Global| Dec 21 2015

Global| Dec 21 2015Japan's Sector Indices Rise

Summary

Japan's all-sector index rose in October but only stands in the 68th percentile of its historic queue of values, the same as the construction sector. As we have seen in Europe and in the U.S., the manufacturing sector lags badly. The [...]

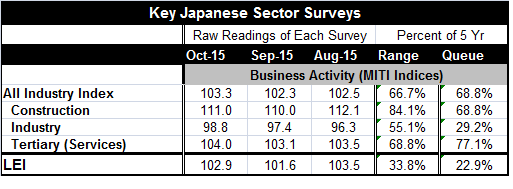

Japan's all-sector index rose in October but only stands in the 68th percentile of its historic queue of values, the same as the construction sector. As we have seen in Europe and in the U.S., the manufacturing sector lags badly. The industry standing is only in the 29th percentile of its historic queue. Also, as in Europe and the U.S., the services sector is the sector carrying growth. The services sector standing is in the 77th percentile of its historic queue of values, leading all sectors in its relative strength.

Japan's all-sector index rose in October but only stands in the 68th percentile of its historic queue of values, the same as the construction sector. As we have seen in Europe and in the U.S., the manufacturing sector lags badly. The industry standing is only in the 29th percentile of its historic queue. Also, as in Europe and the U.S., the services sector is the sector carrying growth. The services sector standing is in the 77th percentile of its historic queue of values, leading all sectors in its relative strength.

Weakest of all is the LEI which stands in its 22nd percentile as of October.

There are other indicators out that are slightly more topical. The economy watchers index stands in its 54th rank percentile in November. Construction stands as the strongest sector in the Teikoku framework in November, but manufacturing is still the weakest. Services is still the stalwart sector in the Teikoku framework.

As the chart aptly demonstrates, Japan's economy has pulled out of a period of extreme weakness from early-2014 through mid-2015. However, while the economy does not appear to be declining, its growth remains weak.

Japan, once helped, is now hampered by being in Asia where the growth miracle has tuned to nightmare. Taiwan reported today a drop in exports orders in November. China continues to struggle and the yuan is now on a path lower underlining the weakness in China, Japan's most important trading partner.

Japan has tough domestic problems. The international dimension is another large negative for Japan. The MITI indicators tell us that as bad as domestic problems are in Japan, the international problems are worse since the industry index is so weak. Japan's activity is marked compared to where it has been. But it is still extremely weak compared to where it must get in order to be sustainable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief