Global| Jul 13 2017

Global| Jul 13 2017Japan's Retail Sales Drop in May But Stay on Trend Rise

Summary

Japan's retail sales fell by 0.5% in May, only partly negating the strong rise of 1.6% in April. As a result, sales are still strong, rising at a 6.8% annual rate over three months on a seasonally adjusted basis. Japan's sales are up [...]

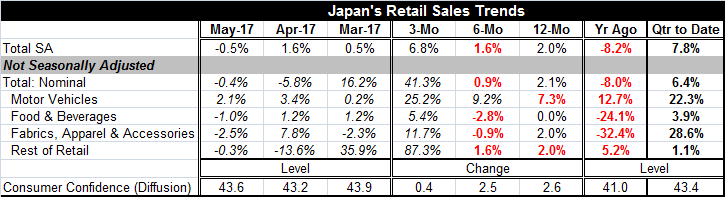

Japan's retail sales fell by 0.5% in May, only partly negating the strong rise of 1.6% in April. As a result, sales are still strong, rising at a 6.8% annual rate over three months on a seasonally adjusted basis. Japan's sales are up by 2% over 12 months then eased to a 1.6% pace over six months, but even with the drop in May, sales are up at that strong 6.8% three-month pace in May. In the quarter-to-date, sales are up at a stronger 7.8% pace, also seasonally adjusted.

Japan's retail sales fell by 0.5% in May, only partly negating the strong rise of 1.6% in April. As a result, sales are still strong, rising at a 6.8% annual rate over three months on a seasonally adjusted basis. Japan's sales are up by 2% over 12 months then eased to a 1.6% pace over six months, but even with the drop in May, sales are up at that strong 6.8% three-month pace in May. In the quarter-to-date, sales are up at a stronger 7.8% pace, also seasonally adjusted.

Japan's retail sales data have strong seasonal components and you can tell that by comparing the not seasonally adjusted total data with the seasonally adjusted total series in the table. The sequential detail in the components will not tell us much about true trends.

But compared to one year ago, sales are doing much better and 12-month growth rates are fair game for comparisons and are much less distorted for not seasonally adjusted data. One year ago the year-on-year growth for overall sales, for food & beverages, and for fabrics, apparel & accessories all were showing contraction. By comparison, all of those are in the growth column for year-on-year changes in May 2017 except for food and beverages where growth has nonetheless improved but is simply flat. However, both motor vehicles and the rest of retail are showing weaker year-on-year growth in May 2017 than they demonstrated in May 2016.

Japan is not growing fast, but the signs for growth are still positive. Consumer confidence in 2017 is 2.6 points higher than it was one year ago in May 2016. And while confidence rose in May, it is still struggling to do better. On a quarter-to-date basis, confidence is only unchanged for its April-May average compare to Q1 level.

Bank of Japan policy continues to be strongly accommodative with strong language underpinning its intent for the future. But on the political side, Prime Minister Abe has run into some difficulties and has had some setbacks perhaps making any further nonmonetary initiatives on his part harder to envision. Moreover, Japan's confidence measure is a diffusion metric; and while it has been improving at a level of 43.6 in May, it is still below the neutral level for confidence which occurs at 50. The average Japanese consumer is still more likely to be pessimistic than optimistic about his or her situation.

Policy in Japan still faces some steep challenges. But the good news for Japan on the day was the stronger export growth in China since China is Japan's largest trade partner and since Japanese firms have operations in China. Any picking up of global growth would be an assist for Japan's growth. Japan probably has about as much monetary stimulus in train as the Bank of Japan can muster. Anything other than minor political tweaking is probably out of bounds for Japan's fiscal policy. Japan's best bet for unexpected good news is a pick-up in global growth. The global manufacturing PMI has in fact been on the rise and while global services metrics have flattened and sagged, the pick-up in manufacturing globally is hope for Japan and for all exporting nations.

Policy in Japan still faces some steep challenges. But the good news for Japan on the day was the stronger export growth in China since China is Japan's largest trade partner and since Japanese firms have operations in China. Any picking up of global growth would be an assist for Japan's growth. Japan probably has about as much monetary stimulus in train as the Bank of Japan can muster. Anything other than minor political tweaking is probably out of bounds for Japan's fiscal policy. Japan's best bet for unexpected good news is a pick-up in global growth. The global manufacturing PMI has in fact been on the rise and while global services metrics have flattened and sagged, the pick-up in manufacturing globally is hope for Japan and for all exporting nations.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief