Global| Aug 24 2018

Global| Aug 24 2018Japan's Inflation Trends Diverge

Summary

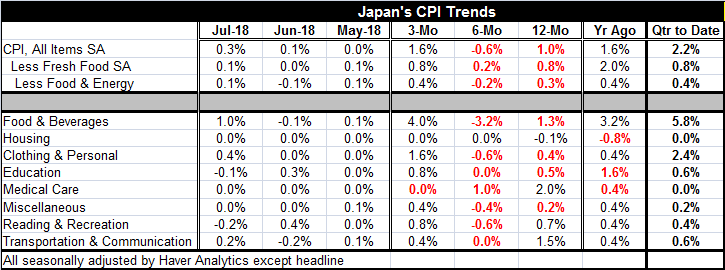

In July, Japan's headline inflation was up by a strong 0.3% but balanced by a 0.1% gain in the CPI excluding food and energy (core). The headline gain followed a weak 0.1% June rise while the core gain followed an even weaker 0.1% [...]

In July, Japan's headline inflation was up by a strong 0.3% but balanced by a 0.1% gain in the CPI excluding food and energy (core). The headline gain followed a weak 0.1% June rise while the core gain followed an even weaker 0.1% June decline.

In July, Japan's headline inflation was up by a strong 0.3% but balanced by a 0.1% gain in the CPI excluding food and energy (core). The headline gain followed a weak 0.1% June rise while the core gain followed an even weaker 0.1% June decline.

The chart demonstrates the year-on-year trends for the headline and for the core. The headline is showing signs of accelerating while the core trend is failing again.

The chart aptly demonstrates the fake rise of inflation in 2014 when the imposition of the VAT tax boosted the measured inflation rate for 12 months then disappeared from sight as year-over-year inflation settled back to its weak and declining ways.

The three-month inflation rate for the headline is showing some push again as it is up to a 1.6% pace the same annual pace it had over 12 months, back 12 months ago. The 1.6% gain represents an acceleration from its six-month pace of -0.6% and reverses a deceleration that had been brewing as the six-month pace is below the 12-month pace.

The sequential growth rates for core inflation are noncommittal with the same 12-month to six-month deceleration and with the three-month pace picking up relative to the six-month pace. But the overriding story of core inflation is that the variations in inflation are small and that inflation has remained low.

Over 12 months Inflation slowed compared to its pace over 12 months of one year ago; that slowing is present for headline and core inflation as well as for four of eight components. The over six-month inflation slowed again compared to its 12-month pace. That slowdown holds for the headline and core and for seven of eight components. So it is not very surprising to find that over three months inflation is rising compared to six months or even that the three-month pace generally outstrips the 12-month pace. Inflation in Japan has gone through a broad period of slowdown. And now while that is reversing to some extent, it is not reversing with any vigor.

Despite its rebound, the three-month headline CPI pace is only at 1.6% and the three-month core pace is only at 0.4%. Japan continues to be dogged by weak inflation trends like so many other countries.

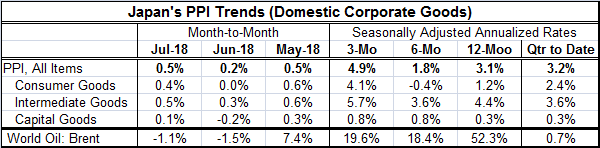

Not surprisingly, PPI inflation is led by intermediate goods gains as oil prices have flared. Consumer goods prices have also been boosted. But capital goods prices have a very low energy input into them and capital goods prices are consistent and steady in their mild rate of expansion at a pace below 1% on all sequential horizons as well as for the quarter-to-date.

With this shift in policy, there is very little guidance as to what the BOJ will do regarding its ongoing inflation undershooting. Clearly, the Bank of Japan, like the Fed, BOE and ECB, is taking steps to end or planning to take steps to end the ultra-easy policy period and is doing so without providing clarity about its inflation target. Moreover, less accommodation does not help the economy achieve a higher rate of inflation. But if the BOJ has decided that forces beyond its control are responsible for keeping inflation low, it may be deciding that ultra-accommodative polices are too dangerous and distortive to the economy to continue and not effective in lifting inflation. It may still feel that it wants to encourage 2% inflation, but that it is not in a position to make that happen. If this is a correct interpretation, the risk here is to Japan's credibility as it will be keeping an objective of 2% on the books but will continue to miss that objective and run the risk of losing market confidence. The BOJ will probably need to make some policy statement about that, separating the short-term inflation outcome from its long-term goal.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief