Global| Jul 01 2015

Global| Jul 01 2015Markit Manufacturing Indices Are Mixed in June; Conditions Turn Up in EMU

Summary

Globally, the manufacturing PMI picture is mixed. Of the 10 countries or areas (excluding Germany and France as they are part of the EMU), six are below 50 in June. Except for China, these weak reporters are also relatively small [...]

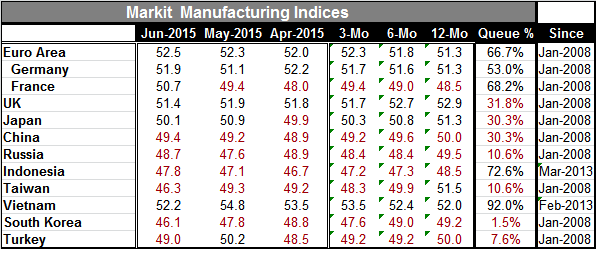

Globally, the manufacturing PMI picture is mixed. Of the 10 countries or areas (excluding Germany and France as they are part of the EMU), six are below 50 in June. Except for China, these weak reporters are also relatively small countries. But the picture of an irregular manufacturing sector is real. Although the large countries tend to be expanding, their PMI values are uniformly low. The highest manufacturing PMI value in the table is the 52.5 reading in the EMU, followed by 52.2 for Vietnam. Manufacturing is strong nowhere in this table.

Globally, the manufacturing PMI picture is mixed. Of the 10 countries or areas (excluding Germany and France as they are part of the EMU), six are below 50 in June. Except for China, these weak reporters are also relatively small countries. But the picture of an irregular manufacturing sector is real. Although the large countries tend to be expanding, their PMI values are uniformly low. The highest manufacturing PMI value in the table is the 52.5 reading in the EMU, followed by 52.2 for Vietnam. Manufacturing is strong nowhere in this table.

That story is also told by the percentile standings. These are somewhat less meaningful, however, since many of the countries in the table have very short-time series of data on their manufacturing PMI measures. For comparability, we chronicle all these values from 2008 or even later (Indonesia and Vietnam from 2013). A longer time series gives the percentile standing more meaning. Even for this truncated set of measures, we are measuring performance since 2008, which is a period of extreme economic duress, and still we get, by and large, relatively weak contemporaneous readings!

We see weak values being reported currently with few exceptions. Vietnam, with a very short history, appears strong (92nd percentile), but this on a diffusion value of only 52.2, for which such a high standing should be suspect. It is the product or a poor history for comparisons (a history of weakness) and what is a really a moderate current reading. Indonesia is moderate at a 72nd percentile. France, Germany and the EMU are moderate or weakly moderate. For the rest, we see the U.K., Japan and China in the lower one third of their respective queues since 2008. Russia and Taiwan are at the border on their lower 10% standing. And South Korea and Turkey are even weaker.

These are poor standings in absolute terms and extremely poor standings for the times, in what should be the recovery period from a major recession. On top of that, there is very little upward momentum.

Greece failed to make payments to the IMF, but the credit rating agencies do not call it a default. Greece has tried to propose another deal. While Germany has said the door is open, it has registered skepticism over reports of this new proposal from Greece. Angela Merkel has already said she would not negotiate with Greece as long as there is a referendum pending. And there is a referendum pending.

There is no surprise that markets are confused about all of this. Markets are trading higher on news that Greece has a new proposal. Nevertheless, we can be sure that Europe is not interested in negotiating with Alex Tsipras any more. Some think Europe would torpedo any new negotiations just to make Greece vote in its referendum on a proposal that, if it is rejected, would send Greece out of the euro area and, if it is accepted, would likely result in the ejection of the Tsipras government from power.

While that view may be a bit cynical, it is true that Merkel has said she would not negotiate with a referendum pending. To that extent, the Tsipras offering is totally rejecting conditions that a key European country has put on further negotiations.

To say that market conditions are a mess is to downplay the state of uncertainty. Markets are coming up from sold off levels on what they hope will be good news. At the end of the day, no one really thinks Greece wants to leave the EMU, but these negotiations have been full of misappraisals or we would not be where we are now. Be careful using logical in an intrinsically illogical situation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief