Global| Dec 01 2017

Global| Dec 01 2017Manufacturing PMIs on an Upswing... in the West at Least

Summary

Manufacturing PMIs has been making strong gains on a rather widespread basis. But there is no denying that the epicenter of the rebound has been in the West. The United States and the EMU have shown particularly long-lived and strong [...]

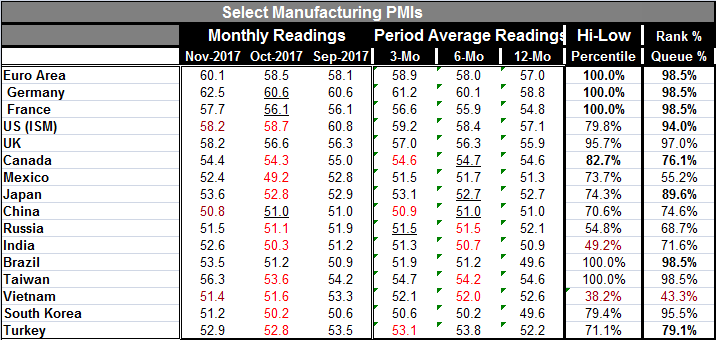

Manufacturing PMIs has been making strong gains on a rather widespread basis. But there is no denying that the epicenter of the rebound has been in the West. The United States and the EMU have shown particularly long-lived and strong ongoing manufacturing PMI gains. The chart is rather dramatic in its depiction of the EMU and the U.S. showing their respective manufacturing sectors advancing in leaps and bounds while China lies all but fallow on a manufacturing PMI reading that does not even reach 51.

Manufacturing PMIs has been making strong gains on a rather widespread basis. But there is no denying that the epicenter of the rebound has been in the West. The United States and the EMU have shown particularly long-lived and strong ongoing manufacturing PMI gains. The chart is rather dramatic in its depiction of the EMU and the U.S. showing their respective manufacturing sectors advancing in leaps and bounds while China lies all but fallow on a manufacturing PMI reading that does not even reach 51.

However, China's PMI, while lagging, has a standing that is not terrible. Ranked against its value since January 2012, the November manufacturing PMI lies above three quarters of China's observations over that period. The relatively low PMI value with a relatively firm percentile standing is an acknowledgement of the tough times China has had and recognition that digging out is in process but is still slow-going. By comparison, the EMU ranking finds the EMU PMI this high or higher about one half of one percent of the time as the November reading marks a new high point on this timeline for the EMU, Germany, France, Taiwan and Brazil. Taiwan and Brazil mark high points, like China, on relatively modest absolute readings as their PMIs have been struggling over the past six years.

India, Brazil, Taiwan, the euro area and Germany each posted monthly changes in their respective PMI levels that have been greater less than 10% of the time. This shows us that on the month there were some significant pick-ups in growth that were relative widespread globally.

The November rise in the manufacturing PMIs follows in the wake of a disappointing October. In October, of the 16 countries in the table, only Brazil, the U.K. and the euro area as a whole logged month-to-month improvement. Three PMIs were unchanged and full ten move to lower levels. But with the new postings in November, the trend to improving PMI values seems to be back on track and with some PMIs getting to quite elevated readings. As already noted, five of 16 countries/regions already are listing their highest readings since January 2012.

Markit, this month, reports robust conditions in the euro area with order backlogs piling up and pressures being demonstrated on input as well as output prices.

While there is a lot of optimism attendant to this report and in the wake of its clear improving trend, what is missing most is evidence that consumption has picked up anywhere. The PMIs speak to a ramp up in output; yet, we do not see evidence of retail sales rising strongly in the EMU or in the U.S. In the U.S. there has been moderation apart from the strong replacement buying of vehicles destroyed by hurricanes. Asia generally is not a hot-bed of consumerism and there is no evidence of sales conditions heating up there either.

This brings me around to my usual caveat on the PMI data. They are very sensitive data reports and they are formally about the breadth of output not about its strength. Growth has been pushing ahead in a fashion we call relentless but also ponderous. And we might expect that this sort of glacial advance would be more likely to be broad-based than one characterized by jack-rabbit like jumps by a few leading sectors. Both will tend to pull other industrial businesses along with them but the slow as it goes recovery would probably be the broader one. So we have great breadth of gains in manufacturing and we have yet to see growth that is knocking our socks off anywhere. There are improvements and advancements, but there are not many indications of output or consumer-led growth that is actually surging from reports that actually measure strength rather than breadth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief