Global| Jun 19 2013

Global| Jun 19 2013Japan's Trade Trends

Summary

Japan's yen-based current account deficit eroded again in May as exports rose by 3.2% as imports rose faster by 4.7%. Over three months Japanese exports and imports are both growing at a hefty pace over 30% with imports growing [...]

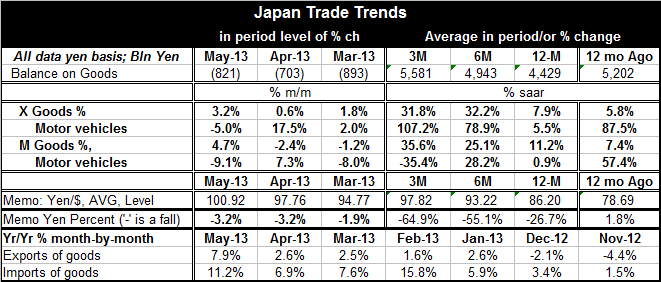

Japan's yen-based current account deficit eroded again in May as exports rose by 3.2% as imports rose faster by 4.7%. Over three months Japanese exports and imports are both growing at a hefty pace over 30% with imports growing slightly faster. These growth rates are also strong over six months. For that period, export growth is nearly flat while imports have accelerated from the 25% pace to their 35% pace over three months. Year-over-year Japanese exports are up by nearly 8% with imports up by about 11%.

Japan's yen-based current account deficit eroded again in May as exports rose by 3.2% as imports rose faster by 4.7%. Over three months Japanese exports and imports are both growing at a hefty pace over 30% with imports growing slightly faster. These growth rates are also strong over six months. For that period, export growth is nearly flat while imports have accelerated from the 25% pace to their 35% pace over three months. Year-over-year Japanese exports are up by nearly 8% with imports up by about 11%.

One year ago the yen was sitting at a level of 86.2 yen Vs the US dollar. It has since fallen to a level of 100.92 yen. This drop is been one of the main factors driving Japanese exports. The program of QE has been successful in getting the yen lower, helping to stimulate Japanese exports, reviving the domestic economy and helping to increase imports. Despite the rapid decline of the yen, and the recent backtracking in its move, more weakness lies ahead for it. The yen had been vastly overvalued and the QE process is beginning to undo that situation, to restore normalcy to the exchange market.

Still, the Japanese economy is a long way from getting the all-clear signal. Japan has huge debt problems and ongoing issues with the demographic trends that imply a shrinking population. That will make growth harder to attain and will intensify the already heavy burden of the federal debt. Financing its current needs is also an issue for Japan, The older population should begin to whittle down its pile of assets instead of continue to build them.

Japan's ongoing shift away from nuclear power has boosted its imports of fuels and undermines what has been a long history of current account surpluses for Japan. Fortunately Japan's heavy indebtedness is not an issue for international investors as it owes most of its debt to its own citizens. So the crop up of a string of current account deficits is not a problem for Japan's financing.Japan continues to have problems not just in developing economic demand, but with the ongoing issues from its 'ongoing' nuclear disaster. Just recently the toxic radioactive isotope strontium-90 has been found in the groundwater at Japan's Fukushima nuclear plant. The presence of this toxic radioactive isotope in the local groundwater is a disturbing new development.

Japan's export and import revival is encouraging. Still, exports have not been able to move ahead of imports to reduce Japan's monthly trade deficit. But the revival in the growth rates for both exports and imports are good signs for an improvement in the demand for Japan's products, underscoring the repair that's been made to Japan's competitiveness. Strength in imports underscores the revival of the domestic economy. Year-over-year figures are only just beginning to come into line. The biggest growth rates have been those of the recent handful or so of months, but it's still a set of encouraging developments for a country that still has a long way to go to solidify its outlook for sustainable economic growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief