Global| Dec 13 2013

Global| Dec 13 2013Japan's IP Advances in October

Summary

Japan's industrial output rose by 1% in October, beating expectations. Output in Japan cratered in early 2012; it has been gradually advancing since then. The year-over-year growth rate of 5.3% is the highest since May 2012. Japan has [...]

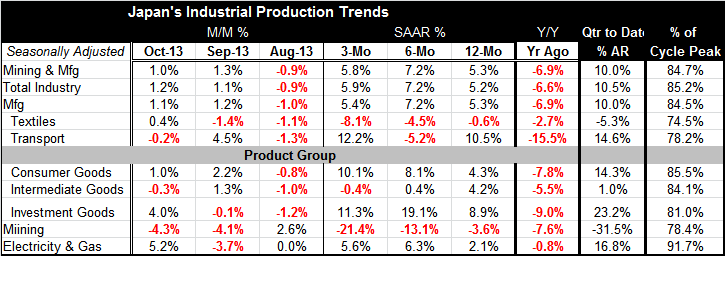

Japan's industrial output rose by 1% in October, beating expectations. Output in Japan cratered in early 2012; it has been gradually advancing since then. The year-over-year growth rate of 5.3% is the highest since May 2012.

Japan's industrial output rose by 1% in October, beating expectations. Output in Japan cratered in early 2012; it has been gradually advancing since then. The year-over-year growth rate of 5.3% is the highest since May 2012.

Japan has still not had a full recovery from the financial crisis as it has been hit by the Tsunami and is still dealing with problems at its decommissioned nuclear facility in Fukushima. Japan's manufacturing is still better than 15% short of its pre-recession peak.

Transportation has the strongest growth rate over the past 12-months on a gain of 10.5%. But that is still part of lagging recovery. The transportation sector's output level is still some 22% below its past cycle peak.

Output for consumer goods and intermediate goods is expanding at a pace between 4% and 4.5%. Utilities output of gas and electricity is weaker, rising by just 2.1% over 12-months. The output of investment goods is up at a very strong 8.9% year-over-year.

Momentum paints a slightly brighter picture. Output is undergoing steady acceleration for consumer goods. Investment goods and electric and gas output show much stronger growth rates over 3-months and 6-mopnths compared to 12-months. Intermediate goods, however, show a steady deceleration in growth from 12-months to 3-months; over 3-months output is declining in this sector. Mining also shows deceleration with a negative growth rate of 21.4% at an annual rate over the last three months.

On balance Japan's situation is improving- it still has a long way to go. Growth rates in output are solid and over the last 12 months and on shorter horizons. Over the last two months, total industry and manufacturing have had positive and strong monthly rates of growth. Japan continues to make progress. With the improvement in the global environment, this improving trend should continue.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief