Global| Jan 13 2015

Global| Jan 13 2015Italy Shows Solid IP Gain in November but Weakness Lingers

Summary

The euro area seemed to show some signs of improved life in November. Italy, reporting its IP later than most EMU members, has joined the party. Still, Italian production trends remain weak. The chart shows year-over-year trends for [...]

The euro area seemed to show some signs of improved life in November. Italy, reporting its IP later than most EMU members, has joined the party. Still, Italian production trends remain weak.

The euro area seemed to show some signs of improved life in November. Italy, reporting its IP later than most EMU members, has joined the party. Still, Italian production trends remain weak.

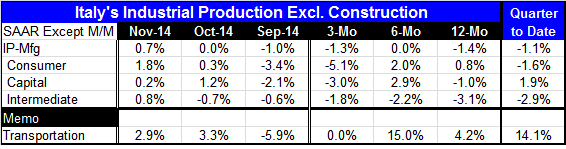

The chart shows year-over-year trends for the three main industrial sectors: consumer goods, capital goods, and intermediate goods. Intermediate goods output traces the steadiest decline while capital goods output seems to have settled into a steady state slow decline and consumer goods output remains volatile in a principally declining trend.

Over shorter horizons, from 12 months and in, IP sequential growth rate are mostly negative. Consumer goods trends show a rise over 12 months and six months but with a relatively sharp drop over three months. Capital goods show a decline over 12 months with a stronger pace of decline over three months and a growth rate of nearly 3% sandwiched in-between over six months. Intermediate goods show declines on all horizons but the pace of these declines is diminishing over more recent periods. In contrast, production of the transportation sector has 4% growth over 12 months with a 15% pace over six months and a pace of zero over three months.

In the quarter to date, output is declining in all three major sectors but this is with two of three months in play. This calculation is based on growth in October and November over the Q3 base (average Q3 IP). As you can see, most of the growth rates for the three sectors over this two month period are positive (intermediate goods in October is the exception). The negative growth rate for Q4 is right now not a function of declining growth rates in Q4 but because of a sharp decline at the end of Q3 from which Q4 output has not sufficiently recovered. That could change with the December IP report.

The picture we get for Italian output shows that Q3 was very weak, not that Q4 is so terribly weak. Of course, the manufacturing PMI data for Italy do not give us a reason for much hope to change that. The November manufacturing PMI was below 50 and it is farther below 50 in December. Italy's industrial sector is still weak. The measured weakness is not due to a technicality. It's reality. But the weakness is not progressive; it is more lingering. And this is the situation for most of Europe. Weakness is lingering more than cumulating. Still, the global environment is poor and the sanctions on Russia are still in play as is the lingering geopolitical risk. The main positive forces that could boost the EMU - and Italy - are three: (1) the weakening euro exchange rate that boosts competitiveness of all EMU members vs. countries outside the single exchange rate area, (2) the drop in oil prices which will help most of Europe's consumers, and (3) the action expected from the European Central Bank.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief