Global| Jun 19 2019

Global| Jun 19 2019Japan's Trade Deficit Worsens As Exports Decelerate Faster

Summary

Japan's trade deficit surged in May. The moving average of the deficit has worsened from 12-months to 6-months to 3-months. Exports are falling and are falling more rapidly from 12-months to 6-months to 3-months. Imports have been [...]

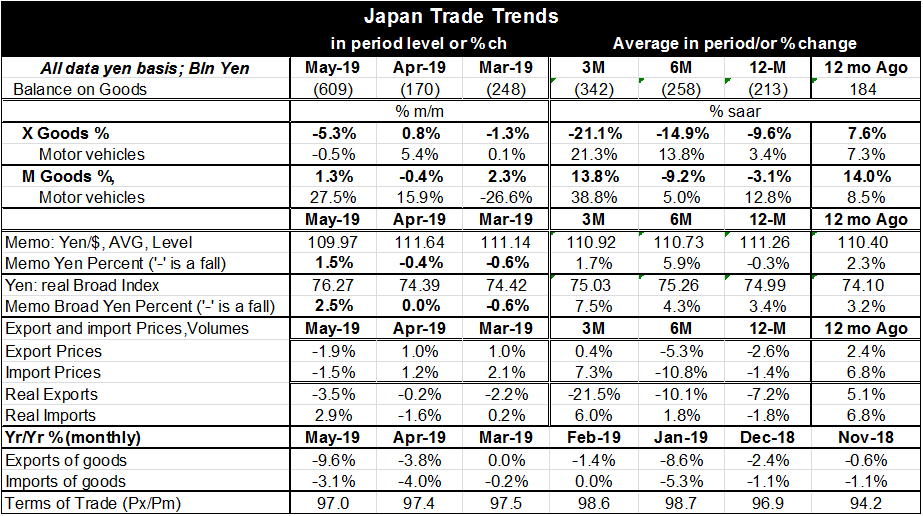

Japan's trade deficit surged in May. The moving average of the deficit has worsened from 12-months to 6-months to 3-months. Exports are falling and are falling more rapidly from 12-months to 6-months to 3-months. Imports have been weak until the last 3-months. Over 12-months and 6-months imports are falling but over 3-months they are rising sharply.

Japan's trade deficit surged in May. The moving average of the deficit has worsened from 12-months to 6-months to 3-months. Exports are falling and are falling more rapidly from 12-months to 6-months to 3-months. Imports have been weak until the last 3-months. Over 12-months and 6-months imports are falling but over 3-months they are rising sharply.

The yen exchange rate Vs the dollar has been relatively stable but has been strengthening in recent months. The broad real trade weighted yen also has been rising slowly.

Export prices and import prices that fall over 12-months and 6-months are now rising over three-months. Import prices are rising sharply. Typically a strengthening currency will depress own-currency export prices and import prices.

We can use export and import prices to deflate nominal flows to create export and import volumes. Export volume shows that exports are plunging on a real basis, falling at a 21.5% annual rate over three-months. Real imports are growing faster over shorter horizons despite some recent yen strength. That is helping to balloon Japan's trade deficit and to weaken growth.

Clearly Japan's exports have been hit by trade tensions and events. Japan trades most intensely with the US and China the two countries that are engaged in a trade war. A trade war can create all sorts of trade distortion and deflection so we are in an anything goes zone now with Japan trading heavily with these two heavy-weight trade combatants.

In the recent Zew survey German financial experts that report in that survey see more monetary easing in Japan and more deflationary pressure there on both prices and on growth.

In Europe, Mario Draghi has pledged to do more easing if European inflation does not come back to its target. But in Japan the government has not cut its outlook for the economy. The BOJ stands ready to do more if necessary. The Fed is meeting and is broadly expected to engage in some easing this year …but not yet. Whether central bankers take another step or not may not matter. Monetary policy has not been an effective stimulant to growth just about anywhere. But Japan is full up on fiscal policy and is planning a long-awaited consumption tax hike. Monetary policy may be Japan's last chance unless it decides to go whole hog for modern monetary theory.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief