Global| Oct 11 2006

Global| Oct 11 2006Lower Gasoline Prices Helped Lift Chain Store Sales

by:Tom Moeller

|in:Economy in Brief

Summary

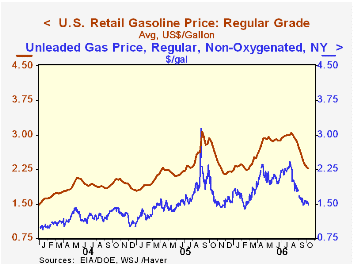

The retail price for a gallon of regular unleaded gasoline fell for the ninth consecutive week. The nickel decline last week lowered the price to an average $2.26 (-20.6% y/y) and was to the lowest level since February.

The retail price for a gallon of regular unleaded gasoline fell for the ninth consecutive week. The nickel decline last week lowered the price to an average $2.26 (-20.6% y/y) and was to the lowest level since February.

The retail price for a gallon of regular unleaded gasoline fell for the ninth consecutive week. The nickel decline last week lowered the price to an average $2.26 (-20.6% y/y) and was to the lowest level since February.

Moreover, the earlier decline in spot market prices resumed this week. In trading yesterday, the NY harbor price for regular unleaded gasoline fell to $1.48 per gallon versus an average $1.54 averaged during each of the prior two weeks.

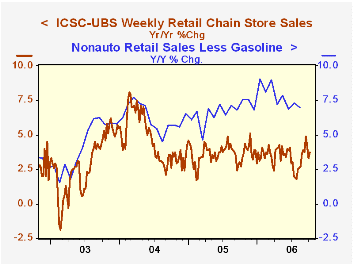

For the opening week of October, the International Council of Shopping Centers (ICSC)-UBS indicated that chain store sales rose 0.5% following four consecutive weeks of decline. The gain still left sales 0.5% below the average of sales in September which fell 0.5% from August. During the last ten years there has been a 47% correlation between the y/y change in chain store sales and the change in nonauto retail sales less gasoline.

During the last ten years there has been a 47% correlation between the y/y change in chain store sales and the change in nonauto retail sales less gasoline.

The ICSC-UBS retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

The leading indicator of chain store sales from ICSC-UBS rose again by 0.3%, the fourth gain in the last five weeks. The indicator in September rose 0.3% from the August average. Though slight (and downwardly revised), it was the first m/m rise since June.The latest Short-Term Energy Outlook from the U.S. Energy Information Administration is available here.

| ICSC-UBS (SA, 1977=100) | 10/07/06 | 09/30/06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 465.4 | 463.0 | 3.7% | 3.6% | 4.7% | 2.9% |

by Tom Moeller October 11, 2006

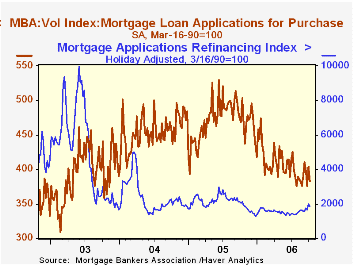

According to the Mortgage Bankers Association, the total number of mortgage applications last week retraced about half of the prior period's gain with a 5.5% decline. The decline nevertheless left applications up 1.7% from the September average.

Purchase applications reversed nearly all of the prior week's gain. The 5.3% w/w decline pulled the level of purchase apps in early October 3.1% below the September average which rose 3.2% from August.

During the last ten years there has been a 58% correlation between the y/y change in purchase applications and the change in new plus existing single family home sales.

Applications to refinance fell 5.8%. After the prior week's 17.5% surge, that left applications up 8.1% from the September average which rose 8.7% from August.

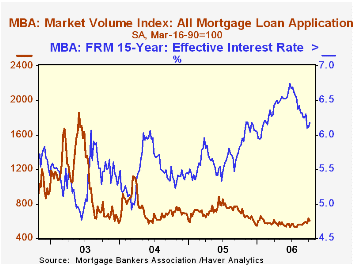

The effective interest rate on a conventional 30-year mortgage rose four basis points w/w to 6.49%. It averaged 6.50% last month versus 6.64% in August. The peak for 30 year financing was 7.08% late in June. The rate on 15-year financing also rose w/w to 6.18% versus 6.20% averaged last month. The peak rate was 6.75%. Interest rates on 15 and 30 year mortgages are closely correlated (>90%) with the rate on 10 year Treasury securities.

During the last ten years there has been a (negative) 79% correlation between the level of applications for purchase and the effective interest rate on a 30-year mortgage.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey accounts for more than 40% of all applications processed each week by mortgage lenders. Visit the Mortgage Bankers Association site here.

| MBA Mortgage Applications (3/16/90=100) | 10/06/06 | 09/29/06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total Market Index | 599.1 | 633.9 | -13.8% | 708.6 | 735.1 | 1,067.9 |

| Purchase | 383.3 | 404.6 | -18.4% | 470.9 | 454.5 | 395.1 |

| Refinancing | 1,857.0 | 1,970.8 | -7.4% | 2,092.3 | 2,366.8 | 4,981.8 |

by Carol Stone October 11, 2006

Basic industry data covering the winter months in South Africa seems to portray a fairly healthy economy. Retail sales volumes were up 1.0% in July and 11.5% from July 2005. Current price data show the biggest year-on-year increases in "general dealers", clothing and hardware stores; these were all up well more than 15%, but the history for individual store types extends back only through last year, so it's hard to judge the relative performances.

Basic industry data covering the winter months in South Africa seems to portray a fairly healthy economy. Retail sales volumes were up 1.0% in July and 11.5% from July 2005. Current price data show the biggest year-on-year increases in "general dealers", clothing and hardware stores; these were all up well more than 15%, but the history for individual store types extends back only through last year, so it's hard to judge the relative performances. Factory sales have also been buoyant, with monthly increases of 1.8% in August, 1.3% in July and 3.4% in June. These are in current prices and put sales up 15.1% from August 2005. Interestingly, though, factory output hasn't been this strong. It fell in July and August, by 0.4% and 0.7%, respectively, and is "only" 4.1% ahead of the year-ago month. Industries with strong sales include petroleum refining, metal products, electrical machinery and furniture. But at least the petroleum must relate to its high prices, since output of petroleum products was down 6.1% in August from the year earlier. Separately, production of wood and metal products and electrical machinery was up more strongly than the total, as was motor vehicles and parts.

Factory sales have also been buoyant, with monthly increases of 1.8% in August, 1.3% in July and 3.4% in June. These are in current prices and put sales up 15.1% from August 2005. Interestingly, though, factory output hasn't been this strong. It fell in July and August, by 0.4% and 0.7%, respectively, and is "only" 4.1% ahead of the year-ago month. Industries with strong sales include petroleum refining, metal products, electrical machinery and furniture. But at least the petroleum must relate to its high prices, since output of petroleum products was down 6.1% in August from the year earlier. Separately, production of wood and metal products and electrical machinery was up more strongly than the total, as was motor vehicles and parts. While many countries stand at various stages of development, South Africa's emphasis on machinery and metal products, as well as motor vehicles, gives us the impression that it is far along an industrial track. A quick comparison with GDPs of other countries shows that while, converted to US dollar terms, South Africa is about half the size of Turkey and moderately smaller than Poland, it is considerably larger than the Czech Republic and Hungary.

While many countries stand at various stages of development, South Africa's emphasis on machinery and metal products, as well as motor vehicles, gives us the impression that it is far along an industrial track. A quick comparison with GDPs of other countries shows that while, converted to US dollar terms, South Africa is about half the size of Turkey and moderately smaller than Poland, it is considerably larger than the Czech Republic and Hungary.

Data on South Africa are contained in Haver's EMERGEMA database. For many countries of the world, Haver has translated GDP into current and constant US dollars to facilitate international comparisons, such as we just made.

| South Africa, All Seas Adj. | Aug 2006 | July 2006 | June 2006 | Year Ago | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| Retail Trade, Volume, 2000=100 | -- | 140.5 | 139.1 | 126.0 | 128.7 | 119.7 | 115.1 |

| % Change | -- | 1.0 | -0.1 | 11.5 | 7.5 | 4.0 | 5.7 |

| Manufacturing Sales, Bil.Rand | 83.20 | 81.76 | 80.77 | 72.30 | 85.23 | 80.22 | 73.87 |

| % Change | 1.8 | 1.3 | 3.4 | 15.1 | 6.2 | 8.6 | -1.1 |

| Manufacturing Production, 2000=100 | 119.2 | 120.0 | 120.5 | 114.5 | 113.8 | 109.8 | 105.4 |

| % Change | -0.7 | -0.4 | 1.7 | 4.1 | 3.6 | 4.2 | -1.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief