Global| Mar 19 2014

Global| Mar 19 2014Japan's Sector Indices Move Higher Ahead of Tax Hike; Will the Consumption Tax Be a Brick Wall to Abe-Nomics or a [...]

Summary

Japan's sector indices continue to turn higher in January. After a setback in December, the January all-industry index for Japan is moving back up. The level in January 2014 is above the level of November 2013, making the January [...]

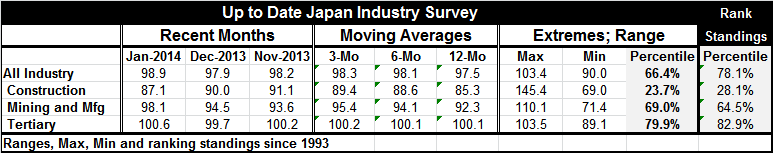

Japan's sector indices continue to turn higher in January. After a setback in December, the January all-industry index for Japan is moving back up. The level in January 2014 is above the level of November 2013, making the January recovery from the December swoon more than complete. The construction sector index fell in January compared to December; however, both mining and manufacturing and the tertiary sector (also known as the services sector) continued to press higher carrying the overall index up with them.

Japan's sector indices continue to turn higher in January. After a setback in December, the January all-industry index for Japan is moving back up. The level in January 2014 is above the level of November 2013, making the January recovery from the December swoon more than complete. The construction sector index fell in January compared to December; however, both mining and manufacturing and the tertiary sector (also known as the services sector) continued to press higher carrying the overall index up with them.

The past three-month, six-month, and 12-month moving-averages for the various sectors show steady progress. The weakest progress logged by these indices is for the tertiary sector which averages 100.1 for 12-months, 100.1 for 6-months and barely edges up to 100.2 over 3-months. Mining and manufacturing has moved up more vigorously from a 12-month average of 92.3 with its 3-month average at 95.4. Even construction, that has a recent setback, has a 3-month average of 89.4 compared with 12-month average of 85.3. The all-industry index progression has been from 97.5 over 12-months to 98.1 over 6-months to 98.3 over 3-months.

On the chart we see steady increases in construction, mining and manufacturing, and a slow and steady improvement in the services index. That's true even with the peeling back of construction in January. While there are still doubters about Abe-nomics, so far the improvement in the economy is still in gear. There has been some concern over the recent pickup in manufacturing that some of it might reflect a building of goods and purchasing ahead of the coming tax hike in Japan.

The coming increase in the consumption tax is certainly a very big hurdle the economy and will have to get over. Several times in the past, Japan, with the huge debt problems, has tried to implement some kind of a tax increase only to find that the economy was not strong enough to bear up under it. Although the central bank and the government have strongly jawboned that they're ready to support economic growth - even in the face of this tax hike- only time will tell if they have the tools and the will to do this. We'll have to see what kind of headwinds the economy actually is facing.

According to the historic comparison of the current indices, Japanese industry is in relatively good shape at the moment with its tertiary index in the 78th percentile of its historic queue. That means the overall industry gauge has been higher about 22% of the time. That makes the current reading relatively good but not exceptionally strong. It may be surprising to look at the chart, seeing the sharp recent rise in construction, but to find that the construction sector that has moved up so much is still quite weak and its historic context. The construction sector is only in the 28th percentile of its historic queue; that means it is weaker only about 28% of the time. Mining and manufacturing is in the 64th percentile of its historic queue. That means it's weaker than the all-industry index, but it is considerably above its median standing which occurs at a rank standing of the 50th percentile. So it is some nearly 15 percentage points above its median. The tertiary index which we can see from the chart has had a very steady menu of increases is nearly in the 83rd percentile of its historic queue. It's higher only about 17% of the time, slightly better than the all-industry index. This is a firm reading, but still not a super strong reading. All of this suggests that while Japan's economy has made some gains, it's not really in a strong position to absorb shocks that might come from the consumption tax. At the same time the international economy is still struggling. There has been some complaint that Japan is not getting the benefit that it would like to see from its export sector.

In assessing Japan we have to admit that it still has forward momentum, but it's about to hit some rather severe headwinds as consumption taxes take hold. Japan's exports continue to try to make headway in an environment where global growth is quite impacted. And since Japan has recently reset its trade to have more commerce with China, the recent underperformance of the Chinese economy is going to hit Japan more than the recovery in Europe and ongoing growth in United States is going to help. The next few months for Japan could be extremely important for its economy as well as for our assessment of the efficacy of Abe-nomics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.