Global| Oct 01 2015

Global| Oct 01 2015Japan's Tankan Survey Tails But Holds High

Summary

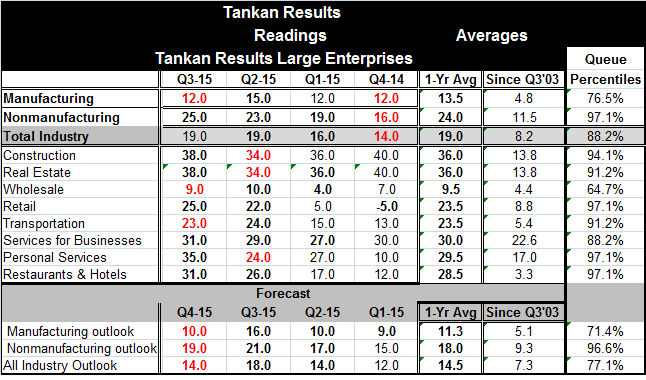

Japan's Tankan survey of large, medium-sized and small firms showed a drop in its bellwether large company index of manufacturers. That index fell to 12 in Q3 2015 from 15 in Q2. The index value of 12 is below the four-quarter average [...]

Japan's Tankan survey of large, medium-sized and small firms showed a drop in its bellwether large company index of manufacturers. That index fell to 12 in Q3 2015 from 15 in Q2. The index value of 12 is below the four-quarter average value of 13.5. That index sits in the 76.5 percentile of its historic queue of values. That is a moderately firm standing. Nonmanufacturing saw an improvement in its index to 25 in Q3 from 23 in Q2. It stands above its 12-month average of 24 and stands much higher in its historic queue, in its 97.1 percentile. This sector is rarely stronger and still improving.

Japan's Tankan survey of large, medium-sized and small firms showed a drop in its bellwether large company index of manufacturers. That index fell to 12 in Q3 2015 from 15 in Q2. The index value of 12 is below the four-quarter average value of 13.5. That index sits in the 76.5 percentile of its historic queue of values. That is a moderately firm standing. Nonmanufacturing saw an improvement in its index to 25 in Q3 from 23 in Q2. It stands above its 12-month average of 24 and stands much higher in its historic queue, in its 97.1 percentile. This sector is rarely stronger and still improving.

The total industry index is a combination of these two sectors. It is unchanged in Q3 at a level of 19. The total industry index stands at its 12-month average and in the 88th percentile of its historic queue of data.

The eight nonmanufacturing sectors show steady exceptional strength. Of those eight, six sectors have standings in their 90th percentile range. One has an 88th percentile standing. Only wholesaling has weaker, but still moderate, 64th percentile standing.

Japan is an economy driven by its manufacturing sector; that is why despite exceptionally strong performance outside manufacturing, there is some concern about this month's reading. The focus of the tankan index is the manufacturing gauge.

There are also outlooks formed for the quarter ahead for the tankan sectors. The outlooks for the manufacturing index and the nonmanufacturing index in Q4 both showed declines compared to the expectations formed for Q3. The manufacturing outlook index fell sharply from a 16 outlook index last quarter to 10 for Q4. That slippage leaves it below its 12-month average of 11.3 and in the 71st percentile of its historic queue of outlook values. The nonmanufacturing outlook slipped to 19 for Q4 from an outlook value of 21 for Q3. The Q4 outlook slipped sharply but to a still very strong 96.6 percentile standing for its Q4 outlook.

While Japan's current quarter and outlook values have fallen off, they are not weak. The manufacturing sector has an average historic outlook value of 5.1, a value it nearly doubles this quarter. Similarly, the nonmanufacturing sector outlook more than doubles its historic average, despite its backtracking.

Japan is hoping to hop-up the growth rate to something much stronger. And last quarter's manufacturing outlook and current manufacturing Tankan index made it look like that was in train. Now the readings for Q3 and the outlook for Q4 are less robust, but still very constructive readings. The disappointment over the Tankan is more about having had very hopeful expectations that were not met. But as can be seen in the nonmanufacturing sector there is real strength outside of manufacturing and manufacturing itself is still making solid progress.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief