Global| Oct 30 2020

Global| Oct 30 2020Japan's IP Is Recovering

Summary

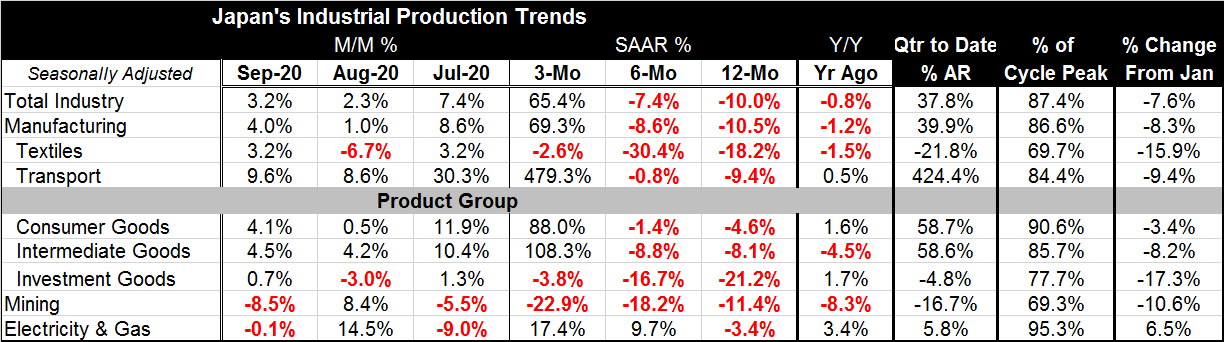

Japan's industrial production is up by 3.2% in September. IP is growing at a 65.4% annual rate over three months, but it is sill contracting on balance over six months and 12 months. The fire under IP in recent month is still not [...]

Japan's industrial production is up by 3.2% in September. IP is growing at a 65.4% annual rate over three months, but it is sill contracting on balance over six months and 12 months. The fire under IP in recent month is still not enough to boost IP to an output expansion over either six months or 12 months.

Japan's industrial production is up by 3.2% in September. IP is growing at a 65.4% annual rate over three months, but it is sill contracting on balance over six months and 12 months. The fire under IP in recent month is still not enough to boost IP to an output expansion over either six months or 12 months.

Moreover, overall IP, manufacturing IP, textiles and transportation all showed increases in September and strong increases at that. By sector, consumer goods output was very strong as was intermediate goods output. Investment goods output goods output increased only by 0.7% in September.

Looked at more broadly, consumer goods output is up at an 88.0% annual rate over three months, Intermediate goods output is up at a 108.3% pace over three months. Investment goods output is declining over three months at a 3.8% annual rate.

Year-on-year overall IP is lower by 10.0%. Consumer goods output is off by 4.6% and investment goods output is down 21.2%. Intermediate goods output is lower by 8.1% as all sectors show declines.

Quarter-to-date, Japan's output is expanding sharply up at a 37.8% annualized rate from Q2. Manufacturing is up at a 39.9% annualize rate. Consumer goods, investment goods, and intermediate goods output all are up at annualized rates that ranges from -4.8% to 58.7%. It is investment goods that are lagging in the quarter.

If we walk back to January before the coronavirus has really been spreading, we find that Japan's IP is lower by 7.6% from that date. Manufacturing is lower by 8.3%. Consumer goods output is lower by 3.4% with investment goods lower by 17.3%. Intermediate goods output is lower by 8.2%. Japan is still in a recovery mode over the Covid-19 period.

Japan, while showing some solid current period rebounding, is still not having enough rebound to offset previous weakness. That is why the year-over-year comparisons are showing net output declines and the change since January show declines across the board. There is still a lot of work to do to make up for lost time for output and in manufacturing in Japan.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief