Global| Mar 26 2010

Global| Mar 26 2010Italian Households Take Another Step Back In Comfort Italian Consumer Confidence Turns The Corner, The Wrong Corner

Summary

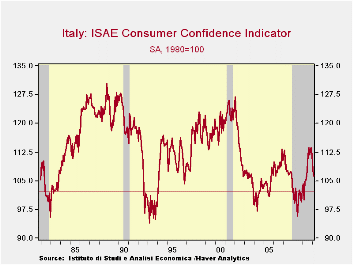

Italian consumers used to feel better. They used to feel a lot better just a few short months ago. In December of 2009 at a level of 113.6 Italy’s consumer confidence measure compiled by ISAE hit what is for now its cycle high. That [...]

Italian consumers used to feel better. They used to feel a lot better just a few short months ago. In December of 2009 at a level of 113.6 Italy’s consumer confidence measure compiled by ISAE hit what is for now its cycle high. That reading had barely surpassed the December 2006 confidence peak-reading of 113.4. But December 2009 stood as the best reading since July 2002 and all seemed good. In retrospect, Italy’s funk goes back to that late 2000 transitional period when confidence dropped from very strong levels to begin its period of what has been readings that have persisted at much lower levels. For Italy it’s problems are not just the financial crisis and economic recovery.

Now it is clear that the bloom is off the consumer’s rose. That rose seemed to bloom early and with all of Italy’s troubles it was hard to tell what the real truth was. The truth appears to be that Italy’s consumers were overly optimistic or actually in denial. Their spirits are now deflating fast.

Italian consumers rate the past twelve months as better in March than they did in February. But that was only a 61st percentile of the range response. In March, looking to the more important next 12-months, the overall rating remains what is was in February but that is a lower 34th percentile of range response. In other words the level of the reading is nearly in the lower one-third of its range. Expectations of unemployment are up and that reading is in the top 2% of its range. Unemployment fears have really ratcheted up in Italy. It’s possible that events in fellow Mediterranean country Greece are having some chilling knock-on effects.

Despite these responses consumers rate their household finances as one point improved over the next 12-months compared to last month’s outlook reading; it’s a 36 range percentile assessment. Households also rate current savings as high, in the top 7% of their range, but future savings are rated in the bottom 25th percentile of their range. But where the rubber hits the road and the spending environment is assessed Italian consumers place the assessment right in the middle at the 54th percentile of the range. Good time to spend? Mezzo-mezzo.

There is a lot of confusion in Italy about where the country is going and how fast. There is a lot of concern about unemployment. Recent events in the e-Zone must have Italians worried; they can see that if they slip-up there is no safety net that will be thrown under them, maybe a blanket thrown over them after-the-fact. The thought is chilling. Not even pasta can salve the pain.

| Italy ISAE Consumer Confidence | |||||||

|---|---|---|---|---|---|---|---|

| Since 1992 | Rank | ||||||

| Mar-10 | Feb-10 | Jan-10 | Dec-09 | Percentile | Rank | percentile | |

| Consumer Confidence | 106.3 | 107.7 | 111.6 | 113.6 | 37.4 | 146 | 31.5% |

| Last 12 months | |||||||

| OVERALL SITUATION | -63 | -67 | -54 | -57 | 67.2 | 83 | 61.0% |

| PRICE TRENDS | -41.5 | -45 | -38 | -41 | 12.6 | 206 | 3.3% |

| Next 12months | |||||||

| OVERALL SITUATION | -14 | -14 | -1 | -1 | 39.7 | 140 | 34.3% |

| PRICE TRENDS | 17 | 16 | 11.5 | 8.5 | 39.5 | 48 | 77.5% |

| UNEMPLOYMENT | 26 | 25 | 16 | 16 | 82.4 | 4 | 98.1% |

| HOUSEHOLD BUDGET | 0 | 2 | -1 | 1 | 16.3 | 202 | 5.2% |

| HOUSEHOLD FIN SITUATION | |||||||

| Last 12 months | -38 | -39 | -36 | -37 | 36.7 | 138 | 35.2% |

| Next12 months | -6 | -7 | -6 | -3 | 59.2 | 136 | 36.2% |

| HOUSEHOLD SAVINGS | |||||||

| Current | 69 | 73 | 78 | 73 | 81.7 | 13 | 93.9% |

| Future | -29 | -24 | -23 | -20 | 43.2 | 159 | 25.4% |

| MAJOR Purchases | |||||||

| Current | -40 | -39 | -36 | -38 | 47.1 | 98 | 54.0% |

| Total number of months: Back to Jul-92 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief