Global| Sep 11 2017

Global| Sep 11 2017Italian IP Makes Strong Ongoing Gains in July As PMI Warns of a Slowing

Summary

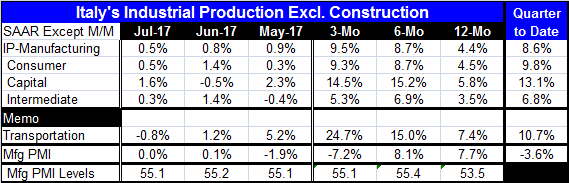

Italy's industrial production gained 0.5% in July after a 0.8% increase in June. It also advanced 0.9% in May. IP has advanced strongly for three straight months as well as in five of the last six months. Growth rates by sector are [...]

Italy's industrial production gained 0.5% in July after a 0.8% increase in June. It also advanced 0.9% in May. IP has advanced strongly for three straight months as well as in five of the last six months.

Italy's industrial production gained 0.5% in July after a 0.8% increase in June. It also advanced 0.9% in May. IP has advanced strongly for three straight months as well as in five of the last six months.

Growth rates by sector are gaining momentum. The strength is not just an artifact of the headline rising on one sector. All three main manufacturing sectors show three- and six-month growth substantially stronger than their respective year-on-year rates of growth.

Italy's manufacturing PMI echoes the strength in the manufacturing production series. Ranking the manufacturing PMI index back to January 2012, the index stands at the 70th percentile in this historic queue of data, a relatively firm reading.

In the evolving quarter-to-date, manufacturing IP is up at an 8.6% annualized rate, supported by stronger quarter-to-date gains in the consumer sector and in capital goods with intermediate goods up at a 6.8% annual rate. This is very broad based strength that demonstrates that the recent surge is ongoing and smooth as it provides growth at a pace very similar to the three-month growth rates.

Similarly, the transportation sector is strong despite a drop in output in July. Transportation output is still up at a 24% annualized rate over three months and accelerates strongly from 12-month to six-month to three-month while demonstrating a double-digit growth rate in the quarter-to-date.

Prevarication from the PMI

The Markit manufacturing PMI for Italy shows steady and firm recent readings around the 55 mark for raw diffusion. The average of the manufacturing PMI moved up strongly from 12-month to six-month, but over the last three months the index has backtracked slightly. The PMI hints that Italy's run of strength and acceleration may have run its course as the manufacturing PMI is a tick lower in July and more substantially lower in May compared to April. The July level is falling at a 3.6% annual rate comparted to its Q2 level. However, the PMI data also are available for August and in August the PMI has accelerated again. Still, with the PMI vacillating, it's a good idea to retain some skepticism about trend.

Data dissonance

These data create a bit of dissonance between the production data and Italy's diffusion reading. IP is still advancing and accelerating while the diffusion gauge is beginning to back off even as it jumps back 'into gear' in August. PMI gauges are sensitive and often are the first places where we see changes in momentum. Separately, the pace of the gain for Italy's IP is simply unsustainable and basically apart from the experience of growth in much of the rest of EMU at this time. Looking ahead, the euro is rising and that should create some negative feedback that will impact Italian manufacturers.

Outlook

While the production data on their own are very strong and seemingly bullet-proof, the PMI offers some palpable warnings as it slows and begins to gyrate even if it does so at a high level. I would take the PMI warnings to heart and look for this spurt in Italian IP growth to lose steam and to settle down. Beyond that, it is too soon to tell how much slowing there may be. The PMI gauge is only pointing to some slowing as the gauge itself remains at a relatively firm reading and then reignites in August. However, there is nothing in either of these reports to slow down the ECB. Italy appears to show enough strength and good enough prospects that if other EMU members were to show similar strength would allow the ECB to feel confident that it could begin to dismantle some of its current stimulus architecture.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief