Global| Sep 28 2009

Global| Sep 28 2009Italian Consumer Confidence Moves Sharply Higher

Summary

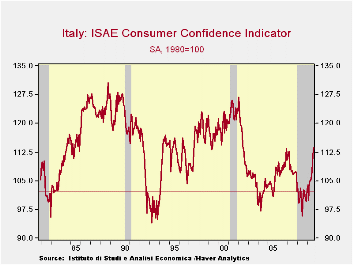

Getting better - Italian consumer confidence rose sharply higher in September. After bottoming in August of 2008, confidence made a large 4.3point jump in August 2009 and in September of 2009 it has added a further advance of 1.8 [...]

Getting better - Italian

consumer confidence rose sharply

higher in September. After bottoming in August of 2008, confidence made

a large 4.3point jump in August 2009 and in September of 2009 it has

added a further advance of 1.8 points. The rise in August had been the

13th largest monthly gain on record. Having another significant rise

(55th largest out of 215 total.) is a sign that the improvement has

legs. Now you have to go back to July of 2002 to find a higher reading

as the rise in September brings the consumer sentiment reading above

its previous local peak at end 2006.

Getting better - Italian

consumer confidence rose sharply

higher in September. After bottoming in August of 2008, confidence made

a large 4.3point jump in August 2009 and in September of 2009 it has

added a further advance of 1.8 points. The rise in August had been the

13th largest monthly gain on record. Having another significant rise

(55th largest out of 215 total.) is a sign that the improvement has

legs. Now you have to go back to July of 2002 to find a higher reading

as the rise in September brings the consumer sentiment reading above

its previous local peak at end 2006.

Upbeat on the future - Italians rate their confidence overall in the 79th percentile of its range since 1992 and better than the readings that are produced 62% of the time (its rank standing). Italian consumers now rate the overall situation as in the 77th percentile of its range at a raw reading of -58. Over the next twelve months (the raw reading is +6) but as a percentile it stands in the 69th percentile of its range. Note the difference in Italian consumers and their expectations. At a raw reading of -58 the overall situation is rated in the 77th percentile of its range a rather high percentile standing for such a sour (net!) negative reading. When it comes to looking ahead, however, the raw reading of +6 stands in the 69th percentile of its range, a roughly comparable relative position. Clearly this suggests that Italian consumes are prone to optimism. But the percentiles of course adjust for that; the raw readings do not, but they are instructive. It is interesting ant a people whose capital city is replete with ruins of its past greatness are able to shake off any semblance of an empire past and look so optimistically to the future.

Flies in the ointment or outlook - Unemployment, however, is still feared as the unemployment expectation reading is still in the 69th percentile of its range. The unemployment expectations worsened month to month with 23% (up from 20) worried that it might rise sharply. Those fearing a slight increase fell to 39% from 40%.. Stable unemployment is now expected by 28% up from 26%. But only 3% (down from 5%) of Italians think unemployment will fall. It’s an odd set of responses on unemployment prospects to occur is such another upbeat assessment of the future.

Upbeat on spending - The household financial situation was in the 46th percentile of its range over the past 12 months while expectations are in the 69th percentile over the next 12-months. The environment for making purchases is in the 42nd percentile while in the next twelve months it is expected to rise to the 96th percentile.

High hopes - Obviously for Italy hopes are high. Current measures have improved but there is still a lot that is wrong. For whatever reason Italian consumers have ratcheted up their expectations especially as to the future environment for making purchases. The news is good news, but it is heavily dependent on confidence, per se. While Germany seems to be getting more concerned about its future and the potential for unemployment to rise in Italy, glee over the outlook is spreading amid a still sour outlook for unemployment prospects. Still, the overall reading is at its best level since mid-2002.

| Italy ISAE Consumer Confidence | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Since Jan 1992 | Rank | ||||||||||

| Sep 09 |

Aug 09 |

Jul 09 |

Jun 09 |

Percen tile |

Rank | Max | Min | Range | Mean | percen tile |

|

| Consumer Confidence | 113.6 | 111.8 | 107.5 | 105.5 | 59.8 | 79 | 127 | 94 | 33 | 110 | 62.9% |

| Last 12 months | |||||||||||

| OVERALL SITUATION |

-58 | -62 | -68 | -68 | 71.2 | 68 | -22 | -147 | 125 | -70 | 68.1% |

| PRICE TRENDS | -42 | -42 | -48 | -40.5 | 11.7 | 208 | 4 | -48 | 52 | -9 | 2.3% |

| Next 12months | |||||||||||

| OVERALL SITUATION |

5 | 1 | 2 | -8 | 69.8 | 12 | 24 | -39 | 63 | -9 | 94.4% |

| PRICE TRENDS | 9.5 | 7.5 | 1.5 | 8.5 | 19.4 | 92 | 49 | 0 | 49 | 11 | 56.8% |

| UNEMPLOYMENT | 17 | 11 | 8 | 15 | 69.1 | 7 | 38 | -30 | 68 | -1 | 96.7% |

| HOUSEHOLD BUDGET | 6 | 0 | 1 | 0 | 27.7 | 178 | 40 | -7 | 47 | 16 | 16.4% |

| HOUSEHOLD FIN SITUATION | |||||||||||

| Last 12 months | -33 | -34 | -40 | -37 | 46.9 | 89 | -7 | -56 | 49 | -31 | 58.2% |

| Next12 months | -1 | -2 | -2 | -4 | 69.4 | 86 | 14 | -35 | 49 | -3 | 59.6% |

| HOUSEHOLD SAVINGS | |||||||||||

| Current | 80 | 79 | 60 | 60 | 100.0 | 1 | 80 | 20 | 60 | 43 | 99.5% |

| Future | -16 | -21 | -30 | -25 | 68.1 | 106 | -1 | -48 | 47 | -19 | 50.2% |

| MAJOR Purchases | |||||||||||

| Current | -40 | -37 | -40 | -39 | 42.1 | 100 | -7 | -64 | 57 | -39 | 53.1% |

| Future | 4 | 4 | 4 | 3 | 96.8 | 3 | 7 | -87 | 94 | -64 | 98.6% |

| Total number of months: 213 | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief