Global| Sep 08 2017

Global| Sep 08 2017Japan's Surplus Hovers As Trends Steady

Summary

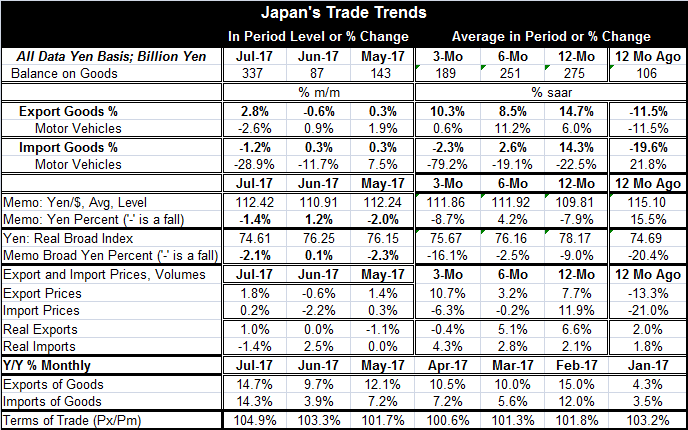

Japan's trade surplus continues to log positive readings and sports a higher reading at 337 billion yen in July, up from 87 billion yen in June. The surplus is the highest since February and about double the values posted from March [...]

Japan's trade surplus continues to log positive readings and sports a higher reading at 337 billion yen in July, up from 87 billion yen in June. The surplus is the highest since February and about double the values posted from March through May. Even so it is only one month and the reading, while an outlier of sorts by recent standards, is still only back in the pack of values it had posted in 2016.

Japan's trade surplus continues to log positive readings and sports a higher reading at 337 billion yen in July, up from 87 billion yen in June. The surplus is the highest since February and about double the values posted from March through May. Even so it is only one month and the reading, while an outlier of sorts by recent standards, is still only back in the pack of values it had posted in 2016.

Also year-over-year nominal growth rates for exports and imports have steadied in 2017. There is some variability but little sense of any change in trend after both of them have recovered from 2016 growth rate lows.

Sequential nominal growth rates are reasonably stable for exports but showing deceleration for imports.

The real thing...

However, sequential growth rates for export and import volumes show the opposite trends with exports slowing from a growth range of 5% to 6.5% over 12 months and six months to showing a slight contraction over three months. Imports, contrarily, are mildly accelerating in real terms from 2.1% over 12 months to 2.8% over six months to 4.3% over three months. Of course, none of these are dramatic moves and given the volatility in monthly data these patterns may not persist. And one thing is clear: that is whatever growth horizon one inspects both exports and imports broadly have been decelerating with small differences among the sequential comparisons. So that both exports and imports expressed in real terms are broadly pointing to slower growth or to growth stabilizing at modest rates of growth.

There is nothing in Japan's trade trends that is supportive of the idea that either Japan's economy is picking up or that exports are picking up because foreign growth is picking up.

Just today Japan actually trimmed back its own Q2 growth rate to the 2.5% region taking it down from the 3% region it seemed to have achieved with its preliminary results. Also the economy watchers index, a well-known service sector gauge, was unchanged month-to-month at a reading just below the mark of 50, suggesting some contraction from this diffusion-type survey.

The data from the Asia region showed that China's exports have slowed to 5.5% in August from 7% in July. That trend is also in sync with what we are seeing in Japan's own trends.

While Japan's exchange rate has recently moved abruptly higher, the move is nascent and on trade data through July the yen keeps its fading characteristics. On fresher data looking forward, the exchange rate change is going to tend to being unchanged over 12 months.

The global scene: better, but not improving

The global scene: better, but not improving

While there has been some interest in the theme of global revival and acceleration, the Markit global indexes show that while there has been a revival relative to 2016 weakness, since the end of 2016 globally conditions have been more or less flat in both the services and manufacturing sectors. PMIs are nowhere near the peak readings in 2015 or 2014 nor do they appear to be headed in that direction presently. Today's Japan trade data and other indicators and China's faded export growth are both in sync with this observation. Conditions are better, but there is little evidence of acceleration.

Policy

The Federal Reserve in the U.S. and the European Central Bank in Europe may be getting ready to abandon their most stimulative policies but remember that growth has been achieved for these current conditions with that stimulus in the mix. Since there is no evidence of acceleration, it is not clear what happens to growth or to momentum if any of the special stimulus programs are removed. Maybe the time is ripe to stop them. Maybe these economies' private sectors are ready to make up for what the central banks are preparing to take away...and maybe not. Keep an open mind.

The behavior and reaction of the U.S. bond market is particularly notable as the Fed gets ready to shift gears. I was struck by comments from the NY Fed's President William Dudley last night that financial conditions have eased since the Fed has tightened because of stock market and bond market reactions. Mr. Dudley noted that this could be grounds for the Fed to expedite its tightening. I am struck by what a bad idea it would be for the Fed to 'fight the market' especially since 'the markets' have been so much better at handicapping growth than the Fed. The bond market does not act as if either inflation or stronger growth are around the corner even if the Fed (and Mr. Dudley) thinks so. I think policymakers are very confused. They are best off moving policy very slowly whatever they decide to do. I have little confidence that they will choose to do the right thing. But if they choose to do the wrong thing and do it slowly enough, the outcome might be surmountable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief