Global| Aug 31 2018

Global| Aug 31 2018Japan's IP Edges Lower

Summary

Industrial production fell in Japan for the third consecutive month. While the July drop was small, the three-month growth rate shows a sizeable decline in the works. IP in the developing third quarter is falling on a quarter-to-date [...]

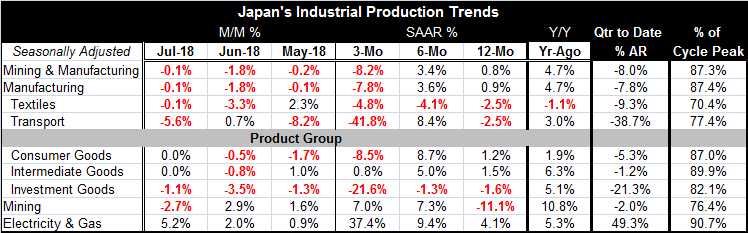

Industrial production fell in Japan for the third consecutive month. While the July drop was small, the three-month growth rate shows a sizeable decline in the works. IP in the developing third quarter is falling on a quarter-to-date basis, logging an annual rate decline at an 8% pace.

Industrial production fell in Japan for the third consecutive month. While the July drop was small, the three-month growth rate shows a sizeable decline in the works. IP in the developing third quarter is falling on a quarter-to-date basis, logging an annual rate decline at an 8% pace.

Still, the supporting trends for IP are confusing. While output is dropping sharply over three months and logs weak growth over 12 months, output speeds up over six months. And this is true among all product groups. In short, that is no real intra-yearly progression in place although current data are quite weak.

Despite the recent weakness, the month's drop in output is the most limited drop of the last three months. That does not make it look as though a new round of weakness is kicking in.

Certainly, there are concerns and there should be sensitivity to the potential for the trade environment to impact the economy. The U.S. is taking aim at China and China is Japan's most important trading partner. But this does not look like the accumulating weakness from trade war exported to Japan. And the trade war really has not started yet, but it is possible through planning that adverse effects could precede actual tariff warfare although usually we expect the opposite of output and trade flows, to ramp up ahead of tariff imposition to try to get merchandise in place before trade restrictions kick in. There is no evidence of that in Japan.

However, viewed more broadly in the chart, all the growth rates show some tendency to decelerate. The trend is clearest for 12-month growth as the other rates of change are so volatile. Japan has a longer term slowing in progress.

Japan's PMIs have been eroding and logging very low readings showing output barely expanding. Living on the edge is not a reliable way to keep growth going. Of course, the Bank of Japan has been stepping on the accelerator, but that does not seem to have had any more impact on growth than it has had on inflation.

Asia generally has been lagging the expansion in the West. Japan shows the upshot of that in its lethargic pattern of growth. It is perhaps one of the least talked about aspects of the Western central banks having decided to raise rates and move on. What happens to export dependent Asia? Asia services its growth typically through the export channel. If the U.S., Europe and the U.K. slow, will there be enough demand left over for Asia? And if the U.S. slaps a 25% tariff on a large portion of China's exports, how much will that cool demand? This another side-effect of China's decision to delay the development of its services sector and to drag its feet on stimulating domestic demand. Xi's 'Belt and Road' program 'of the future' is no such thing. It is a program of the past. It is just a way to grease the skids to let China's exports fly. The rest of the world is already saturated with China's exports. China really needs to move on to plan B and to develop markets at home. And that is not what the Belt and Road project does. But China has put all its egg foo young in that basket and that will put it at risk to slower growth in the West. And with China as Japan's main trade partner, Japan may find that it has hitched its wagon to a falling star.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief