Global| Jul 09 2015

Global| Jul 09 2015Japan's Machinery Orders Begin to Show Life

Summary

While overall machinery orders are still falling for two consecutive months in Japan, the more reliable series of core orders that excludes large and lumpy projects is showing steady and strong growth. Core orders are rising at a 25% [...]

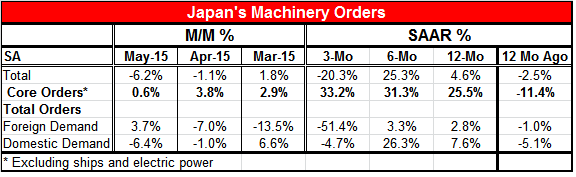

While overall machinery orders are still falling for two consecutive months in Japan, the more reliable series of core orders that excludes large and lumpy projects is showing steady and strong growth. Core orders are rising at a 25% pace over 12 months, a 31% pace over six months and a 33% pace over three months. These are quite elevated rates of growth. However, the chart shows that overall orders, too, are starting to find some stability at positive values in their 12-month growth rates.

While overall machinery orders are still falling for two consecutive months in Japan, the more reliable series of core orders that excludes large and lumpy projects is showing steady and strong growth. Core orders are rising at a 25% pace over 12 months, a 31% pace over six months and a 33% pace over three months. These are quite elevated rates of growth. However, the chart shows that overall orders, too, are starting to find some stability at positive values in their 12-month growth rates.

Twelve-month growth rates show that domestic demand has been stronger than foreign demand. The chart shows that foreign demand is relatively more erratic than domestic demand and has seen some big down-drafts recently.

Japan engages in a good deal of trade with China and the U.S. Its China trade has been under pressure as the Chinese economy has been slowing and shows some signs, like Japan in the past, of having overinvested in some key sectors notably housing. While the U.S. economy has been producing steadier growth and the strong dollar has increased American purchasing power for Japanese goods, the strong dollar also has made the U.S. a less competitive place to do business. That will diminish interest in purchasing capital goods even at relatively cheap prices. Europe, another substantial market for Japan, continues to struggle to maintain growth.

This is an old story of weak growth. While Japan's strong monetary stimulus policy has borne some fruit, its expansion has been cut back by its attempt to get control of the growth of its government debt by hiking its VAT tax. That consumption tax hike hit the economy hard and despite ongoing monetary stimulus Japan has been struggling to move ahead. The troubles in the overseas markets have doubled the challenge to get growth in gear despite the drop in the yen and its positive impact on Japan's competitiveness. So much of Japan's productive capacity has been moved offshore that the increase in competitiveness caused by a weaker yen is not as powerful an impact as the rise in domestic costs from the yen's lost purchasing power as the yen falls.

Japan continues to face challenges to growth. In addition to the weak yen not being an elixir for growth, Japan has a shrinking population and an aging population and those trends compound the difficulty of corralling excessive government debt and its growth.

For now there is some evidence of revival in Japan's key orders series for core machinery. But Japan's domestic economy is still sputtering; the overseas economies, while doing better, are still not a wonderland for growth. Japan is being held back by the same weak global growth environment that is affecting everyone else. Every country would like to benefit from export-led growth but that, of course, is impossible. In fact, global growth is so weak that few can benefit at all from export-led growth. And many economies, many of them in Asia, have been constructed to grow based on foreign demand. That is why China, Japan and South Korea are struggling, to name a few.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief