Global| May 09 2019

Global| May 09 2019Japan's Consumer Confidence and the 'New Normal'

Summary

The chart mixes quarterly frequency data (dots) with monthly data (line) Japan's consumer confidence ticked down to 40.4 in April from 40.5 in March. In doing so, the index reached a point weaker than what it has seen over three [...]

The chart mixes quarterly frequency data (dots) with monthly data (line)

The chart mixes quarterly frequency data (dots) with monthly data (line)

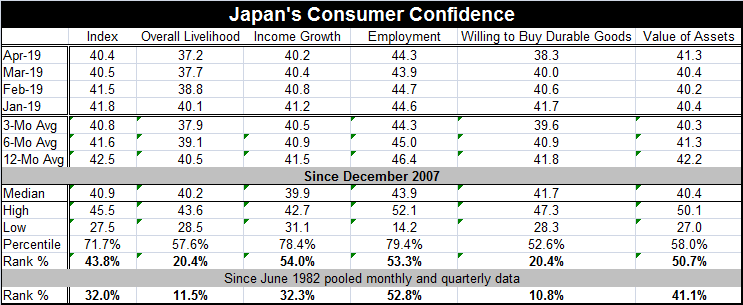

Japan's consumer confidence ticked down to 40.4 in April from 40.5 in March. In doing so, the index reached a point weaker than what it has seen over three years. Confidence fell by one diffusion point in March to 40.5 from 41.5 in February. That was the bigger step down. But a slow erosion continues. The message from the April decline in confidence is that the drop in March was not a fluke.

The consumer confidence measure for Japan is a diffusion index constructed so that 50 is a neutral reading. At 40.4 the headline is below 50 as are all of its component readings as of April.

However, Japan has been in under protracted dislocation since the Great Recession as watershed demographic events, (a shrinking population) an earthquake/Tsunami and a nuclear disaster, have buffeted the economy. At the same time, Japan is highly dependent on trade and it trades most with China and second most with the United States. The recent U.S.-China trade war has also adversely affected Japan. Since it trades so much with China, the China slowdown has had an impact. The U.S. and Japan have not yet begun their bilateral negotiations, but they are 'in the works' as well. Japan also has skin in the game over North Korea and has had some on again off again run-ins with China over a string of disputed islands.

Against this background, it is not surprising that Japan's confidence gauges remain depressed (below neutral). To see them in a different perspective, I also rank the index and its components on a timeline since December 2007. The raw diffusion gauge has confidence at the 40.4 mark below its neutral value of 50. But the ranking of that value is in its 43rd percentile. On the face of it, these two metrics (which measure different things) seem very similar. However, if we were to put confidence at a neutral value of 50, the rank percentile for that would shoot all the way to its 99th percentile. Confidence has not been at or above neutral since February 2006. Confidence is both currently and structurally weak.

We see that such is the case for other components as well. For example, the measure of overall livelihood is at its 37.2 diffusion value with a diffusion value ranking of 20.4%. The livelihood gauge is well below neutral and it has been weaker (since December 2007) only 20.4% of the time. In fact, to take this further, the table shows the median values for each component since December 2007. All of the medians are well below 50. The median observation since December 2007 has been a measure reflecting conditions worse than neutrality for each component. To generalize, the medians for the headline reading and for components are close to the '40' diffusion mark, some 10 diffusion points below neutral. Only 'Income,' 'Employment' and Value of Assets' are above their medians since December 2007.

Since 2007, Japan has been depressed. And now the rank standings tell us that Japan is relatively more depressed than it has been on average since end-2007. The willingness to buy and the overall livelihood measures show the most distress. In fact, since late-2007, there have been only two observations of 50 or higher. For Japan, neutral is about 'as good as it gets.'

This parsing of Japanese confidence explains a great deal about how Japan's economy is operating. There is an aging population. Fertility rates are down because it is such a high cost country some couples have decided to forego having families. Competitive pressures remain intense. Eighty-nine of the one hundred and thirty-six observations since December 2017 lie in the diffusion range of 40.0 to 49.9. Another thirty observations lie between 35.0 and 39.9. That is 87% of the entire distribution. Japanese consumer confidence metrics are stuck in a diffusion reading of 30 to 44.9. All of these reflect subpar results. And interestingly, Japanese values or psyche have not changed to call these readings what they really have become which is 'normal.'

In the U.S. in the past recession period, an expression has arisen called the 'new normal.' It is unclear what that means even in the U.S. But it is an acknowledgement that in the wake of the Great Recession, things have changed. It seems to be marked by a lower rate of unemployment and lower inflation as well as by lower equilibrium interest rates. In the U.S., it also has come with a relatively solid economy. In Japan, the new normal seems quite different. If we measure new normal as the medians on the consumer sentiment index and components for the last four years, we do not get a result that is much different from the medians for the full period back to end-2007. The biggest shift is a median that is 5% higher for 'value of assets' (42.5 instead of 40.4). The fact that the last four year median and the last 11 year median are nearly identical underscores that Japan has moved into a new steady-state environment. Over the last 4 years, Japan's GDP has averaged growing only 1.2% per year. Domestic demand has grown by only about 1% per year. Exports have outpaced imports averaging growth of 2.8% per year compared to 1.8% per year for imports. However, Japan continues to make capital equipment investment which has averaged growth of 2.5% per year. All of this has translated into an average annual gain in GDP per capita of 1.3%.

Japan is not doing badly. But Japan is not doing well. It is hard to tell how consumers are going to assess the future and what that will mean. It does not seem likely that Japan is going to grow a lot faster and yet Japanese consumers render confidence measures that are well below their neutral readings for a long span of time. What will cause these responses to change? How long can a people go expressing their steady state confidence situation as something that is inferior year in and year out? At some point doesn't reality have to set and don't people have to accept actual persistent conditions as the new normal? Or do they?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief