Global| Nov 20 2017

Global| Nov 20 2017Japan's Trade Surplus Flattens Out

Summary

Japan's trade trends, seemingly, offer little to the story about Japan's growth or global growth. Its surpluses have flattened out in the 300 billion yen range. Its exports and imports are now growing at very flat and highly similar [...]

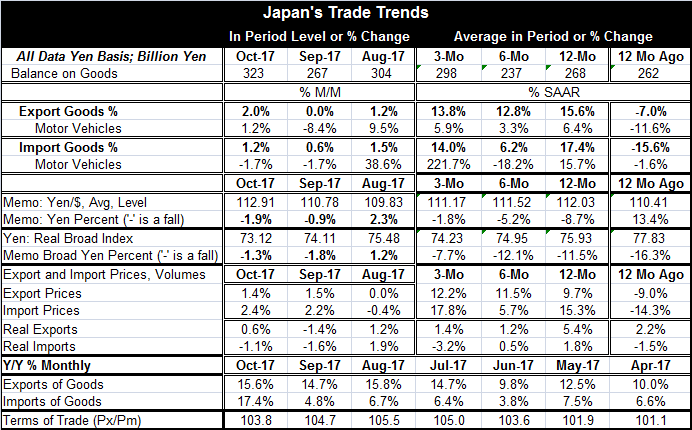

Japan's trade trends, seemingly, offer little to the story about Japan's growth or global growth. Its surpluses have flattened out in the 300 billion yen range. Its exports and imports are now growing at very flat and highly similar trajectories. However, under this surface of nominal stasis, there are still some conflicting forces at work.

Japan's trade trends, seemingly, offer little to the story about Japan's growth or global growth. Its surpluses have flattened out in the 300 billion yen range. Its exports and imports are now growing at very flat and highly similar trajectories. However, under this surface of nominal stasis, there are still some conflicting forces at work.

In nominal terms, the numbers we most readily see, exports expand at a 13.8% pace over three months compared to imports at a 14.0% pace. Exports are up at a 15.6% pace over 12 months and imports are rising by 17.4% over 12 months. The nominal growth rate seems to be joined at the hip; however, in truth, that result is coincidence and the factors behind these nominal growth rates are more much more complex, diverse and actually are out of sync with each other despite their appearance of conformity.

Let's begin by comparing prices. Export prices are up at a 12.2% pace over three months and by 9.7% over 12 months. Import prices are up at a 17.8% pace over three months and by 15.3% over 12 months. The export and import prices paths are more diverse than the nominal growth rates. A good deal of this difference is because of the rising price of oil, an important Japanese import.

Next look at real trade flows. Real exports are up at a meager 1.4% pace over three months and by 5.4% over 12 months. Real imports are falling over three months, declining at a 3.2% annual rate while gaining just 1.8% over 12 months.

In the break out of the nominal growth rates into real and price portions, we can see that on the import side prices have risen much more and there is some import conservation going on as import price elasticities begin to work. Higher prices cause consumers to stay away from the higher priced good or to use less of it. On the export side, prices have risen but not by as much so that real export flows have slowed but are not falling.

The yen has been declining more or less steadily over the past year, dropping at an 8.7% pace over 12 months in nominal terms vs. the dollar and dropping on a real and broad-based trade-weighted fashion by a faster 11.5% drop. A rising yen gives Japanese exporters an opportunity to raise prices to some extent and still to increase competitiveness (in foreign currency terms). That explains in part why exports are not falling. Still, even with the weaker yen, the pace of exports is very slow and so there is little presumption that Japan is facing any kind of substantial growth in its export markets. Japan's rising import prices are a function of rising oil prices (Brent oil is up at an 80% annual rate over three months!) and of rising import prices on other goods from other regions because of the yen's fall. The weaker yen helps to raise yen-based import prices (as we see it is doing with some help from oil) and that in turn reduces import volume, which is happening as imports are falling over three months. Still, this extreme weakness for imports also suggests that domestic demand in Japan is not very strong. Indeed, Japan's Q3 growth rate (annualized) was only 1.4% with GDP up by 1.6% year-on-year.

Japan's two largest trading partners are the U.S. and China. And while China is running a growth rate in the 6.5% to 7% range, it has been slowing down. The U.S. has speeded up with growth pressing the 3% mark. U.S. consumption has been subdued except for a spurt of auto buying to replace vehicles lost in a recent one-two punch from hurricanes. On balance, Japan's trade slows do not seem to signal a great deal about foreign demand picking up.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief