 in October from 49 in September. And the Westpac-MNI consumer sentiment index for China fell to 109.7 from 118.2, an extremely sharp drop. This is the weakest reading by this index since it was launched in 2007.

Sentiment readings are interesting indicators. Consumer sentiment, for example, will be based on a broad array of data that the consumer knows firsthand. For example, consumers know if the firm where they work is hiring or firing. Salesmen know if they have earned a commission even if it has not yet been paid. Consumers know if homes on the block where they live are for sale and if they are selling for a good price or not. In sum, consumers have a broad array of information about the economy that can be used to help answer broad, but not quantitative, questions about the economy. And their information is up to the minute, unlike government surveys that are month old at best, and even then, in all likelihood still `preliminary.' Sentiment does get substantially revised.

Today's sentiment readings should give us pause. Yesterday the Conference Board consumer confidence index in the U.S. fell sharply and the drop exceeded expectations. Consumers around the world are seeing things they do not like and they are seeing these things in recent months.

While GfK attributed some of the drop in expectations to the migrant crisis, there are more fundamental concerns afoot too even in Germany. Consumer expectations slid to a negative reading for the first time since May 2013. The weakness in economic expectations reflects in part concerns felt by many German citizens that the labor market will worsen in the coming months. About 44% of respondents believe that unemployment will rise or rise significantly over the next few months versus 22% with that expectation in July.

Clearly, a multiplicity of factors is buffering the global economy. Consumers can feel it from China to the EMU strong-man, Germany, to the United States where the Fed had been on the verge of hiking rates.and maybe still is. But in these varied reports today, there is little evidence of any economy anywhere really gaining any traction. As one day's data go, today's reports are about as consistent and one-way as it will ever get. And the news is not good.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief