Global| Apr 18 2018

Global| Apr 18 2018Japan’s Trade Surplus Returns Even As Trade Flows Slow

Summary

While the IMF has just lifted its outlook for growth in 2018, Japan is logging weaker and weaker export and import growth as the year progresses. Asia generally has been lagging. The PMIs in Europe have weakened but are still showing [...]

While the IMF has just lifted its outlook for growth in 2018, Japan is logging weaker and weaker export and import growth as the year progresses. Asia generally has been lagging. The PMIs in Europe have weakened but are still showing growth. The German ZEW financial experts have just cut their expectations for growth on a broad group of countries. And guess what? Everyone can’t disagree and still be right! I find the IMF’s decision to hike its forecast in the midst of concerns about a trade war and with various reports showing encroaching weakness an odd choice rather than a convincing argument.

While the IMF has just lifted its outlook for growth in 2018, Japan is logging weaker and weaker export and import growth as the year progresses. Asia generally has been lagging. The PMIs in Europe have weakened but are still showing growth. The German ZEW financial experts have just cut their expectations for growth on a broad group of countries. And guess what? Everyone can’t disagree and still be right! I find the IMF’s decision to hike its forecast in the midst of concerns about a trade war and with various reports showing encroaching weakness an odd choice rather than a convincing argument.

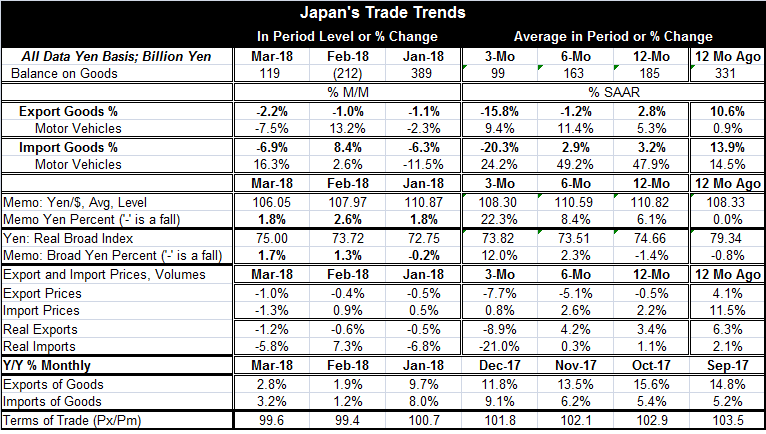

For Japan, the yen has been rising against the dollar and on a broad basis. That goes a long way toward explaining the weak exports - but not the weak imports.

The rising yen seems to be putting downward pressure on Japan’s export prices. Japan’s export prices have been exceptionally weak (in yen terms). Import prices have crept up increasingly slowly. In real terms, both Japanese exports and imports have fallen sharply especially over the last three months and particularly for imports. Such excessive import volume weakness in the face of a rising yen that should be boosting imports remains surprising.

Japan is an odd case to begin with. Its population is shrinking so its demand is fighting an uphill battle. Still, Japan’s GDP has been growing and that should be underpinning imports especially as the yen rises increasing Japan’s purchasing power. But there is a second possibility. Japan is quite sensitive to exchange rate developments and it is possible that the strength in the yen undermines confidence and leads to weakness and stunts imports despite their relative attractiveness.

However, more broadly there are global events that give substance to concerns about growth. I mentioned some of the economic trends at the outset of this article. But there is more than that. The geopolitical scene is particularly difficult especially for parties in Asia or in the Middle East. The U.S. position on trade has put most countries back on their heels. At the same time, the U.S. is pushing for some improvements in NAFTA and the recent surprise is the President making overtures to the possibility of joining up with the TPP after all - albeit with some modifications, of course. Just today the IMF issued a warning on the risk of excessive global debt with some not so subtle jabs at the U.S. and China. Make no mistake about it: these are debt warnings aimed at the largest and most important economies in the global matrix. This is not the IMF waving a red flag at someone unimportant off in the periphery.

There is not a lot of sure footing around these days. Asia has not really recovered. China’s growth is short of its mark and, as always, I am suspicious of what it might ‘really be doing.’ Even debt is less successful in motivating Chinese growth these days. Trade tensions are exacerbated by countries in the West being unwilling to trust the products of Chinese tech companies in telecommunications especially. While there is hope surrounding the upcoming North Korea talks, success is not guaranteed. The Middle East will continue to throw off displaced persons and Europe will continue to battle the problem of unwanted migrants and will create further divisions within Europe. What would happen in Asia if the push toward a new peace fails; if the talks collapse and sanctions remain in place or are tightened? On top of that, Japan’s Prime Minister Abe faces a deepening political problem that now seems likely to result in his leaving office prematurely. And Abe is not the only world leader on thin ice. Theresa May is under constant pressure; Angela Merkel is much less in control than she used to be; France is protesting Macron’s labor market reforms with nationwide strikes; and Italy is looking to form some sort of government. And in the U.S., Donald Trump is Donald Trump. It is not possible to name a major economic/political power whose leader is not facing political challenges at the moment apart from in China, Russia, and North Korea. And that is a chilling admission on where we stand.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief