Global| Apr 23 2019

Global| Apr 23 2019Japan’s CPI and Core CPI Creep Higher

Summary

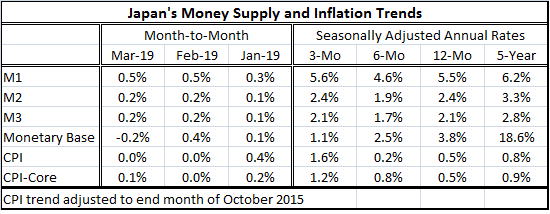

Japan's money supply is showing no change in its rate of growth across its various measures. The respective 12-month and three-month growth rates are nearly identical for M1, M2 and M3 although each aggregate weakens slightly over six [...]

Japan's money supply is showing no change in its rate of growth across its various measures. The respective 12-month and three-month growth rates are nearly identical for M1, M2 and M3 although each aggregate weakens slightly over six months. Monetary base, however, shows decelerating growth.

Japan's money supply is showing no change in its rate of growth across its various measures. The respective 12-month and three-month growth rates are nearly identical for M1, M2 and M3 although each aggregate weakens slightly over six months. Monetary base, however, shows decelerating growth.

CPI headline inflation gains just 0.5% over 12 months, weakens its pace over six months, then accelerates over three months. Oil prices are just starting to make a recovery after a period of weakness and that gain in price will filter through to the CPI headline. But the core CPI, free from the impact of rogue commodity prices, also is on the rise. The core pace has picked from 0.5% over 12 months to 0.8% over six months and to 1.2% over three months.

Japan's indicators do not paint a picture of an economy rising up to grow strong and to pressure inflation higher. This has been a dream or nightmare at central banks around the world. The dream is that growth will gain footing and will become more solid, stronger and dependable. And that with it prices will firm, inflation will rise and the threat of deflation will dissipate. The nightmare is that inflation will not just rise but may also surge and after being bottled up so long and it will take a strong dose of monetary medicine to control it. In the event, neither one of these scenarios has come to pass.

In the U.S., growth did firm and accelerate on the back of fiscal stimulus, but inflation still did not rise. In Europe, the central bank stayed in the full stimulus mode for a very long time. At the end of 2018 as the ECB was preparing for the delivery of less stimulus, the German economy slowed. The ECB is now on the fence about what comes next. It has more lending stimulus planned, but beyond that it is playing its cards one at a time.

In Japan, the Bank of Japan has its full stimulus policy in gear including yield curve control. GDP continues to grow but not to impress. Of course, Japan's situation is unique with its shrinking population. That makes it hard for Japan to post strong-looking growth. But even the relative lack of labor resources has not been enough to light any inflation fires in Japan. Japan trades most intensively with China and second most with the U.S. Its trade with China, a very low wage and highly competitive country, helps to keep the lid on prices in Japan. And the aged population simply makes Japan a hard place to get price pressure started so inflation in Japan continues to undershoot. Too many Japanese consumers are in the saving portion of their life cycle.

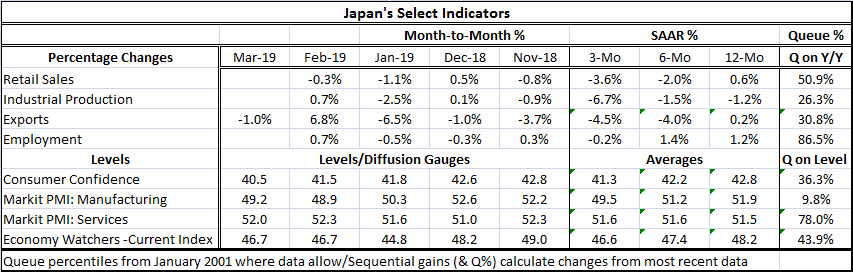

Currently, the Japanese economy is struggling on a number of fronts. Retail sales fell in February and in January and are falling at a 3.6% annual rate over the last three months. And retail sales have been steadily losing momentum over the past year, along with industrial production, and exports. Employment growth is moderate but has been slipping; over the last three months it is declining.

The queue percentile standings for industrial production and exports are particularly weak in their lower 30th percentiles or weaker. Retail sales growth is about at its median pace with a 50.9 percentile standing for its 12-month rate of growth. Employment growth even with its decline over three months has a 12-month growth rate that ranks it in the 86th percentile. Of course, with weak population growth, weak-looking employment growth is still pretty solid for Japan.

Consumer confidence has a 36th percentile standing. That tells us that consumers are at least somewhat restless. The Markit manufacturing PMI ranked over the last four years has a 9.8 percentile standing – extremely low. The economy watchers index has a 43rd percentile standing, below its historic median. However, the backbone of Japan's strength is its services sector where the Markit services PMI has a 78th percentile standing.

On balance, Japan is challenged to maintain growth because of its shrinking population. This is a structural and long lasting issue for Japan. Currently, momentum is slipping. Growth is holding to positive ground mostly by the services sector. But Japan in Asia does business in the large shadow of China, a country deep in debt where growth has been slowing and the authorities have been fighting to prop it up. The global manufacturing slowdown is weighing heavily on Japan. Surprisingly, with these conditions, there is some firmness to inflation, and to core inflation at that, but that gain does not seem to have any staying power.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief