Global| Dec 14 2015

Global| Dec 14 2015Japan's Tankan Is Unchanged But the Outlook Is Cut

Summary

Japan's large manufacturing firms, the bellwether group in the tankan report, showed an unchanged reading of 12 in Q4 2015. Nonmanufacturing firms showed an unchanged reading as well, but the overall total industry index ticked lower [...]

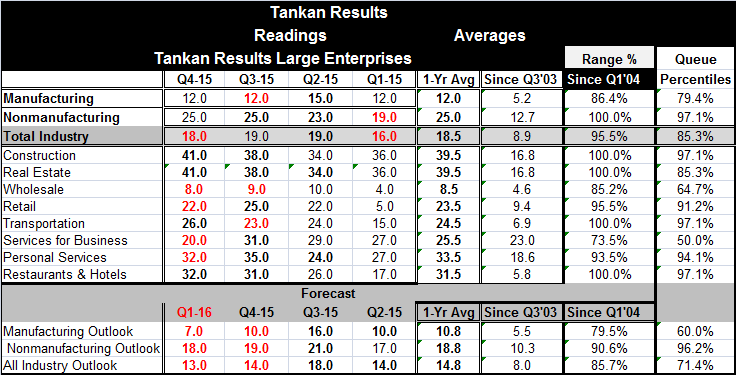

Japan's large manufacturing firms, the bellwether group in the tankan report, showed an unchanged reading of 12 in Q4 2015. Nonmanufacturing firms showed an unchanged reading as well, but the overall total industry index ticked lower to a reading of 18 in Q4 from 19 in Q3. The manufacturing tankan reading has a 79th percentile standing which is quite firm. Nonmanufacturing firms are much stronger in relative terms with a queue standing of 97.1% (the reading has only been this strong or stronger about 3% of the time). The total industrial standing is in its 85th percentile.

Japan's large manufacturing firms, the bellwether group in the tankan report, showed an unchanged reading of 12 in Q4 2015. Nonmanufacturing firms showed an unchanged reading as well, but the overall total industry index ticked lower to a reading of 18 in Q4 from 19 in Q3. The manufacturing tankan reading has a 79th percentile standing which is quite firm. Nonmanufacturing firms are much stronger in relative terms with a queue standing of 97.1% (the reading has only been this strong or stronger about 3% of the time). The total industrial standing is in its 85th percentile.

Nonmanufacturing details shows strength in construction, transportation, restaurants and hotels and in personal services and retailing. Real estate is also relatively strong. Wholesaling and services for business have more moderate percentile standings. The business-related sectors are doing relatively worse and manufacturing is lagging.

Moving to the outlook for Q1 2016, manufacturing has an outlook that has slipped to 7 from 10. The manufacturing outlook stands in the 60th percentile of its historic queue of data and was last lower in mid-2013. Nonmanufacturing slips in Q1 2016 too, to a standing of 18 from 19 but still has a 96th percentile standing. The all industry outlook slips by a point too, to 13 from 14 and has a 71st percentile standing.

Japan's weakness is centered in manufacturing and in business-related sectors. These sectors used to be its strength. Current performance is still relatively good, but the outlook is worse than current performance in all sectors.

Medium and small tankan responders show approximately the same pattern with relatively firm-to-strong current readings but with outlooks that are worsening.

Japan continues to struggle with deflation. Its battle is harder than elsewhere since Japan has a shrinking population. Various external factors have intruded on Japan's ability to reflate. The most recent is the tight trading relationship it has with China at a time that China is undergoing a pronounced slowdown.

Japan is closed off from fiscal measures because its national debt is so high. And its intent to implement further rounds of tax hikes also hangs over the economy. The tankan shows a relatively robust level of activity in Japan. In some ways the current reading is surprisingly strong. But the outlook shows a loss of momentum led by encroaching weakness in the manufacturing sector. Japan's real challenges still lie ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief