Global| Oct 01 2020

Global| Oct 01 2020Japan's Tankan Escapes the Deep Dive of Pessimism

Summary

There are always several different views of the reality of economic analysis and forecasts. Each observer has a different, or parallax, view reflecting different interests, expectations or methods of analysis. Still, there are certain [...]

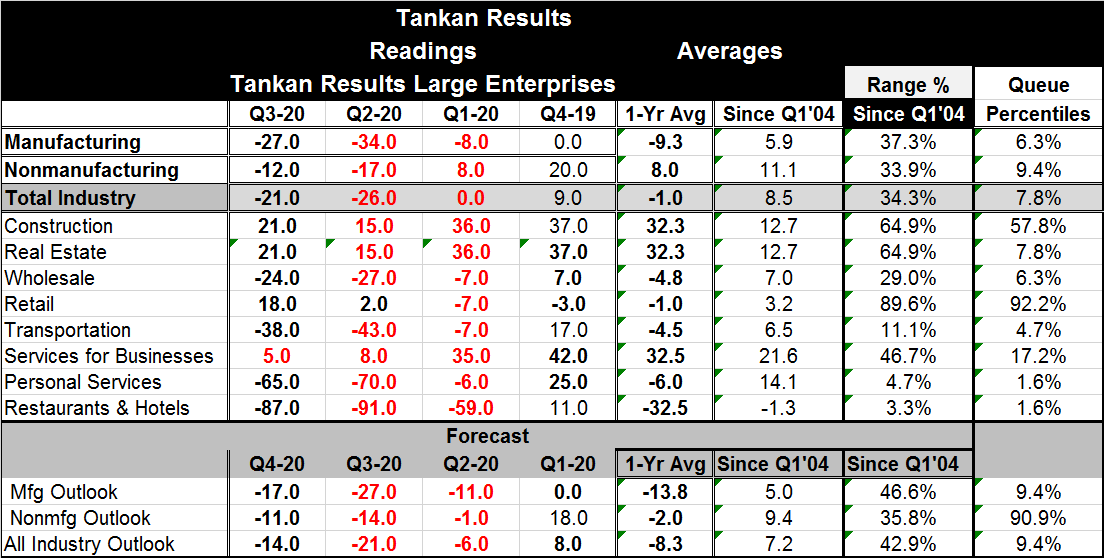

There are always several different views of the reality of economic analysis and forecasts. Each observer has a different, or parallax, view reflecting different interests, expectations or methods of analysis. Still, there are certain truths that transcend these differences. This month in Japan, the Tankan report's one truth is that the quarterly change in the manufacturing current index is large. It is the ninth largest quarterly gain in the last 163 quarters of the index. Yet, the ranking of the level of the reading in Q3 2020 is still very low in the bottom 6.3% among all historic quarterly readings. That seeming contradiction is explained by the ranking of the year-on-year change which comes in as only the 124th strongest out of 160 observations. That is a lower 11% standing. What the Tankan is telling us this quarter is that the abject pessimism that has been creeping into the survey in the wake of trade wars and coronavirus has lifted as the quarterly reading rose sharply. However, concerns about the future and the strength of recovery remain a reality. The Tankan respondents see poor conditions prevailing, but they are also willing to recognize improvement and even to see improvement continuing.

There are always several different views of the reality of economic analysis and forecasts. Each observer has a different, or parallax, view reflecting different interests, expectations or methods of analysis. Still, there are certain truths that transcend these differences. This month in Japan, the Tankan report's one truth is that the quarterly change in the manufacturing current index is large. It is the ninth largest quarterly gain in the last 163 quarters of the index. Yet, the ranking of the level of the reading in Q3 2020 is still very low in the bottom 6.3% among all historic quarterly readings. That seeming contradiction is explained by the ranking of the year-on-year change which comes in as only the 124th strongest out of 160 observations. That is a lower 11% standing. What the Tankan is telling us this quarter is that the abject pessimism that has been creeping into the survey in the wake of trade wars and coronavirus has lifted as the quarterly reading rose sharply. However, concerns about the future and the strength of recovery remain a reality. The Tankan respondents see poor conditions prevailing, but they are also willing to recognize improvement and even to see improvement continuing.

The Tankan is a comprehensive survey of a host of industries each quarter and of firms of different sizes within those industries, but it is the large-firm manufacturing portion of the survey that serves as its bellwether. This index rose sharply in Q3 to -27 from -34, but in Q4 2019 it had stood at zero. The large company manufacturing index in the Tankan had been slowing for a number of quarters. From Q2 2017 through Q4 2018, it had been steadily in the range of 20-25. In early-2019, it slipped out of that range and slid all the way to zero in the fourth quarter as Japan's two largest trading partners engaged in a tit-for-tat trade war slapping restrictions on one another's products. Then, in 2020 the coronavirus rose up from China and spread. That was the final straw and it sunk the tankan reading to new lows for this cycle. Fortunately, in Q3 the erosion has been stopped and a turning is in evidence.

Both manufacturing and nonmanufacturing firms show some improvement in their situation in Q3 compared to Q2. Despite the monthly improvements all the sectors are weaker year-on-year except for retailing. Retail has improved by a net of 14 points from its value in Q3 2019. Retailing is leading the way higher. Restaurants and hotels are the most severely impacted with a 96-point loss from Q3 2019 to Q3 2020. This is clearly a problem related to the virus and the inability to put certain businesses back in gear because of their dependence on close social contact.

The outlook survey finds manufacturers better by 10 points in Q4 than they were in Q3. However, the percentile standing for this measure at 9.4% is even a bit weaker than as the standing for the Q3 current tankan assessment for manufacturing firms. Nonmanufacturers see a three-point gain in the outlook in Q4 compared to Q3.

On balance, this Tankan survey is both reassuring and sobering. The worst of the recession appears to be behind Japan. Yet, the current and expected paths of improvement seem to be slow.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief