Global| Mar 12 2018

Global| Mar 12 2018Japan's Cabinet Office Survey

Summary

Japan's Cabinet Office survey backtracked in Q1 2018 with the business conditions index for large firms overall falling back to 3.3 in Q1 from 6.2 in Q4. The bellwether large manufacturing firm index fell to 2.9 from 9.7. This survey [...]

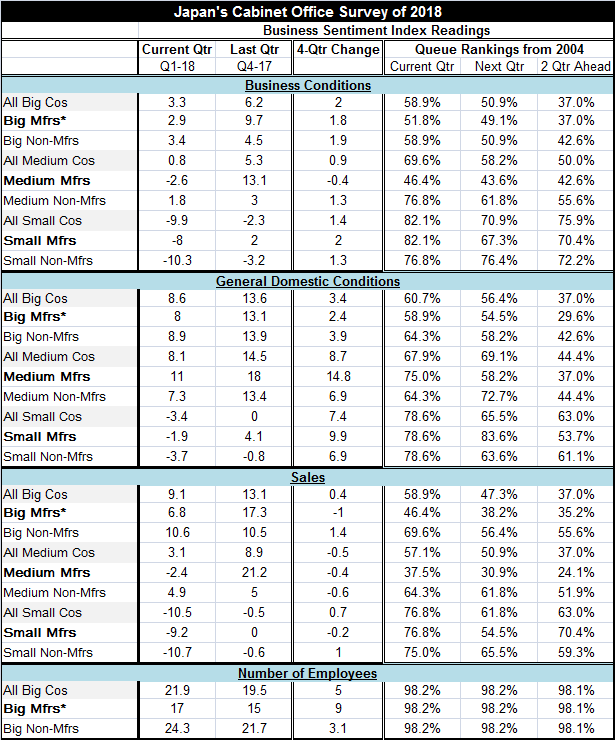

Japan's Cabinet Office survey backtracked in Q1 2018 with the business conditions index for large firms overall falling back to 3.3 in Q1 from 6.2 in Q4. The bellwether large manufacturing firm index fell to 2.9 from 9.7.

Japan's Cabinet Office survey backtracked in Q1 2018 with the business conditions index for large firms overall falling back to 3.3 in Q1 from 6.2 in Q4. The bellwether large manufacturing firm index fell to 2.9 from 9.7.

This survey assesses large-, medium- and small-sized firms separately. It provides readings on business conditions, general domestic conditions, sales and the number of employees. It is a very comprehensive report. The table below provides all those metrics except I have only presented the employment offerings of large companies since all of them simply have extremely high rank standings. Japan, like the U.S., is seeing employment growth and labor market tightness. In Japan's case, it is more of supply side constraint at work as its population is shrinking.

The table shows the two most current quarters' values, the 4-quarter change and then a ranking of the current quarter, the next quarter and the two quarter-ahead readings. For all readings, except the employment module, the percentile standings of the readings decay as the survey moves farther into the future.

For business conditions, as we note above, the overall index fell month-to-month, but it is up by two points over the last four quarters. The current business conditions index has a 58.9 percentile queue standing, but for one quarter ahead that standing falls to 50.9 percentile and for two quarters ahead it falls again to the 37th percentile. In each case these responses are ranked against similar one or two quarter ahead responses over their respective histories. The weaker outlook is real not a function of something being more distant and less certain since we rank each response against the historic series of expectations responses. What we see is that Japanese firms are losing confidence about growth on the future. Despite the gain over four quarters, there is a quarter-to-quarter step back and the progression seems to be about the same for manufacturing as well as for nonmanufacturing large firms. Medium sized firms experience less of a setback in their expectations and small firms have a bit less of step back and much higher readings compared to history all around.

The percentile standings for business conditions, general domestic conditions and sales are quite similar for large firms on all three of these metrics. However, the gains on sales are more erratic across the various size classes of firms and are smaller for large firms per se. Medium sized companies of all sectors and all manufacturers regardless of size are experiencing some loss in sales over four quarters.

Japan may be in for political uncertainty as well as some old charges are being raised again against Mr. Abe. And while the Bank of Japan is resolute in its stimulus, it has joined the ranks of central banks talking about an end game for stimulus by putting its likely end game in fiscal 2019.

The recent U.S. jobs report brought a message of more of the same as job growth was once again strong with wage gains continuing to be suppressed. It is hard to know what the Fed will do with that and where the Federal Reserve is in its tightening cycle; yet, that is important for everyone to know. Globally, inflation continues to be under wraps, but central banks clearly are nervous about what's next. Japan is the one country that is a little different in that regard as inflation in Japan is still being leveraged higher and no one is afraid of Japan's inflation overshooting.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief