Global| Dec 11 2017

Global| Dec 11 2017Italian Retail Sales Fall Sharply -Continuing Pattern of Weak Retail Readings in EMU

Summary

Italy's retail sales fell by 1% in October with declines in food and clothing & furniture as well as a sharp pull-back in real retail sales. Italian retail sales show a lot of red ink, indicating sales declines for all categories over [...]

Italy's retail sales fell by 1% in October with declines in food and clothing & furniture as well as a sharp pull-back in real retail sales. Italian retail sales show a lot of red ink, indicating sales declines for all categories over all horizons from 12-month to six-months to three-months. Real retail sales in Italy also are falling on all horizons and their 2.7% pace of decline over three months exceeds the year-on-year drop of 1.8%.

Italy's retail sales fell by 1% in October with declines in food and clothing & furniture as well as a sharp pull-back in real retail sales. Italian retail sales show a lot of red ink, indicating sales declines for all categories over all horizons from 12-month to six-months to three-months. Real retail sales in Italy also are falling on all horizons and their 2.7% pace of decline over three months exceeds the year-on-year drop of 1.8%.

Retail sales and consumer confidence follow the same rough contours over time. Currently, Italian confidence has been on an upswing that has peaked and only started to erode for that recent local peaking. Retail sales also are a volatile series. While retail sales and confidence do follow the same broad paths, retail sales are exceptionally volatile. The steepness of the drop in October does not necessarily carry a message. We really won't know the economic context for this drop until we see how much of this drop will be offset in the following month. But there is no denying that October's drop is part of a yearlong pattern of weak and slipping retail sales in Italy.

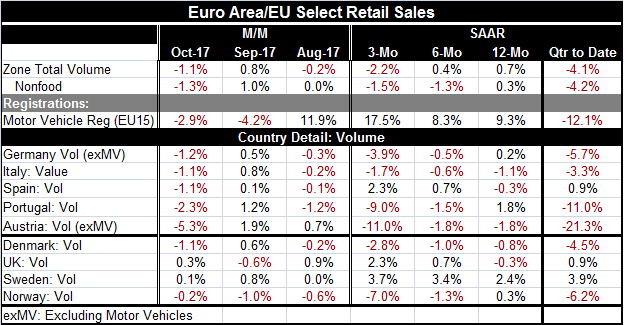

There also is a wide variety of retail sales data available for much of the EMU as well as for the EMU as a whole. EMU sales volumes are weak; they are falling by 1.1% in October and falling at a -2.2% annual rate pace over three months but are up at growth rates under 1% over 12 months and six months. Motor vehicle trends are complicated with registrations falling sharply in two consecutive months but are still expanding briskly over three months on balance with strong momentum for one year and six months as well.

Across the EMU as well we have numbers of the original EMU countries and other European venues where sales are lower month-to-month. Of the five EMU countries, whose data are presented in the table, three have declines over 12 months Germany has real sales up by just 0.2% over 12 months while Portugal with a again of 1.8% has the strongest year-on-year sales in this group. Quarter-to-date sales are weak and largely declining.

Despite building momentum in the PMI data from Markit, retail sales have continued to show a much more lethargic picture than the PMI data. With the release of Italian sales today, I am recapping again the EMU-wide retail sales weakness. Output data continue to be relatively upbeat while consumer activity shows much less ebullience and a good deal of outright weakness. We look for this dichotomy to be resolved in the coming months. In the meantime, it is also true that consumer confidence appears to be still relatively buoyant. But the failure of consumers to engage remains an ongoing worrisome aspect of the ongoing recovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief