Global| Nov 30 2015

Global| Nov 30 2015Japan's IP Marks a Strong October Gain

Summary

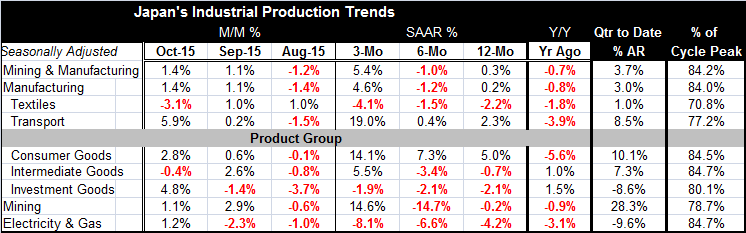

Japan's industrial production index rose by 1.4% in October, pushing the three-month growth rate up to 5.4% annual rate. Manufacturing now has two consecutive monthly gains of more than 1%. Still, growth is negative on balance over [...]

Japan's industrial production index rose by 1.4% in October, pushing the three-month growth rate up to 5.4% annual rate. Manufacturing now has two consecutive monthly gains of more than 1%. Still, growth is negative on balance over six months and weak over 12 months. Back-to-back monthly strength may not be decisive. Despite two previous monthly gains in textiles of 1%, textile output collapsed in October; that sector shows shrinking output up and down the timeline. If October marks a change in direction for output, we cannot see it in the trends yet.

Japan's industrial production index rose by 1.4% in October, pushing the three-month growth rate up to 5.4% annual rate. Manufacturing now has two consecutive monthly gains of more than 1%. Still, growth is negative on balance over six months and weak over 12 months. Back-to-back monthly strength may not be decisive. Despite two previous monthly gains in textiles of 1%, textile output collapsed in October; that sector shows shrinking output up and down the timeline. If October marks a change in direction for output, we cannot see it in the trends yet.

Manufacturing output is up at a 4.6% pace over three months, shrinking over six months, and up by 0.2% over 12 months. By product group, consumer goods output remains strong. Output in that sector rose by 2.8% in October and is rising at a 14.1% annual rate over three months and clearly accelerating from 12 months to six months to three months. But the consumer goods sector is the lone bright spot. Investment goods output is shrinking at a steady 2% pace over all horizons, despite a sharp rise of 4.8% in October. Intermediate goods output has been running hot and cold over the last three individual months. But over that span as a whole, there is a strong 5.5% annual rate gain. Yet, that gain juxtaposes to a 3.4% rate of decline over six months and a drop of 0.7% over 12 months.

Mining output has had a similar patch of strength over three months matched by severe weakness over six months and an output decline over 12 months. Electricity and gas production show clearly declining trends and decelerating growth.

However, because there has been strength in October, the quarter-to-date calculations show solid growth. With overall IP up at a 3.7% pace, there are strong gains in consumer goods and intermediate goods output quarter-to-date. However, investment goods output is falling quarter-to-date at a severe 8.6% annual rate. And while mining output is up at an extreme 28.3% annual rate, electricity and gas production are falling at a 9.6% annual rate. Utilities output is often taken as a proxy for overall growth. And that metric points to weakness.

The final column in the table tells the real story of Japan's industrial production in perspective. IP overall is only at 84% of its prerecession peak. In fact, no sector has shown an ability to retake its past cycle level of output. Textiles is the weakest sector at only 70% of its past peak output, while intermediate goods and electricity and gas production have come the closest to recouping their respective past cycle peak levels but each is still more than 15% short.

Japan is showing some rebound in October. But it's a rebound that does not yet have a clear base of strength either domestically or internationally. At home Japan's consumer confidence is still very weak. Abroad Japan's largest trading partner, China, continues to struggle. The October surge in IP is welcome and having strong gains for two consecutive months is encouraging, but it still is not enough to instill real confidence.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief