Global| Jan 14 2021

Global| Jan 14 2021Japan's Orders Are Mixed and Its Surveys Are Weak

Summary

Japan's industrial orders were mixed in November with headline orders falling by 1.5% and core orders rising by 1.5%. Year-on-year the comparison is exactly opposite with total orders rising by 1% and core orders lower by an outsized [...]

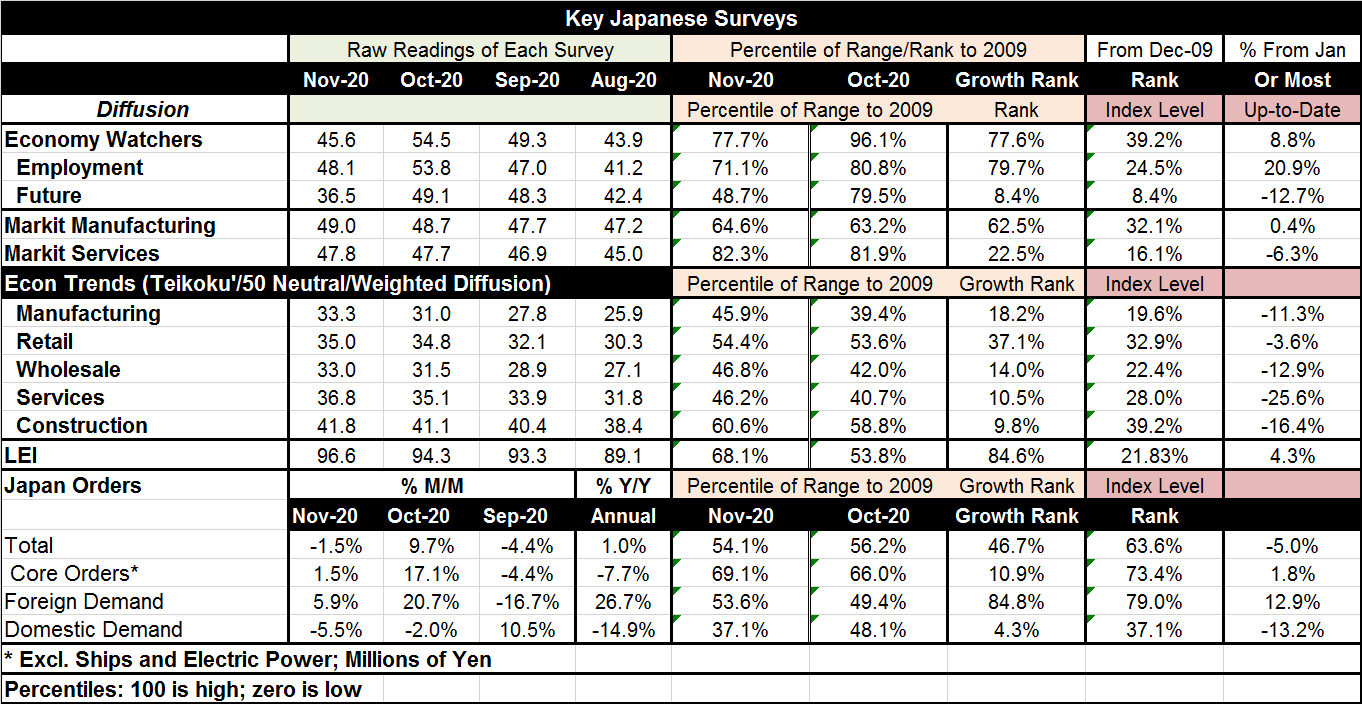

Japan's industrial orders were mixed in November with headline orders falling by 1.5% and core orders rising by 1.5%. Year-on-year the comparison is exactly opposite with total orders rising by 1% and core orders lower by an outsized 7.7%. The October to November turn is mixed across indicators with the turn itself favoring strength, but the overall performance of the fifteen measures tending more to weakness.

Japan's industrial orders were mixed in November with headline orders falling by 1.5% and core orders rising by 1.5%. Year-on-year the comparison is exactly opposite with total orders rising by 1% and core orders lower by an outsized 7.7%. The October to November turn is mixed across indicators with the turn itself favoring strength, but the overall performance of the fifteen measures tending more to weakness.

The table below chronicles a number of well-watched Japanese indicators through November. Five indicators weaken month-to-month and 10 improve month-to-month. However, in terms of the growth ranking that looks at the ranking of the year-on-year percentage change in an indicator, only five have a rank above 50 meaning that only five are above their historic median one-year gain. The rest fall short of that. We can also look at the ranking of the levels of these variables since many of them are diffusion indexes (LEI and orders excepted). Rankings based on levels find only three above the 50% mark and all of those are in the orders section where level comparisons are less relevant.

Assessments

Foreign orders (foreign demand) rank above their median measured either in terms of the level of the index or its year-on-year change. The LEI is stronger in its rate of its growth ranking than its level ranking. The economy watcher index and its employment components both are stronger on their growth ranks (which are quite solid) that on their level ranks (that are quite weak)-and that survey uses diffusion indexes, so the level reading is relevant. Apparently, the economy watchers index shows a strong pick up year-on-year that still leaves the level of the reading weak. All the Teikoku indexes (that also are diffusion indexes) are weak whether expressed as levels or as changes over the past year. Of course, orders are boosted by their foreign component that shows strength and helps total orders to firmness or near firmness overall. Still, core orders are weak on growth which is a key metric for assessment and domestic demand scores weak standings for both growth and level measures.

Since January 2020

Of course, the Covid-19 virus has been percolating in Japan over most of the past year. Comparisons of the November levels with levels in January allow some evaluation of how these various metrics have performed since the virus hit. Of the fifteen categories in the table, only six are higher than their January levels. These include two of the economy watcher measures, the Markit manufacturing gauge, the LEI, and in the order section, core orders and foreign demand. The Teikoku diffusion indexes show the weakest readings with drops of 25.6% for services, 16.4% for construction and nearly 13% for wholesaling, while in the orders sector domestic demand is 13.2% lower and the Markit services gauge is 6.3% lower. Clearly where services are highlighted the surveys show more weakness. And while the slippage of the Markit and the Teikoku indexes is different, the percentile standings for services on the two diffusion gauges are actually quite similar.

Japan and the virus

The data mentioned are through November 2020 while in real time it is mid-January 2021. As of mid-January, a Bank of Japan survey finds improvement in three of nine regions. However, the state of emergency declared in Tokyo is being broadened to include more prefectures. That is a bit of a mixed signal from Japan.

Summing up

The virus is still really the only game in town globally. It determined what can and what can't be done. As of this moment, the virus is still spreading and countries are struggling to get their vaccine rollouts on better footing. The U.K. has finished some work on infections and immunity and concluded that after infection a person has immunity for about 5 months giving them a much lower probability of catching the virus again (lower by about 83%). But it warned that people can ‘catch it again.' This casts some doubt on the role of herd immunity beyond a few months. In any event, that does not apply to Japan where infection has been so much less widespread. But it does apply to the U.S. and Europe where infection has spread considerably more and where herd immunity may actually be more of a possibility. The U.K. continues to urge mask-wearing for those who have been infected even well after they have dispatched the disease. Of course, the incidence of mask-wearing and ‘concern for your fellow man' has always been higher in Japan.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief