Global| Feb 28 2018

Global| Feb 28 2018Japan's IP Tanks, Housing Starts Plunge and Retail Sales Drop...What's Next?

Summary

Japan had more than a bad hair day as economic reports showed helter-skelter weakness. Industrial output in January fell by 6.6%, an astoundingly weak one month result. Retail sales fell by 1.2% in January. Housing starts in Japan [...]

Japan had more than a bad hair day as economic reports showed helter-skelter weakness. Industrial output in January fell by 6.6%, an astoundingly weak one month result. Retail sales fell by 1.2% in January. Housing starts in Japan fell by 13.2% year-on-year in January. Welcome to the land of the rising sun and the setting growth rate.

Japan had more than a bad hair day as economic reports showed helter-skelter weakness. Industrial output in January fell by 6.6%, an astoundingly weak one month result. Retail sales fell by 1.2% in January. Housing starts in Japan fell by 13.2% year-on-year in January. Welcome to the land of the rising sun and the setting growth rate.

Suddenly, the outlook for Japan is much murkier. The yen has risen vs. the dollar by about 5% this year, too small a gain to account for such widespread and devastating weakness. Some of this may be weather related as Japan was hit in January with some substantial snowfall; economic activity may have been adversely affected in a way that will also create a February rebound. But even if weather is a salient factor in play, the breadth and degree of the weakness seems to speak to a deeper problem.

Japan's growth seems set to slow in 2018. The early manufacturing PMI gauge for February in Japan is now available and it has also turned lower. That suggests that even if there is a February IP rebound in the making, it will not be substantial.

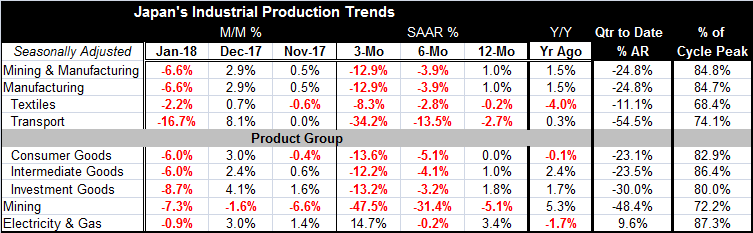

IP trends in Japan show sequentially collapsing trends across all sectors and industry groups except for electric and gas. This is a report for the first month of the quarter and it gets the quarter off to a terrible start with IP falling at a 24% annual rate quarter-to-date.

It is too early for Japan to be experiencing any cycle-related slowing as the IP level of activity is only back to the 85% mark of the previous cycle peak. However, there are suggestions that inventories have begun to be a problem and that may have led to a cutback in production. Still, a 6.6% one-month drop in IP does not seem like the result of some cutting back on output to relieve inventory pressure.

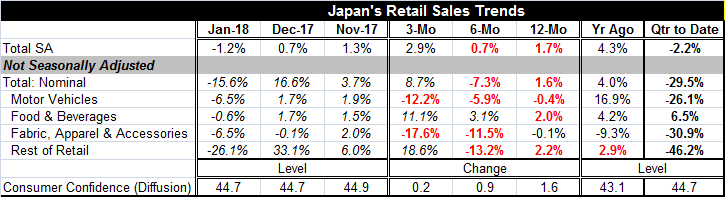

Japan's retail sales show a 1.2% drop in January (seasonally adjusted). The 'not seasonally adjusted' (NSA) data in the table show the extreme growth rate swings that retailing is experiencing this time of year as December is a huge ramp up month and January is a substantial contraction period. Over three months, seasonally adjusted retail sales still are doing relatively well despite the January drop. Three-month growth is at a 2.9% pace, up from a 0.7% pace over six months and still ahead of its year-on-year pace of 1.7%. On balance, retail sales are off in January which (as we can see from the NSA data) is a light month for (actual) sales anyway and not likely to be a month when sales results would substantially impact inventory levels. If retailers don't sell in December, that's an inventory problem in the making, not January.

Still, there is slowing apparent in retailing and consumer confidence in Japan has gotten sticky. Confidence is up over the past year, having rising by 1.6 points. But it has since flattened out and is off-peak. And this measure of confidence is a diffusion measure so its values below 50 tell us there are more pessimistic responses to the survey than there are optimistic responses. The small gain in confidence over the last 12 month has not remedied that condition.

In my report of yesterday (Global Monetary Center Action: Money Supply Growth Is Slowing), I flagged the declines in real money balances across major money center countries. I warned that could be an ominous signal. Today we see a small step back in China's manufacturing PMI which has logged a diffusion score of just 50.3, barely above the neutral reading of 50. And we see broad and deep weakness in Japan.

While GDP is still expanding, as a rule inflation is not gaining. Euro area inflation fell to a 14-month low in February. Central bankers seem to be in a state of confusion over what to do as they continue to harbor their worst fears of inflation finally rising and yet that continues not to happen. This could become a much bigger problem where policy is being made on forward-looking assumptions, like in the U.S.

Central bankers are loath to read the absence of inflation as saying anything about the potential for growth to continue. This approach has been fed by the persistence of job growth even though economic activity growth has remained tempered or boosted by some odd-ball facts as in the U.S. Unemployment in Japan remains low and labor market constraints are real, but in Europe and in the U.S., job gains have been strong and unemployment rates also are either low or falling or both. There is something about this period of weak prices and low inflation with 'strong job growth' which has produced of a lot of 'low end jobs' that has not jelled in the minds of policymakers. At the end of the day, they all seem taken in by the low unemployment rates. There is something sophisticated about this particular combination of growth with no inflation that begs for a deeper understanding.

Of course, Japan has special problems. It has a very rapidly aging, and now shrinking, population both of which give it special policy hurdles it must go over. But it still faces the same sorts of problems as other developed nations. Because Japan has also been fighting off deflation and striving harder than anyone else to hit its price objective of 2%, it is even more surprising that amid all the stimulus Japan is having problems getting both activity and prices in gear.

The global recovery is getting rather long in the tooth, but there are not bottlenecks or other capacity issues since growth has been so slow. Also there is so much trade and access to other countries' markets and such rapid capacity growth, especially in Asia, that it is far easier to understand why inflation has not risen. But in the U.S. the recent monetary report from the central bank largely down plays global arguments and clings to the inward-looking and still malfunctioning 'Phillips Curve' as the answer. If the Phillips curve is the answer, what the heck is the question?

What has been most lacking globally has been demand not supply. The German economy that is growing so well is substantially driven in Q4 by export sales. In the U.S., stronger exports are being touted along with a more stimulative fiscal policy as reasons for growth optimism. But surely everyone can't live by export-led growth? There is some sort of economic accounting fallacy in that.

While everyone is so enraptured about the coming growth acceleration, I think we have to be prepared for disappointment. Even in the U.S. where there is fiscal stimulus, there has to be some care taken to consider how this 'stimulus' was bought; it was bought by mortgaging the financial probity of the future. At some point, economic agents are going to take that into account. Japan already is limited in what stimulus it can consider because of its debt-to-GDP ratio. Italy in Europe has another large debt-to-GDP ratio and it has been stuck nearly flat-lining in this recovery without access to a fiscal remedy because of Maastricht rules. I remain concerned about the future and do not take the notion of a ramp-up in growth in 2018 as given for any country or region. As this year begins to unfold, there seems to be more questions than answers and more question marks than exclamation marks. It's a good time to make your investment decisions one step at a time. In fact, this is one reason why U.S. fiscal policy may not be so potent. There is not a tight relationship between the cost of capital and investment. And with that as a background fact, we do not see U.S. capital spending plans going through the roof in the wake of the new Trump fiscal plan. And if U.S. fiscal stimulus is a disappointment, I'm hard-pressed to see demand ramping up elsewhere. Could Japan's disappointing January be the start of a new global trend?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief