Global| Jun 12 2017

Global| Jun 12 2017Japan's PPI Declines in May

Summary

Over the last 10 years, Japan's PPI has had a nice tracking relationship with Japan's CPI. Of course, the PPI is more volatile than CPI inflation, with PPI inflation rising faster than CPI inflation when inflation is rising and [...]

Over the last 10 years, Japan's PPI has had a nice tracking relationship with Japan's CPI. Of course, the PPI is more volatile than CPI inflation, with PPI inflation rising faster than CPI inflation when inflation is rising and falling faster than CPI inflation when inflation is falling. During this period, the PPI can explain about 47% of the variance in the CPI.

Over the last 10 years, Japan's PPI has had a nice tracking relationship with Japan's CPI. Of course, the PPI is more volatile than CPI inflation, with PPI inflation rising faster than CPI inflation when inflation is rising and falling faster than CPI inflation when inflation is falling. During this period, the PPI can explain about 47% of the variance in the CPI.

However, recently the CPI has been resisting the charms of the PPI. From early-2015 until late-2016, the PPI was falling at pace of up to a 4% annual rate while the CPI stayed close to home while dropping at a pace no greater than one-half of 1% per year. Now the PPI is up to 2% per year and the CPI is dawdling at a year-over-year pace of about 0.4%.

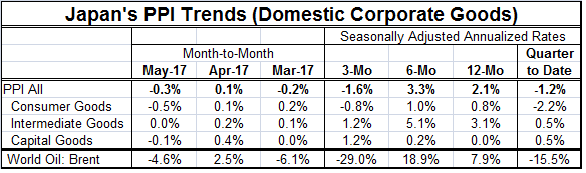

Obviously the PPI has been kicked around by oil prices. Over this period oil explains about 32% of the variance in the PPI. The table shows that episodes of PPI decline line up with episodes of Brent oil price declines.

In the merry month of May the PPI is falling by 0.3% after ticking up in April and falling in March. There is no clear acceleration/deceleration pattern in Japan's PPI over the past year. Among the PPI categories, only the capital goods sector shows any trend and for it there is a mild uptrend with inflation flat over 12 months then rising at a 1.2% annualized pace over three months. In general, there is nothing here to make the BOJ think that it is winning its battle to boost consumer inflation to 2%.

In the quarter-to-date, the PPI is falling at a 1.2% annual rate with consumer goods prices (at the producer level) falling at a 2.2% annual rate as intermediate and capital goods prices are advancing at a 0.5% annualized pace in Q2.

And in Q2, Brent prices are still falling (so far).

In a separate report today, Japan revealed that core machinery orders fell by 3.1% in April. A gain had been expected. Even though the core orders series is designed to omit the lumpiest series, it is still a relatively volatile report. Total foreign orders showed a sharp rise in April gaining 17.4% while domestic demand shriveled at a 3.6% pace. Year-on-year total orders are up by 2%, core orders are up by 3.6%, foreign orders are up by 8.8% and domestic orders are lower by 1.7%. There is some strength in the order series, but it is not from domestic demand. Japan's economy is having a hard time getting into gear and growing steadily enough to generate the inflation targeted by the BOJ.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief