Global| Jan 04 2010

Global| Jan 04 2010Manufacturing Is Digging Out

Summary

The PMI indices for MFG from Markit show an ongoing improvement across the e-zone. The e-Zone index is still some 8.9 points from its cycle peak but it has risen by 18 points from its cycle low. Greece at 10.6 points above its cycle [...]

The PMI indices for MFG from Markit show an ongoing improvement across the e-zone. The e-Zone index is still some 8.9 points from its cycle peak but it has risen by 18 points from its cycle low. Greece at 10.6 points above its cycle low has had the smallest recovery from its low point. The UK Germany and France have risen the most from their respective low points but the UK stands the closest to its cycle peak reading standing only 2.2 points below its cycle peak reading in December. Spain, Greece and France are still the farthest away from their respective cycle peaks.

In December among the countries in the table only Spain saw a set back. This is marked improvement from November when five of these countries experienced a set back in the month’s MFG PMI reading.

Spain’s index has fallen on balance over the last three months. It is the only one in this group to do so. However Austria and Greece rose by less than 0.5 points on balance over the last three months compared to an e-Zone index rise of 2.3points. .The e-Zone advance is now being led by improvements in Italy and in Germany but all the e-Zone countries in the table above are advancing at a slower rate than they had over six months (multiply the respective three month gains by a factor of two to see this). The UK, an EU member, is an exception to this trend as it is still accelerating.

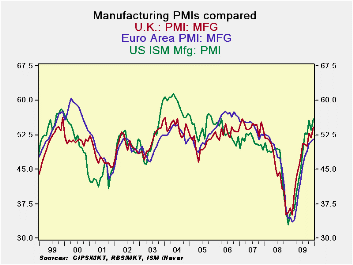

Spain, Greece and Ireland are the only countries in the table that are not back into pre-recession ranges for their MFG PMI readings (levels). The UK is the only country that is near the top of its pre-recession range in terms of its overall PMI index (March 2000- Jan 2008).

On balance the e-Zone is still making progress. Some choppiness in the indices in this region is to be expected if the recovery is going to continue but lose some of its gusto. If the recovery is going to gain speed we will need to see these indices continue to advance. The signals right now seem to favor a period of consolidation and of continued but slow growth progress.

| Changes in Markit MFG Indices | ||||||||

|---|---|---|---|---|---|---|---|---|

| Changes Mo/Mo | Change on Frequency | |||||||

| Dec-09 | Nov-09 | Oct-09 | 3Mo | 6Mo | 12Mo | From Peak | From Low | |

| Euro-13 | 0.39 | 0.47 | 1.44 | 2.30 | 8.97 | 17.72 | -8.9 | 18.0 |

| Germany | 0.25 | 1.40 | 1.39 | 3.04 | 11.81 | 20.03 | -8.2 | 20.7 |

| France | 0.31 | -1.21 | 2.62 | 1.72 | 8.85 | 19.80 | -10.1 | 19.9 |

| Italy | 0.71 | 0.85 | 1.66 | 3.22 | 8.11 | 15.26 | -9.2 | 16.2 |

| Spain | -0.09 | -1.02 | 0.48 | -0.63 | 2.43 | 16.70 | -12.3 | 16.7 |

| Austria | 0.88 | -1.12 | 0.74 | 0.50 | 8.80 | 15.80 | -8.0 | 17.7 |

| Greece | 1.54 | -0.72 | -0.49 | 0.33 | 1.12 | 7.83 | -10.6 | 10.6 |

| Ireland | 0.02 | 0.78 | 1.44 | 2.24 | 6.34 | 10.94 | -7.6 | 15.6 |

| EU | ||||||||

| UK | 2.33 | -1.16 | 2.94 | 4.11 | 6.87 | 18.53 | -2.2 | 19.1 |

| Percentile is over range since March 2000 | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief