Global| May 29 2019

Global| May 29 2019Italy: In a Pickle of Its Own Making? Or Marinated in the Brine from the Rhine?

Summary

Since 2013, Italian inflation has consistently been lower than German inflation The table and chart chronicle some interesting circumstances for Italy. The chart shows that (as they say) ‘believe it or not!' Italian inflation has [...]

Since 2013, Italian inflation has consistently been lower than German inflation

Since 2013, Italian inflation has consistently been lower than German inflation

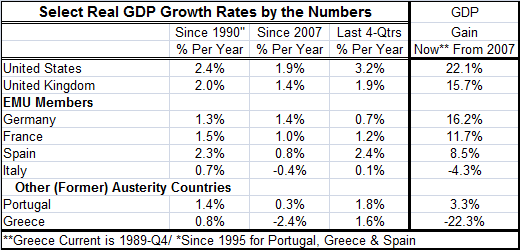

The table and chart chronicle some interesting circumstances for Italy. The chart shows that (as they say) ‘believe it or not!' Italian inflation has persistently been below German inflation since 2013. However, Italy's consumer confidence is in its 81.6 percentile with business confidence much weaker in its 42nd percentile - both ranked on data back to 1995. Italian austerity has been highly successful in both reducing inflation and in keeping inflation's trend growth tame. It has done this without destroying confidence since consumer confidence is still quite robust. But business confidence stands at its 42nd percentile, below its historic median. And Table “Select Real GDP Growth Rates by the Numbers” compares GDP growth across several ‘original' EU/EMU economies. It shows the cost of Italy being stewed in the Rhine brine to remove its inflationary ways was and is steep.

The split between the standing for consumer and business confidence may tell us something too. It may be that Italy still is a bit thick with social welfare programs allowing people to be comfortable (81.6% ranking for confidence) even when economic times (42% confidence for businesses) aren't very good.

From 2007 Germany has grown real GDP by 16.2% while Italy's GDP has shrunk by 4.3%. Italy has achieved a solid measure of success on the inflation front, but all this austerity took a huge toll on growth and has brought to power two parties in a coalition with an anti-EU slant, the Northern League and the Five Star Movement. With Deputy Prime Minister Matteo Salvini pushing the EU for more flexibility, things will be coming to a head in Italy.

As I had warned at the time, austerity was imposed this whole process started with something called the ‘internal devaluation' because no one wanted to called it a policy of deflation and recession. But that's what it was. That approach had a near-impossible goal. The pain and suffering required to put Italian inflation back in the bottle was going to be too great to pass the political test of time even if Italy could get the economics to work, or so I argued. In the end, Italy got the economics to work and it has been at the cost of Italian politics and growth. Now we are seeing the result of pressing so hard to impose the rules favored by Germany and other hard money countries on a country where that mindset for low inflation has not been strong. If this is success, I really fear failure.

The rubber is hitting the road again in the EU. No sooner are the EU elections done than the EU ‘Love Letters' have been sent out. No point sending them out before people vote and making them angrier, eh? But now it is done. The EU is putting on notice those in violation of the mass-trick (also known as ‘Maastricht') agreement. With opposition parties making some gains in the EU elections but with the traditional pro-EU parties garnering enough votes to hold on, there may be some differences in the way the EU is governed but there will not be a tectonic shift. And the sending out of those letters is a reminder that there are debt and deficit standards to be met in EU and they will be enforced. This is a stark and harsh rebuke to Italy's Norther League-Five Star coalition and to Deputy Prime Minister Salvini who had called on the ECB to guarantee the debts of all EMU members. Of course, that was not going to happen. Instead, Italy risks new sanctions and fines from the EU for being out of compliance with budget rules. Italy was sent a letter asking it to report on its fiscal condition and is required to reply by Friday.

Letters also have been sent to France, Belgium and Cyprus. Each case is treated separately depending on the countries' individual circumstances.

EU unity began breaking apart over the broadening of social policy rules and a centralized and imposed position on dealing with migrants made by powerful land-insulated members who drew lines that placed the water boundary countries in a position where the full burden of absorbing and caring for migrants (until such time as they were accepted to entry into the union) fell on those water boundary countries which has meant Greece and Italy. Only recently has Italy become militant and refused to take migrants rescued at sea, forcing them to be shipped to Malta or France.

But the complaints are not just about migrant or other intrusions. They are about economics and growth. Italy was successful on the inflation front only by hammering growth to a pulp. And it can't be very surprising that Italian debt appears excessive relative to GDP after all this austerity which was the tool of inflation reduction. GDP in Italy has declined in real terms, compared to its level in 2007.

Italy, after being water-boarded with German Kool Aid, finds itself with a more aggressive population backing a government that is aggressively bucking EU rules and doing so with a solid economic argument. This argument is made more realistic since in 2002 both Germany and France were in violation of budget rules and they refused to be sanctioned (see der Spiegel on this here). After a banking crisis in Cyprus where the ECB did not want to bail out banks since it was thought there was a lot of hot ‘illegal' money in those banks, EU rules were changed to prohibit bail outs. Now bail-ins are the law. But both France and Germany bailed out their banks ahead of the Greek crisis so Greece could not use bank exposure of their private sectors as leverage. And today Italy still has a banking problem and with bail outs prohibited there is no way Italy is going to be able to fix it.

And Italy's growth has been consistently lower than just about everyone's—except Greece

EU rule-making has followed the golden rule: he who owns the gold makes the rules. Italy has been struggling with debt and that struggle was made worse by its fight to reduce inflation. Surely the EU Commission can see how unfair it would be to hold Italy's feet to the fire over excess debt after what the EU's austerity ‘medicine' did to it?

I say this as a matter of reasonableness although I don't for one minute expect one scrap of forbearance from the EU. The EU respects rules and power and Italy right now has no power and is in violation of the rules. It has come up against this hard stop without getting the new order it sought in the recent EU elections. Italy will now deal with the same old lame duck EU bureaucrats with little hope of any broader view of its circumstance.

In this you can see the great flaw of the EMU. And here is a clear lesson about not letting your inflation rate get out of hand because the medicine to bring a country back into line is draconian with perhaps life-threatening side effects (if ‘you' are government, it certainly is regime-threatening). Italy now faces an even worse situation that what it has endured over the last decade. And it remains on the front lines absorbing the ‘EU's' migrants.

I make these arguments not because Italy is pure and chaste. It is not. And it was certainly among that group of countries that wanted the EMU to get at lower loan rates. And it did abuse borrowing at low rates. And Italy also has been a chronic inflation country. Germany's tact of running a national inflation rate below the mandated EMU-wide 2% put countries like Italy at an even more extreme competitive disadvantage. And eventually all the Mediterranean countries came up against the fiscal constraints of the EU, the very constraints that had been placed there to catch them but that had first caught Germany and France to no effect. Is it still a ‘catch and release program or not?'

At this point in its evolution with the EU saying goodbye to a major member, it would be a good time to ask if, since there is no fiscal arrangement in the EMU or EU, could members be permitted some flexibility relative to the community's budget rules? History shows that it has been lenient in the past. And while leniency may not promote compliance, Italy certainly has been through the wringer on austerity and one with a massive impact on its economy. If Italy cannot be eligible for some measure of leniency, who ever could? And why would Europe be willing to subjugate Italy to such pain to hit a debt ratio that was arbitrarily and not carefully chosen at all? Why ‘stick it to Italy' at 60% instead of with debt at 70% of GDP or 75% of GDP? What is the research behind this arbitrary rule that the EU allowed large powerful members to flaunt in the past? It is indeed a good time for the old EU/EMU ruling elite to ask themselves what is fair. The high inflation countries signed on for the EMU and have played by the rules as best they could; several have hard-landed and have suffered. Italy has even conquered inflation. But what is next for it? How will other members look at the treatment of Italy after all it has been through? Does the EU Commission even care or will it take another round of voting before the message sinks in? Is the EU going to be a community for the betterment of its members or a prison where powerless violators are subjected to economic tortures that prolong their punishment so they can ‘serve' the needs of the wealthier members? That is as good a way to frame the dilemma as any.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief