Global| Oct 15 2015

Global| Oct 15 2015Japan's Indices Wander in Different Directions

Summary

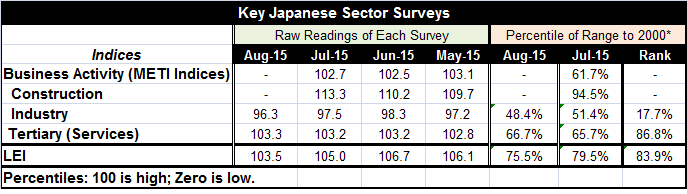

Japan's tertiary index (services sector) in August edged only slightly higher. The industry index has fallen to 96.3 from 97.5. And the industrial production index for August fell by 1.2%, more than the initial estimate of -0.5%. [...]

Japan's tertiary index (services sector) in August edged only slightly higher. The industry index has fallen to 96.3 from 97.5. And the industrial production index for August fell by 1.2%, more than the initial estimate of -0.5%. Japan's economic pulse continues to weaken.

Japan's tertiary index (services sector) in August edged only slightly higher. The industry index has fallen to 96.3 from 97.5. And the industrial production index for August fell by 1.2%, more than the initial estimate of -0.5%. Japan's economic pulse continues to weaken.

Japan's gauges continue to show economic stumbling. We can position its indices in their range in July, the month for which we have the most recent data for all the indices. There we see construction as the strongest sector and services as the next strongest but far back in its range compared to construction. The weakest is the industry index as Japan is having a hard time boosting exports in this weak global environment.

The overall business activity index stands in its 61.7 percentile, a very moderate reading. Meanwhile, Japan's LEI sits in its 70th percentile in July, slightly stronger than the METI headline index.

In the most recent month, we have observations for industry and services. Industry is sitting in the middle of its high-low data range but stands in the in the lower 17th percentile of its rank when re-ranked in its historic queue of data. Japan's industrial sector has been weaker only 17% of the time. Conversely measured as a rank standing, the services sector looms stronger with an 86th percentile range standing compared to its 65.7 percentile standing in its high-to-low range.

The chart bears out these rankings. There we see a sharp drop in services in late 2013 with a slow and deliberate rise from that sunken trough. The tertiary sector is dominated by a slow trend movement except for that ratchet lower in 2013. Industry shows a lot more variability, but it is in the aftermath of its second failed recovery since later 2012. The industrial sector index continues to fade as the global climate remains harsh despite the fall to a more competitive level by the yen.

The construction sector is on its second boom since its trough in later 2011. However, it is a small sector and will not carry the economy.

The recent economic news globally has been disappointing. Markets are starting to give up on the notion of a Fed rate hike this year as the WSJ reports that the Fed itself is losing confidence on that score. In Europe, Ewald Nowotny, the Austrian board member at the ECB, has said that the ECB needs to do more to hit its inflation target. U.S. manufacturing reports from the NY region and Philadelphia region in September were still showing declining activity. Japan is not alone registering economic disappointment. And as we see in the ECB, what is starting to develop is a frustration the more should be done. It is not simply that the economies are underperforming yet again. But there is more of a sense, this time around, that something must be done.

Both the ECB and the BOJ have held back on expanding their respective programs of stimulus. In the U.S., the Fed seems to be backing away from its intention to hike rates in 2015. Disappointment is a global phenomenon. So is the lack of any new action. Meanwhile, backsliding is the same old, same old phenomena.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief