Global| Mar 19 2008

Global| Mar 19 2008Japan Slips and its Assessment is Cut…

Summary

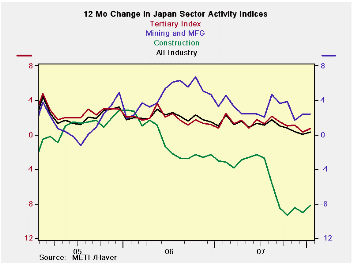

Japan’s all-industry index was flat in January. The tertiary index that it tracks so closely was up to 110.3 from 109.5 in December. In terms of year-to-year changes the tertiary and all-industries indices are about the same showing a [...]

Japan’s all-industry index was flat in January. The tertiary index that it tracks so closely was up to 110.3 from 109.5 in December. In terms of year-to-year changes the tertiary and all-industries indices are about the same showing a small bounce in the recent month but holding in a shallow downtrend overall. Mining and MFG are well off peak and the sector moved lower in January to 109.5 from 112.0 in December. This left the year/year change in the index near zero. Over the past several months Japan’s sector indices have more or less held steady in terms of their year/year changes. Even the very weak construction index that fell again in January is steady to a bit higher over 12 months.

Amid these signals the Japanese government has downgraded its assessment of the economy for the second consecutive month in March.The Cabinet Office that issues the assessment cited stalled corporate capital spending and weak industrial production. Private consumption has lagged for time and was also on the laundry list of reason to downgrade the economy. The government said in its March report that "the economic recovery appears to be pausing recently." This pronouncement is a bold contrast to its overview in the February report that held: "the economy is recovering at a moderate pace recently." Things change.

This is the ‘first second’ for a downgrade: It is the first

time in this cycle that the government has downgraded its overall

assessment of the economy for the second month in a row. Last time it

did such a thing was in November and December 2004.

The first downgrade in this cycle came in February a

period that is not yet covered in the data table below.

In February the government lowered its assessment of the

economy due to slower growth of exports and industrial production in

addition to continuing weakness in private consumption and housing

construction. This month’s downgrade features some of the same sectors:

capital investment, industrial output and private consumer spending.

Japan once again has issues. With the yen now rising, Japan faces

challenges and still needs a head at its central bank. …and it’s not a

good time to be without monetary leadership.

| Up to date Japan Industry Surveys | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Recent Months | Moving Averages | Extremes; Range | |||||||

| Jan 2008 |

Dec 2007 |

Nov 2007 |

3Mo | 6Mo | 12Mo | Max | Min | %-Tile | |

| All Industry | 107.0 | 107.0 | 107.4 | 107.1 | 107.4 | 107.3 | 108.4 | 93.6 | 90.5% |

| Construction | 71.5 | 72.0 | 72.1 | 71.9 | 72.3 | 76.3 | 124.6 | 71.1 | 0.7% |

| Mining and MFG | 109.5 | 112.0 | 110.4 | 110.6 | 111.1 | 109.4 | 112.2 | 87.7 | 89.0% |

| Tertiary | 110.3 | 109.5 | 110.5 | 110.1 | 110.2 | 110.1 | 111.2 | 91.0 | 95.5% |

| Ranges, Max, Min since 1993 | |||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief