Global| Jun 19 2017

Global| Jun 19 2017Japan's Trade Surplus Levels Off

Summary

Japan's trade surplus continues to putter along in a show draft instead of rising as had been expected in May. Japan's exports were flat while imports advanced by 0.3%. Exports show a steady trend of deceleration with growth of 12.2% [...]

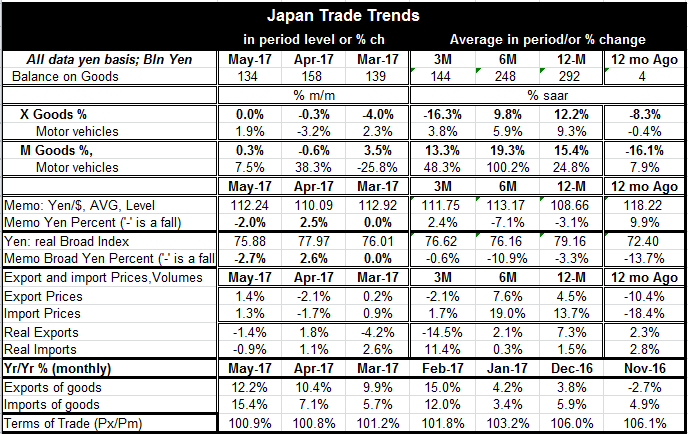

Japan's trade surplus continues to putter along in a show draft instead of rising as had been expected in May. Japan's exports were flat while imports advanced by 0.3%. Exports show a steady trend of deceleration with growth of 12.2% over 12 months shrinking to 9.8% over 6-Mo and further to -16.3% over three months. Japan's import growth has been steadier with growth of 15.4% over 12-months, 19.3% over 6-Mo and 13.3% over 3-Mo. Japan's import growth is weaker over 3-Mo than over either 6-Mo or 12-Mo but the step down is small compared to exports. Still it is not clear that these metrics mark enduring trends especially for imports where oil and oil prices form a greater part of the volatility.

Japan's trade surplus continues to putter along in a show draft instead of rising as had been expected in May. Japan's exports were flat while imports advanced by 0.3%. Exports show a steady trend of deceleration with growth of 12.2% over 12 months shrinking to 9.8% over 6-Mo and further to -16.3% over three months. Japan's import growth has been steadier with growth of 15.4% over 12-months, 19.3% over 6-Mo and 13.3% over 3-Mo. Japan's import growth is weaker over 3-Mo than over either 6-Mo or 12-Mo but the step down is small compared to exports. Still it is not clear that these metrics mark enduring trends especially for imports where oil and oil prices form a greater part of the volatility.

In volume terms exports are falling while imports mostly tend to show stronger growth. Real exports are up by 7.3% over 12-months up by 2.1% at an annual rate over six months but are falling at a 14.5% annual rate over three months. Import gains are steadier, with imports up by a narrow 1.5% over 12-Mo and a skinny 0.3% pace over six months then accelerating to a an 11.4% pace of increase over 3-Mo.

While we often think of exchange rate effects when we speak of Japan's trade, the exchange rate impact has been muted over the past year. Over the 12-mo the yen is 3.1% weaker Vs the dollar and 3.3% weaker on an inflation-adjusted broad basis. On both of these metrics the yen is weaker on a six month basis and on both it is less weak or stronger over three-months. Exchange rate effects have not been kicking trade flows around that much over the past year. Instead, economic growth and growth differences and oil prices have been the dominant feature in trade performance.

Exchange rates also greatly affect export and import prices. On the price front economists look at a gauge called the terms of trade. The "terms of trade" refers to the ratio of export to import prices. The "terms of trade" ratio is a quick way to assess the changing welfare effect on an economy of trade. If the terms of trade are improving (the ratio is rising) a country is gaining in its purchasing power since export prices would be rising faster than import prices. Japan's terms of trade have slipped from an export price to import price ratio of 109.7% one year ago to 100.9% in May of 2017. This slippage is common over this period for most non OPEC countries since oil prices have been rising (sharply!) and as a key importable good, oil will raise import prices. So Japan like most developed economies has been paying more for oil and getting (in relative terms) less for its exports and that reduces its standard of living to some extent.

Japan's trade: An Overview

Viewed as a whole we find Japan is not generating the surplus in May that was expected. We find its surpluses on its trade account are cruising sideways without trend for the last three-months. Japan's import growth points to weakness but to improving domestic demand as import growth has increased from its very slow real gain over 12-months. But on the export front Japan is not scoring wins and export volumes and values are slowing and contracting. Japan's year over year exports continue to look healthy while its recent results show a marked step down. This divergence will bear watching.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief