Global| Apr 25 2018

Global| Apr 25 2018Japan Shows Very Moderate Growth As Trade War Clouds Gather

Summary

Japan’s sector indexes showed a solid gain in February, but it’s less than expected and it brings the business activity index to a level that is barely above its level of last October. The METI indexes are at relatively high marks as [...]

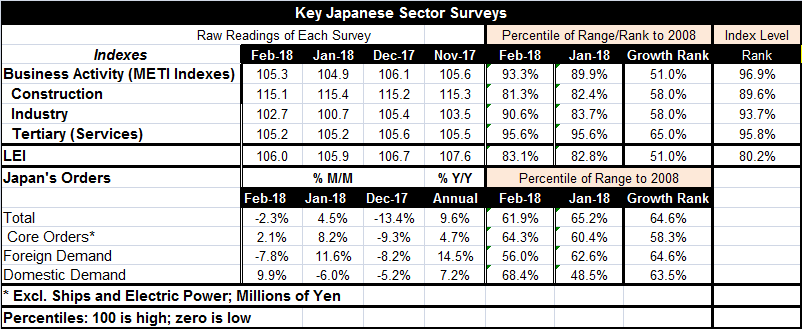

Japan’s sector indexes showed a solid gain in February, but it’s less than expected and it brings the business activity index to a level that is barely above its level of last October. The METI indexes are at relatively high marks as index levels, but these index levels are supposed to grow over time. So being at less than a 100% reading on the level is actually not a very strong showing. The growth rank which places the year-over-year growth rate in its ordered percentile of results since 2008 has the headline index only at its 51st queue percentile, barely above its median for the period (the median occurs at a queue ranking of 50). The construction and the industry indexes stand at their respective 58th percentile, position at modest readings. The services sector (tertiary index) has a 65th percentile standing, also relatively moderate.

Japan’s sector indexes showed a solid gain in February, but it’s less than expected and it brings the business activity index to a level that is barely above its level of last October. The METI indexes are at relatively high marks as index levels, but these index levels are supposed to grow over time. So being at less than a 100% reading on the level is actually not a very strong showing. The growth rank which places the year-over-year growth rate in its ordered percentile of results since 2008 has the headline index only at its 51st queue percentile, barely above its median for the period (the median occurs at a queue ranking of 50). The construction and the industry indexes stand at their respective 58th percentile, position at modest readings. The services sector (tertiary index) has a 65th percentile standing, also relatively moderate.

The fact that the total business index has a percentile standing below that of any of the components tells us that the confluence of weakness is unusual. Since the business activity index is a weighted average of its components, the clear message is that this coordination of moderate readings is historically unusual leaving the weighed activity index on a rank basis weaker than any of its components and barely above its median showing.

The ranking for Japan’s orders data echo the moderation we see in the METI indexes. Orders standing in their high 50 percentile range to mid-60s percentile range are again a series of moderate readings.

Japan is not showing any acceleration. Growth is hanging on but not looking like it is spreading. The inflation picture does appear to have stabilized either in Japan and certainly inflation is not yet at the BOJ target. Yet, all of this is happening with a great deal of help from the Bank of Japan’s massive money stimulus effort. At the same time, Europe is showing signs of lost momentum despite ongoing strong readings on consumer confidence there. Domestic activity surveys as well as the Markit and EU indexes show a loss of momentum that may or may not be linked to concerns about trade wars and tariffs. While Germany trades a great deal (exports are 48% of GDP), much of German trade is conducted within the umbrella of Europe and inside the euro area itself under the regime of a fixed exchange rate and cocooned in the web of agreements that form its customs union. Much of German trade is completely insulated from potential tariffs or trade wars. In Japan, there is more vulnerability to U.S. trade actions. But Japan trades more with China than with the U.S. these days. Moreover, it has been looking more and more like the broad tariffs were meant as a threat rather than as a policy option that was planned to be implemented.

Tariff denial

Every U.S. trade partner from Canada to Mexico to Europe to Asia has tried to assert a special relationship to get out from under the crush of the U.S. tariff threat. And this surprisingly includes countries that have arranged their affairs to run nothing but trade surpluses with the U.S. over the years as though that is OK so that tariffs should not be aimed at them, when in fact tariffs very much SHOULD be aimed at them.

The purpose of trade war threats

There is little doubt that U.S. President Donald Trump is prepared to use tariffs if he cannot get some of the trade deals that he wants. He is a disrupter. He was elected to disrupt. He is doing more or less what had been expected of him, recognizing, of course, that when you recruit someone be disruptive you will not control them or the means or targets of their disruption. But Trump has been remarkably true to his election pledges to disrupt. And he has a very good point about how America has been treated unfairly. U.S. trade deficits are bad. They do not finance productive investment in the U.S. They mostly facilitate financial investment by foreign countries placing funds in the U.S. to maintain their own exchange rate competitiveness. U.S. GDP is 70% consumption. We are financing our own consumptive largesse, using deficits, piling up debt, that future generations will get stuck with as we today ‘live beyond our means.’ Yes, as difficult as things are, they would be even worse in some ways without the deficits. Imagine if we had to save enough (consumer much less) to finance domestically our own fiscal deficits? Our capital inflows make government debt easier to bear; they encourage the government to run larger fiscal deficits too. Academics make the academic point that deficits are neither good nor bad ‘per se.’ And while that is correct (as an abstract point), the U.S. deficits as a specific case in point are definitely bad. Since they are structural, they have helped us to live beyond our means consistently since the early 1980s. And make no mistake about it…someone WILL pay for this. Maybe it will be YOUR children.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief