Global| Sep 01 2017

Global| Sep 01 2017Japan's Manufacturing PMI Ticks Higher in August

Summary

Japan's manufacturing diffusion PMI gains to 52.2 in August from 52.1 in July. The manufacturing sector is showing growth, but it has no momentum. As it turns out, that is a theme for early PMI reports in Asia. The August reading is a [...]

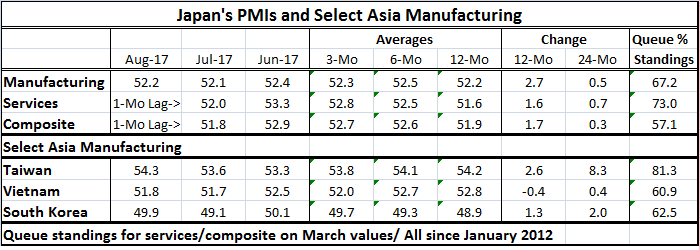

Japan's manufacturing diffusion PMI gains to 52.2 in August from 52.1 in July. The manufacturing sector is showing growth, but it has no momentum. As it turns out, that is a theme for early PMI reports in Asia. The August reading is a tick below its three-month average and below its six-month average and only even with its 12-month average. The five-year percentile standing for manufacturing is at its 67th percentile, just inside the top one-third of its five-year queue of values. Still, the 12-month changes show that Japan's manufacturing PMI has gained 2.7 points in 12 months compared to 0.5 over 24 months so the last year still has shown some solid gains and a step up from Japan's PMI.

Japan's manufacturing diffusion PMI gains to 52.2 in August from 52.1 in July. The manufacturing sector is showing growth, but it has no momentum. As it turns out, that is a theme for early PMI reports in Asia. The August reading is a tick below its three-month average and below its six-month average and only even with its 12-month average. The five-year percentile standing for manufacturing is at its 67th percentile, just inside the top one-third of its five-year queue of values. Still, the 12-month changes show that Japan's manufacturing PMI has gained 2.7 points in 12 months compared to 0.5 over 24 months so the last year still has shown some solid gains and a step up from Japan's PMI.

Japan's services sector reading still lags by one month; as of July, the PMI fell relative to June. And the services PMI's averages have been gradually strengthening over shorter periods. Like manufacturing, services have made a slightly greater gain over the last 12 months. Moreover, the services sector shows more strength overall with a 73rd percentile queue standing.

Elsewhere in Asia

Early PMI readings elsewhere in Asia from Taiwan, Vietnam and South Korea show similar conditions to Japan's manufacturing sector. By that, I mean not robust and not accelerating. In terms of the queue standings, Vietnam and South Korea are a bit weaker than Japan; Taiwan is considerably stronger.

In terms of the outright level the PMI readings, Taiwan is stronger than Japan while both Vietnam and South Korea are weaker. South Korea, despite improving in August, is still below the 50 mark showing a minor contraction.

In terms of the various sector averages, all of the sequential trends by country are relatively flat; only Korea shows sequential improvement, but its raw PMI in August is still showing contraction.

The 12-month change in Taiwan's manufacturing PMI is comparable to the 12-month change in Japan. Both Vietnam and South Korea trail that gain. Taiwan shows a huge slowdown over the last 12 months compared to the previous 12 months unlike any other country in the table. Taiwan's 12-month gain pales next to its 24-month gain.

Outlook

Despite some optimism about global manufacturing, there is very little that is upbeat out of this sample of countries in Asia. Only Korea is not signaling growth, but it is getting closer to showing expansion. Growth in Asia can hardly be called robust. The level of activity in Taiwan is still 'elevated' on its PMI scale but it is lacking momentum and over the last year its momentum has slowed markedly.

If Asia is supposed to be driving growth, right now it is pulled over to the rest stop. U.S. reports show growth, but the August jobs report will shed new light on that. Fresh U.S. and European inflation news shows inflation is still behind its targets with U.S. inflation looking just a bit more sluggish than had been expected. Also U.S. consumer spending is off to a modest start in Q3. Europe's data have been more upbeat, but the PMI data from Europe put more optimistic spin on growth that do the recent labor market data, for example. Optimism is only where you find it and only there if you emphasize the right reports. It is not obvious.

The reported slow progress in the UK-Europe Brexit talks is not good news. Apparently Europe is willing to cut off its nose to spite its face to teach the U.K. and anyone else with a mind to leave the EU an unforgettable lesson. The outlook for growth stands in the balance as this approach is bad for everyone. Moody's has recently let some of its forecasts tick higher, but by and large the global output picture has not changed. Still, there has been a sense of growing optimism. Will it be justified?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief