Global| Jun 18 2018

Global| Jun 18 2018Japan's Loses Its Trade Surplus

Summary

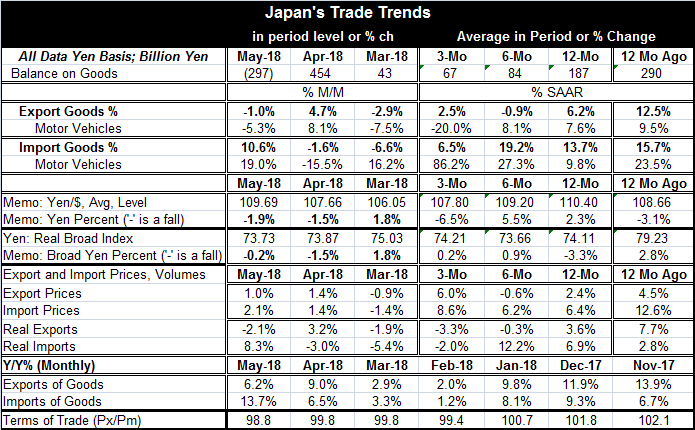

In May, Japan has logged its second trade deficit in 13 months and only its third in the last 28 months. Technically, the deficit was generated by a 1% drop in exports combined with a 10.6% surge in imports. The yen has been gradually [...]

In May, Japan has logged its second trade deficit in 13 months and only its third in the last 28 months. Technically, the deficit was generated by a 1% drop in exports combined with a 10.6% surge in imports.

In May, Japan has logged its second trade deficit in 13 months and only its third in the last 28 months. Technically, the deficit was generated by a 1% drop in exports combined with a 10.6% surge in imports.

The yen has been gradually rising against the dollar over the past year, but its overall situation is more complicated than that. The dollar sharply depreciated in May falling to 109.7 from April’s 107.7, a one month drop of 1.9%, corresponding to a 25% annual rate of decline. The yen also fell against the dollar for two months in a row at an annual pace of 19%. The broad real yen has been falling at a 10% annual rate over the last two months as well. Year over year, however, the yen is still rising vs. the dollar but its falling on a real broad trade-weighted basis. Japan does most of its trading with China. The United States is Japan’s second largest trade partner. Exchange rate movements vs. China dominate movements in the real broad yen index.

In part because of these exchange rate movements, Japan’s export prices are rising by 2.4% over 12 months and faster over three months. Export prices tend to rise faster when a currency is weakening since exporters can increase their mark-up in domestic currency units and still drop their prices in foreign currency terms. Import prices are up by 6.4% over 12 months and rise even faster over three months. Import prices rise faster when a currency weakens as the higher cost of foreign exchange is added to the imported product’s price. So Japan’s exports and imports are reacting to a weakening yen. Import prices are rising faster than export prices, which is also what should happen when the yen weakens.

Japan’s trade flows in real terms show gains over 12 months with imports rising faster than exports in real terms. This should not continue if the yen continues to weaken, since a weakening yen makes imports more expensive. Weakening is what the yen is doing vs. the dollar over three months, but it is not doing that in real terms on a broad basis over three months. However, the broad real yen is moving very little recently.

Import and export prices are not just a function of currency movements; they also are due to domestic and foreign activity. Relatively stronger Japan imports compared to exports over 12 months suggest that Japan faces relatively mild demand for its goods in overseas markets while domestic demand is ramping up despite fast rising import prices – that should be short-lived. And the data are suggestive on this point as real imports are falling on balance over three months despite their one-month surge in May.

Of course, Japan’s domestic demand has not been very strong as GDP contracted in the first quarter. We would not expect such strong import demand at this time. Japan’s trade and its export and import price movements suggest some adjustment is in progress over trade flows and that the flows have not fully settled into their new trends.

Monthly data on the year-over-year changes in nominal exports and imports show that exports slowed through March and have since picked up. Imports have followed roughly the same profile.

The terms of trade are a shorthand method for gauging the welfare impact of exchange rate changes and other factors that affect export and import price developments. The ‘terms of trade’ refers to the export-to-import price ratio. When the terms of trade rise (improve), a nation’s welfare improves since it can sell goods for higher prices relative to purchases. When the terms fall, a country is getting less for its export sales relative to imports. This is, of course, a consumption view of the effect. Japan has been seeing its terms of trade fall over the last two years as the ratio 24 months ago was at 1.02 and 12 months ago it was 101.8 while in May it stands at 98.8. Looked at either way, exports are either bringing in less remuneration relative to imports or imports are costing more relative to exports. Another impact of this is that as the yen weakens Japan becomes more competitive. Goods may cost more, but jobs become more secure and job growth might even get stronger. For Japan, with a shrinking population, that is less of an enticement.

Japan’s economic position is hard to characterize. Its sector indexes are weakening according to the METI indexes and Teikoku indexes. Inflation, Chronically below target, has actually softened. On the bright side, Japan’s retail sales recently have shown some spunk. Still, Japan is in a difficult spot. U.S. ongoing negotiations with North Korea and trade sanctions hover over its head as either a direct or indirect problem. North Korean talks with the U.S. are ‘portrayed’ as having gone well, but there was nothing specific in the meeting to give Japan solace over North Korea’s missile tests or capacities. In addition, there is the trade row and the new, aggressive, U.S. posture. U.S. policy on metals tariffs is far ranging. But its most devastating attack is on China which has retaliated. China is Japan’s largest trade partner. The IMF has warned that there could be adverse effects from this aggression on global trade and growth. It is hard to handicap how much these concerns will affect growth and how much it might influence businesses to become more defensive and what the spillover effects might be. There are many things to weigh here. Japan itself has a lot of irons in these fires. Japan definitely faces outcome risk over the next few months. Odds are that it will not emerge unscathed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief