Global| Feb 05 2007

Global| Feb 05 2007Michigan Consumer Sentiment Firm for January

by:Tom Moeller

|in:Economy in Brief

Summary

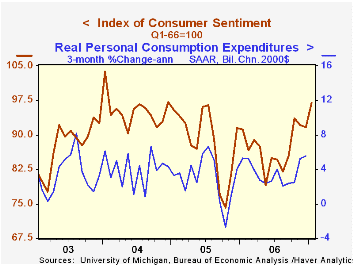

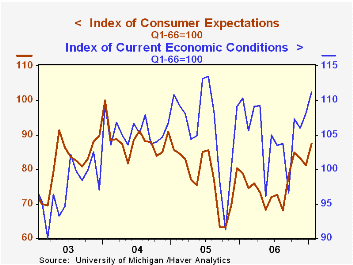

The University of Michigan's final reading of consumer sentiment during January remained quite solid versus December at 96.9 (Q1 1966 = 100). The reading fell, however, from the mid-month read of 98.0. The reading of current [...]

The University of Michigan's final reading of consumer sentiment during January remained quite solid versus December at 96.9 (Q1 1966 = 100). The reading fell, however, from the mid-month read of 98.0.

The reading of current conditions increased to 111.3 from December's 108.1, up 3.0% after a 2.0 rise during that month.

Consumers' reading of personal finances rose 3.4%, the firmest rise in three months, as the sense of buying conditions for large household goods rose 3.1% after a 3.2% December gain.

The expectations component recouped all of the decline during the prior two months with a 7.9% increase and the rise was to the highest level since 2004. Expected business conditions surge 12.4% and expected personal finances rose 2.4% (5.8% y/y).

Consumers' assessment of government policy and performance rose to the highest level since 2005 but expectations about inflation during the next twelve months rose slightly to 3.6%.

The University of Michigan survey is not seasonally adjusted.This mid-month survey was based on telephone interviews with about 340 households nationwide on personal finances and business and buying conditions. The survey is expanded to a total of 500 interviews at month-end.

| University of Michigan | January (Final) | January (Prelim.) | December | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 96.9 | 98.0 | 91.7 | 6.3% | 87.3 | 88.6 | 95.2 |

| Current Conditions | 111.3 | 112.5 | 108.1 | 0.9% | 105.1 | 105.9 | 105.6 |

| Expectations | 87.6 | 88.7 | 81.2 | 11.0% | 75.9 | 77.4 | 88.5 |

by Tom Moeller February 5, 2007

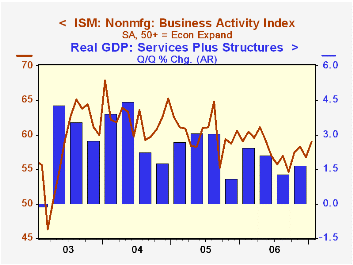

The non-manufacturing sector Business Activity Index rose more than expected to 59.0 last month and more than reversed the 1.6 point decline during December. Consensus estimates had been for a lesser gain to 57.0 and the figures from the Institute for Supply Management were revised to reflect revisions to seasonal factors.

The figure contrasts with the 2.1 point deterioration in the NAPM composite manufacturing index of factory sector activity for January.

Since the series' inception in 1997 there has been a 46% correlation between the level of the Business Activity Index and the q/q change in real GDP for services plus construction.

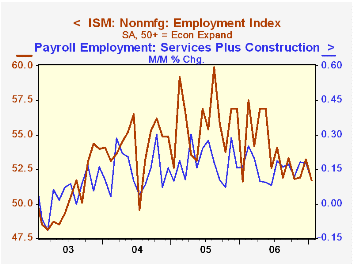

The new orders sub-index and the employment index both fell during January, employment to the lowest level in a year. Since the series' inception in 1997 there has been a 56% correlation between the level of the ISM non-manufacturing employment index and the m/m change in payroll employment in the service producing plus the construction industries.

Pricing power deteriorated a sharp 4.5 points to 55.2, the lowest level since October. Since inception eight years ago, there has been a 70% correlation between the price index and the y/y change in the GDP services chain price index.

ISM surveys more than 370 purchasing managers in more than 62 industries including construction, law firms, hospitals, government and retailers. The non-manufacturing survey dates back to July 1997.Business Activity Index for the non-manufacturing sector reflects a question separate from the subgroups mentioned above. In contrast, the NAPM manufacturing sector composite index is a weighted average five components.

| ISM Nonmanufacturing Survey | January | December | Jan. '06 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Business Activity Index | 59.0 | 56.7 | 59.1 | 58.0 | 60.2 | 62.5 |

| Prices Index | 55.2 | 59.7 | 67.8 | 65.2 | 68.0 | 68.8 |

by Tom Moeller February 5, 2007

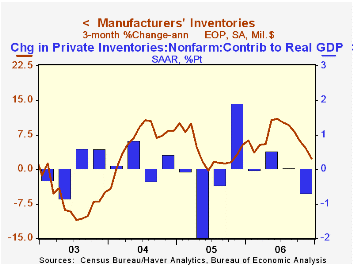

Factory inventories inched up just 0.1% during December after a slowed 0.2% November gain. The 0.6% increase in factory inventories during 4Q06 was the slowest since 3Q05.

Primary metals inventories actually fell during the last two months (+17.9% y/y). Automobile inventories also plummeted 11.8% (+6.3% y/y) and inventories of furniture fell 1.5% (+4.3% y/y). These declines were offset by higher electrical equipment inventories (11.3% y/y), higher inventories of computers (+8.4% y/y) and higher machinery inventories (8.7% y/y).

Total factory orders rose a firm 2.4% following a downwardly revised 1.2% November increase. Durable goods orders surged 2.9% which was little revised from the advance report of a 3.1% pop. Factory orders less transportation surged 2.2% (2.4% y/y) though nondurable are even y/y reflecting lower oil prices but also a decline in textiles.

Factory shipments surged 1.4% reflecting a 1.0% jump in durables which was broad based. Factory shipments less transportation jumped 1.0% (1.0% y/y).

Unfilled orders surged 2.1% due to the another jump in civilian aircraft (39.5% y/y). Less the transportation sector altogether backlogs rose 1.3% (13.8% y/y).

| Factory Survey (NAICS) | December | November | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Inventories | 0.1% | 0.2% | 6.7% | 6.7% | 4.0% | 6.9% |

| New Orders | 2.4% | 1.2% | 1.3% | 5.4% | 8.5% | 7.5% |

| Shipments | 1.4% | 0.2% | 0.4% | 4.7% | 7.1% | 6.8% |

| Unfilled Orders | 2.1% | 1.8% | 20.4% | 20.4% | 16.3% | 4.5% |

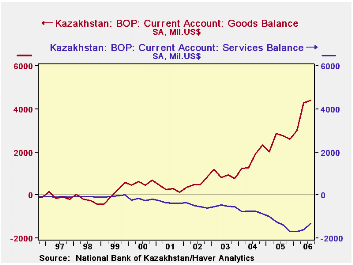

by Louise Curley February 5, 2007

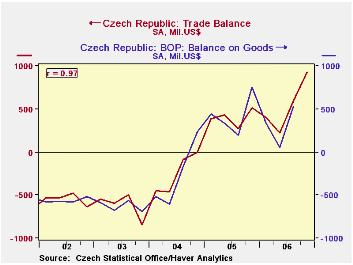

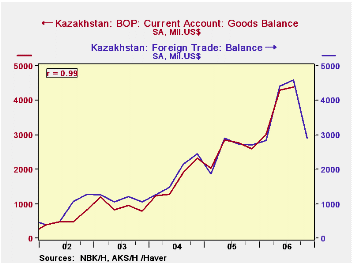

The Czech Republic and Kazakhstan released data on exports and imports of goods for December. The data for the Czech Republic are in Koruny and US dollars; that of Kazakhstan in US Dollars only. The monthly trade in goods when aggregated quarterly should equal the quarterly data reported in the balance of payments. The fact that they do not equal is probably due to differences in timing. The two series are, however, close as the high correlations between the two series indicate. (See the first two charts)

The monthly data for the Czech Republic suggest that the balance of payments data should show a sharp rise in the goods balance in the fourth quarter. The monthly data for Kazakhstan, on the contrary, suggest a sharp decline in the goods balance reported in the balance of payments.

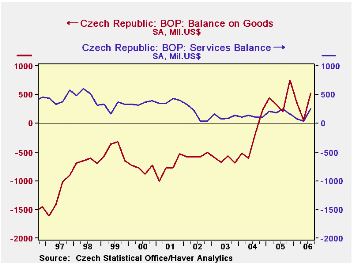

Taking a somewhat longer look and including the balance on services, we find that the Czech Republic has traditionally had a deficit on goods and a surplus on services. It is just since late 2004 that the Republic has had a surplus on trade in goods (as can be seen in the third chart). Ever since mid 1999 Kazakhstan has had a surplus on trade in goods and a deficit on trade in services as seen in the fourth chart. Since mid 2002, the balance on goods has more than offset the deficit on services.

| TRADE IN GOODS (Millions of U.S.$) | Dec 06 | Nov 06 | Oct 06 | Q4 06 | Q3 06 | Q2 06 | Q1 06 |

|---|---|---|---|---|---|---|---|

| Czech Republic | |||||||

| Balance on Goods (Monthly data) | 492 | 168 | 266 | 927 | 599 | 226 | 404 |

| Balance on Goods (Quarterly data) | -- | -- | -- | -- | 528 | 50 | 340 |

| Kazakhstan | |||||||

| Balance on Goods (Monthly data) | 1099 | 1093 | 697 | 2888 | 4599 | 4411 | 2828 |

| Balance on Goods (Quarterly data) | -- | -- | -- | -- | 4399 | 4296 | 3007 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.