Global| Jan 21 2015

Global| Jan 21 2015Japanese Sector Performance Leaves Little Room for Optimism

Summary

Japan's sector indices were less weak than expected. Japan's LEI was revised higher, mitigating the adverse signal from its monthly drop. But on balance there is little good news here apart from the bad news not being worse. The [...]

Japan's sector indices were less weak than expected. Japan's LEI was revised higher, mitigating the adverse signal from its monthly drop. But on balance there is little good news here apart from the bad news not being worse.

Japan's sector indices were less weak than expected. Japan's LEI was revised higher, mitigating the adverse signal from its monthly drop. But on balance there is little good news here apart from the bad news not being worse.

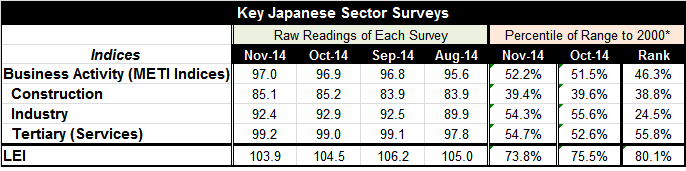

The overall business activity index for Japan edged higher to 97.0 in November from 96.9 in October. That's not much to cheer about. The index sits in the 46th percentile of its historic queue behind its median, which lies at 50.

The industry gauge is particularly weak; it fell month-to-month to 92.4 from 92.9. The gauge stands in the 24th percentile of its historic queue, at the edge of the bottom quartile of its historic queue of values. This sector displays no momentum and has extreme weakness.

Construction edged lower month-to-month, drifting to 85.1 from 85.2. The index sits in the 38th percentile of its historic queue of values. The sector is weak and losing momentum.

The tertiary sector, or services sector, is the lone sector rising in November. But it is not exactly a locomotive, rising only to 99.2 from 99.0. The tertiary sector sits in the 55th percentile of it historic queue, above its midpoint by a modest margin.

Japan is not showing much momentum. The Bank of Japan policy of stimulus remains in force full throttle, but there is no evidence of a cumulating stimulus after a good start.

The new kid on the block is the European Central Bank; it's planning to do QE for the first time, quite a bit late in the cycle. With European bond yields already below zero across many markets in the euro area, it is not clear how well the ECB policy can work and if there is any stimulus there for the rest of the world.

Global growth remains weak. The IMF trimmed its outlook earlier in the week. China has just initiated a program of liquidity injections to stimulate its market. Fiscal policy is held in abeyance everywhere although in the U.S., in his State of the Union address, President Obama suggested a public works program to repair infrastructure while promising to block the Keystone pipeline. Global policy continues to rest on the assumption that monetary policy, a crutch already leaned on too hard, can work even as central banks dip into the less successful forms of monetary policy like QE.

While the weakening yen could help Japan, the fact that so much industry has been outsourced reduces the favorable impact on Japan of the lower yen. Global growth continues to depend on luck, esoteric policy initiatives and the kindness of strangers overseas. No one is really stepping up to the plate. It remains an age of austerity.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief