Global| Apr 17 2009

Global| Apr 17 2009MAPI Survey Indicates Deepening Stress in the Factory Sector

by:Tom Moeller

|in:Economy in Brief

Summary

The manufacturing sector will remain distressed. That is the message reported yesterday in the Manufacturers Alliance/MAPI survey of the factory sector. Their composite index of activity fell to a record low level as it dropped to 21 [...]

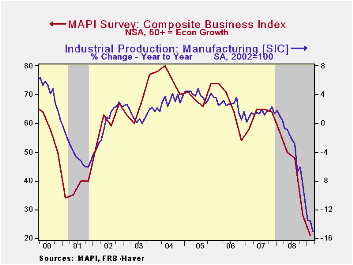

The manufacturing sector will remain distressed. That is the message reported yesterday in the Manufacturers Alliance/MAPI survey of the factory sector. Their composite index of activity fell to a record low level as it dropped to 21 from 28 in 4Q08. Both these readings were down substantially from early last year when the index stood at 57. (The figures are diffusion indexes thus any level below 50 indicates declining activity.)

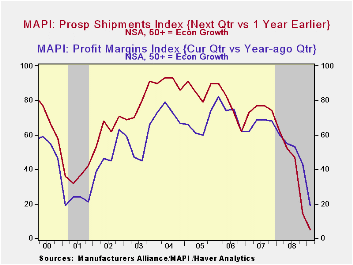

The component series measuring prospective shipments fell to a record low level of 5 as only 2 percent of survey respondents expected shipments to rise. That low reading was backed up by a record low level of the orders index. It fell to 4 as only 2 percent of respondents expected higher orders. And the low level of activity is drawing down the level of order backlogs. As the index fell to a record low reading of 14 it reflected only 8 percent of respondents reporting higher unfilled orders but 80 percent reporting a lower level.

Lower factory sector activity has weighed heavily on profitability. Fully 75 percent of respondents indicated that profit margins fell versus early last year while just 13 percent reported a higher reading. The overall diffusion index fell to a low 19, or one-third the level of last year, as business activity has fallen faster than costs. And lower profits weighed heavily capital spending. Fully 79 percent of respondents cut spending while just 8 percent raised it versus one year ago. The index of R&D spending similarly fell to a record low.

The MAPI data is not seasonally adjusted and the diffusion indexes measure activity in the current quarter versus the same quarter one year earlier. The component weights in the composite are given below in parentheses. The data can be found in Haver's SURVEYS database.

After the Crisis is yesterday's speech by Dennis P. Lockhart, President and Chief Executive Officer, Federal Reserve Bank of Atlanta and it can be found here.

| Manufacturers Alliance/MAPI Survey (NSA) | 1Q 2009 | 4Q 2008 | 1Q 2008 | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Composite Business Index | 21 | 28 | 57 | 46 | 63 | 66 |

| Prospective Shipments (0.4) | 5 | 14 | 62 | 44 | 75 | 77 |

| Backlogs Index (0.2) | 14 | 21 | 21 | 46 | 66 | 70 |

| Inventories Index (0.2) | 37 | 50 | 54 | 58 | 69 | 70 |

| Profit Margin Index (0.2 | 19 | 43 | 60 | 53 | 67 | 73 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief